- United States

- /

- Banks

- /

- NasdaqGM:OPBK

Forecast: Analysts Think OP Bancorp's (NASDAQ:OPBK) Business Prospects Have Improved Drastically

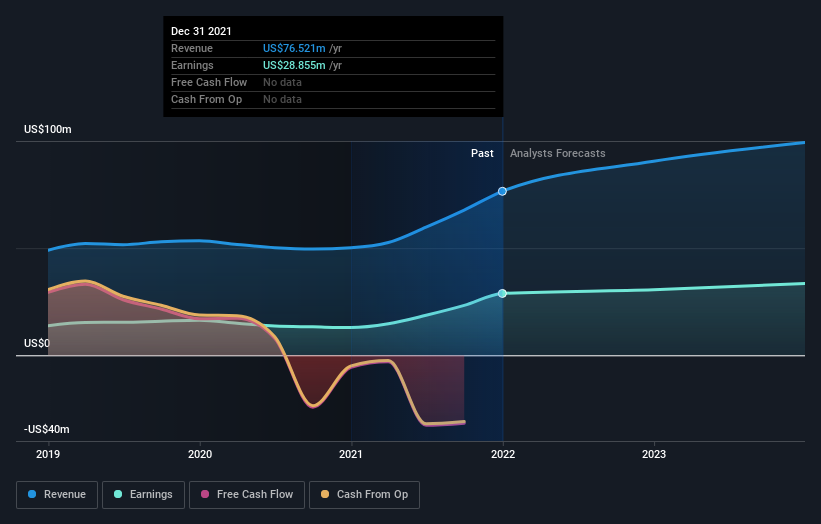

Shareholders in OP Bancorp (NASDAQ:OPBK) may be thrilled to learn that the analysts have just delivered a major upgrade to their near-term forecasts. The consensus statutory numbers for both revenue and earnings per share (EPS) increased, with their view clearly much more bullish on the company's business prospects. The market may be pricing in some blue sky too, with the share price gaining 15% to US$14.01 in the last 7 days. It will be interesting to see if today's upgrade is enough to propel the stock even higher.

Following the upgrade, the latest consensus from OP Bancorp's twin analysts is for revenues of US$91m in 2022, which would reflect a decent 18% improvement in sales compared to the last 12 months. Statutory earnings per share are presumed to accumulate 5.7% to US$2.02. Prior to this update, the analysts had been forecasting revenues of US$78m and earnings per share (EPS) of US$1.69 in 2022. There has definitely been an improvement in perception recently, with the analysts substantially increasing both their earnings and revenue estimates.

See our latest analysis for OP Bancorp

With these upgrades, we're not surprised to see that the analysts have lifted their price target 18% to US$17.75 per share. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values OP Bancorp at US$18.00 per share, while the most bearish prices it at US$17.50. This is a very narrow spread of estimates, implying either that OP Bancorp is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Of course, another way to look at these forecasts is to place them into context against the industry itself. The analysts are definitely expecting OP Bancorp's growth to accelerate, with the forecast 18% annualised growth to the end of 2022 ranking favourably alongside historical growth of 10% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to see a revenue decline of 1.6% annually. It seems obvious that as part of the brighter growth outlook, OP Bancorp is expected to grow faster than the wider industry.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. Fortunately, they also upgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider market. With a serious upgrade to expectations and a rising price target, it might be time to take another look at OP Bancorp.

Using these estimates as a starting point, we've run a discounted cash flow calculation (DCF) on OP Bancorp that suggests the company could be somewhat undervalued. For more information, you can click through to our platform to learn more about our valuation approach.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:OPBK

OP Bancorp

Operates as the bank holding company for Open Bank that provides banking products and services.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Community Narratives