Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:CFB

CrossFirst Bankshares, Inc. Recorded A 41% Miss On Revenue: Analysts Are Revisiting Their Models

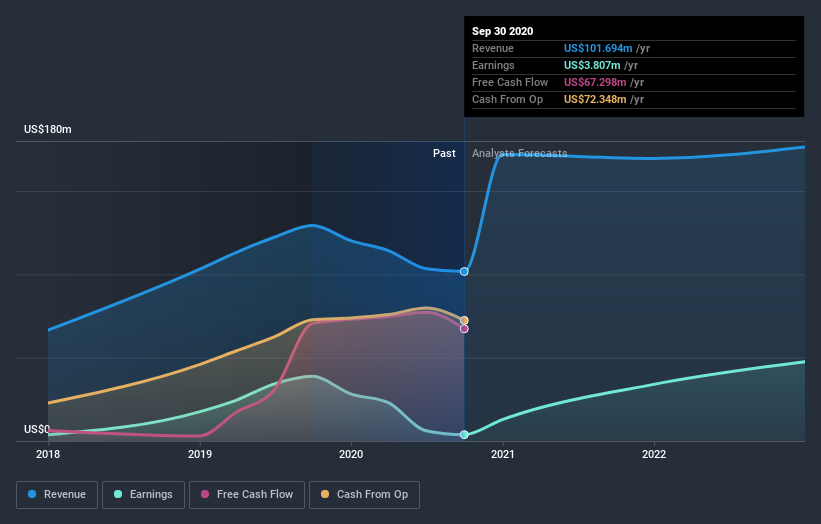

The analysts might have been a bit too bullish on CrossFirst Bankshares, Inc. (NASDAQ:CFB), given that the company fell short of expectations when it released its annual results last week. Earnings came in short of expectations, with revenues of US$102m missing the mark by 41%, and statutory earnings per share of US$0.24 falling 2.4% short. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Check out our latest analysis for CrossFirst Bankshares

Taking into account the latest results, the consensus forecast from CrossFirst Bankshares' five analysts is for revenues of US$169.5m in 2021, which would reflect a major 67% improvement in sales compared to the last 12 months. Statutory earnings per share are predicted to soar 825% to US$0.68. In the lead-up to this report, the analysts had been modelling revenues of US$169.5m and earnings per share (EPS) of US$0.68 in 2021. So it's pretty clear that, although the analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

With the analysts reconfirming their revenue and earnings forecasts, it's surprising to see that the price target rose 10.0% to US$13.20. It looks as though they previously had some doubts over whether the business would live up to their expectations. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic CrossFirst Bankshares analyst has a price target of US$14.00 per share, while the most pessimistic values it at US$10.00. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's clear from the latest estimates that CrossFirst Bankshares' rate of growth is expected to accelerate meaningfully, with the forecast 67% revenue growth noticeably faster than its historical growth of 11%p.a. over the past three years. Compare this with other companies in the same industry, which are forecast to grow their revenue 6.5% next year. Factoring in the forecast acceleration in revenue, it's pretty clear that CrossFirst Bankshares is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have estimates - from multiple CrossFirst Bankshares analysts - going out to 2022, and you can see them free on our platform here.

Even so, be aware that CrossFirst Bankshares is showing 3 warning signs in our investment analysis , you should know about...

If you’re looking to trade CrossFirst Bankshares, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGS:CFB

CrossFirst Bankshares

Operates as the bank holding company for CrossFirst Bank that provides various banking and financial services to businesses, business owners, professionals, and its personal networks.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|28.9% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|46.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.8% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.2% undervalued

AX

Community Contributor