Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:EFSC

Enterprise Financial Services (NASDAQ:EFSC) Is Increasing Its Dividend To $0.24

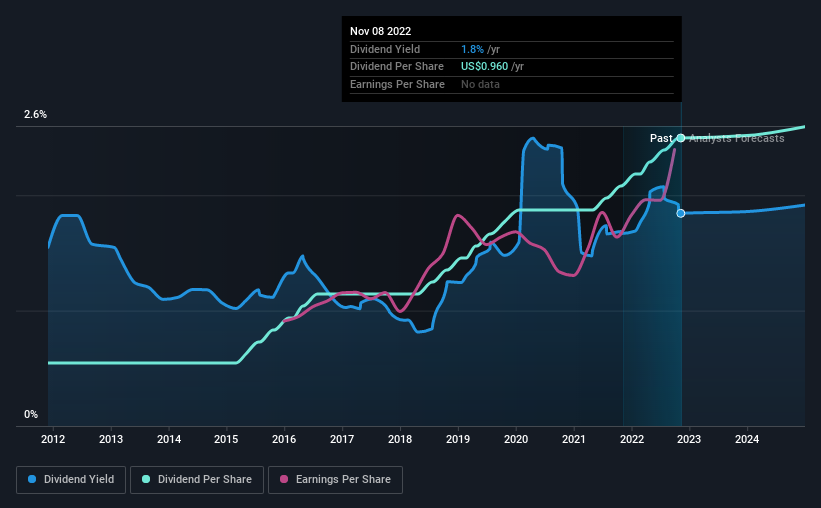

Enterprise Financial Services Corp (NASDAQ:EFSC) will increase its dividend from last year's comparable payment on the 30th of December to $0.24. This takes the annual payment to 1.8% of the current stock price, which unfortunately is below what the industry is paying.

Check out the opportunities and risks within the US Banks industry.

Enterprise Financial Services' Dividend Forecasted To Be Well Covered By Earnings

If it is predictable over a long period, even low dividend yields can be attractive.

Enterprise Financial Services has a long history of paying out dividends, with its current track record at a minimum of 10 years. While past records don't necessarily translate into future results, the company's payout ratio of 17% also shows that Enterprise Financial Services is able to comfortably pay dividends.

Over the next 3 years, EPS is forecast to expand by 17.3%. Analysts estimate the future payout ratio will be 18% over the same time period, which is in the range that makes us comfortable with the sustainability of the dividend.

Enterprise Financial Services Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The dividend has gone from an annual total of $0.21 in 2012 to the most recent total annual payment of $0.96. This works out to be a compound annual growth rate (CAGR) of approximately 16% a year over that time. Rapidly growing dividends for a long time is a very valuable feature for an income stock.

The Dividend Looks Likely To Grow

The company's investors will be pleased to have been receiving dividend income for some time. We are encouraged to see that Enterprise Financial Services has grown earnings per share at 16% per year over the past five years. Enterprise Financial Services definitely has the potential to grow its dividend in the future with earnings on an uptrend and a low payout ratio.

We Really Like Enterprise Financial Services' Dividend

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. Earnings are easily covering distributions, and the company is generating plenty of cash. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Earnings growth generally bodes well for the future value of company dividend payments. See if the 6 Enterprise Financial Services analysts we track are forecasting continued growth with our free report on analyst estimates for the company. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Enterprise Financial Services might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:EFSC

Enterprise Financial Services

Operates as the financial holding company for Enterprise Bank & Trust that offers banking and wealth management services to individuals and corporate customers in Arizona, California, Florida, Kansas, Missouri, Nevada, and New Mexico.

Very undervalued with flawless balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor