Advertisement

- United States

- /

- Banks

- /

- NasdaqCM:CWBC

Community West Bancshares (NASDAQ:CWBC) Will Pay A Dividend Of $0.12

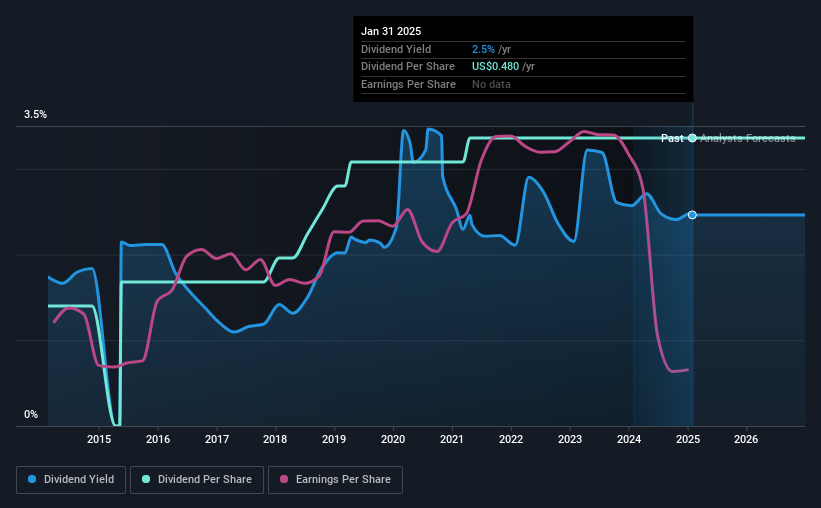

The board of Community West Bancshares (NASDAQ:CWBC) has announced that it will pay a dividend of $0.12 per share on the 21st of February. This means the annual payment will be 2.5% of the current stock price, which is lower than the industry average.

Check out our latest analysis for Community West Bancshares

Community West Bancshares' Earnings Will Easily Cover The Distributions

If it is predictable over a long period, even low dividend yields can be attractive.

Community West Bancshares has established itself as a dividend paying company with over 10 years history of distributing earnings to shareholders. But while this history shows that the company was able to sustain its dividend for a decent period of time, its most recent earnings report shows that the company did not make enough earnings to cover its dividend payout. This is an alarming sign that could mean that Community West Bancshares' dividend at its current rate may no longer be sustainable for longer.

Looking forward, earnings per share is forecast by analysts to rise exponentially over the next 3 years. They also estimate the payout ratio reaching 21% in the same time period, which is fairly sustainable.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. The annual payment during the last 10 years was $0.20 in 2015, and the most recent fiscal year payment was $0.48. This means that it has been growing its distributions at 9.1% per annum over that time. It's good to see the dividend growing at a decent rate, but the dividend has been cut at least once in the past. Community West Bancshares might have put its house in order since then, but we remain cautious.

Dividend Growth Potential Is Shaky

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Community West Bancshares' earnings per share has shrunk at 24% a year over the past five years. A sharp decline in earnings per share is not great from from a dividend perspective. Even conservative payout ratios can come under pressure if earnings fall far enough. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

We should note that Community West Bancshares has issued stock equal to 61% of shares outstanding. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

Community West Bancshares' Dividend Doesn't Look Sustainable

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Community West Bancshares' payments, as there could be some issues with sustaining them into the future. The track record isn't great, and the payments are a bit high to be considered sustainable. We don't think Community West Bancshares is a great stock to add to your portfolio if income is your focus.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. Just as an example, we've come across 5 warning signs for Community West Bancshares you should be aware of, and 1 of them doesn't sit too well with us. Is Community West Bancshares not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:CWBC

Community West Bancshares

Operates as the bank holding company for the Central Valley Community Bank that provides various commercial banking services to small and middle-market businesses and individuals in California.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor