Advertisement

Over the last several months, Ford Motor Company ( NYSE: F ) rose to a multi-year high, fueled by the newfound success with the electric truck (EV) . Yet, growth forecasts remain modest and the debt-to-equity ratio high.

When we think about how risky a company is, we always like to look at its use of debt since debt overload can ruin it. Notably, Ford does carry a lot of debt. But should shareholders be worried about its use of debt?

Recent Developments

After the 2020 market crash, the stock rallied big, basically quadrupling and reaching $16 for the new 5-year high. Thanks to the new F-150 Lightning Truck, sold-out Mustang Mach-E, and other upcoming EVs, Ford generated significant positive buzz. Electrified vehicle sales doubled in the first half of the year, reaching 56,570 units.

The company also announced a plan for an all-electric line-up by 2030 . It is an ambitious plan from one of the oldest car brands that remain the most present automobile on the American market. High brand loyalty is a strength in the transitory periods.

See our latest analysis for Ford Motor

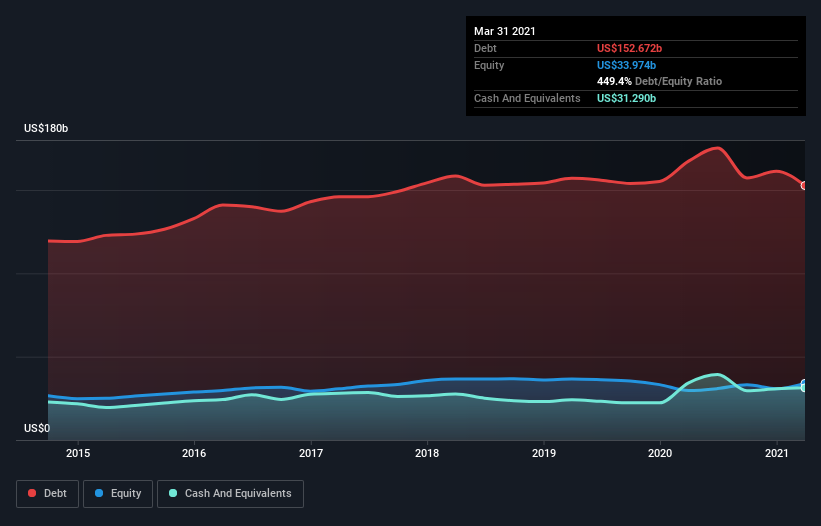

What Is Ford Motor's Net Debt?

You can click the graphic below for the historical numbers, but it shows that Ford Motor had US$152.7b of debt in March 2021, down from US$167.3b, one year before. On the flip side, it has US$31.3b in cash leading to net debt of about US$121.4b.

NYSE: F Debt to Equity History July 7th, 2021

A Look At Ford Motor's Liabilities

We can see from the most recent balance sheet that Ford Motor had liabilities of US$94.2b falling due within a year and liabilities of US$132.6b due beyond that. Offsetting this, it had US$31.3b in cash and US$3.97b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$191.6b.

This massive deficit casts a shadow over the US$57.9b company. So we think shareholders need to watch this one closely. Ford Motor would probably need a significant re-capitalization if its creditors were to demand repayment.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Weak interest cover of 0.96 times and a disturbingly high net debt to EBITDA ratio of 14.4 hit our confidence in Ford Motor like a one-two punch to the gut. This means we'd consider it to have a heavy debt load. However, it should be comfortable for shareholders to recall that Ford Motor grew its EBIT by a hefty 492% over the last 12 months. If it can keep walking that path, it will be in a position to shed its debt with relative ease. The balance sheet is the area to focus on when you are analyzing debt. But it is future earnings that will determine Ford Motor's ability to maintain a healthy balance sheet going forward. So if you're focused on the future, you can check out this free report showing analyst profit forecasts .

But our final consideration is also crucial because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Happily for many shareholders, Ford Motor produced more free cash flow than EBIT over the last three years.

Our View

Ford Motor's interest cover left us tentative about the stock, and its level of total liabilities amplified that impression.

But on the bright side, its conversion of EBIT to free cash flow is a good sign and makes us more optimistic. Looking at the balance sheet and considering all these factors, we believe that debt makes Ford Motor stock a bit risky. That's not necessarily a bad thing, but we'd generally feel more comfortable with less leverage.

Even so, car manufacturing is hardly the best business model. It is a highly capital-intensive cyclical business, required to continuously innovate to stay on the top of the game. Ford has unquestionably surprised by a successful EV launch. If the trend persists, we will see a balance sheet turn-around from one of the most resilient car brands in history.

Although the balance sheet is the area to focus on when analyzing debt, every company can contain risks outside the balance sheet. Case in point: We've spotted 2 warning signs for Ford Motor you should be aware of, and 1 of them is concerning.

It’s often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stjepan Kalinic

Stjepan is a writer and an analyst covering equity markets. As a former multi-asset analyst, he prefers to look beyond the surface and uncover ideas that might not be on retail investors' radar. You can find his research all over the internet, including Simply Wall St News, Yahoo Finance, Benzinga, Vincent, and Barron's.

About NYSE:F

Ford Motor

Develops, delivers, and services Ford trucks, sport utility vehicles, commercial vans and cars, and Lincoln luxury vehicles worldwide.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|3.6% undervalued

TI

Community Contributor

Recently Updated Narratives

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8148.6% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.0% undervalued

22 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BI

BinocularMan on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.3% undervalued

128 followersusers have followed this narrative

5 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

79 followersusers have followed this narrative

10 commentsusers have commented on this narrative

17 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7921.6% undervalued

915 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative