Advertisement

- United States

- /

- Auto Components

- /

- NasdaqCM:WKSP

Increases to Worksport Ltd.'s (NASDAQ:WKSP) CEO Compensation Might Cool off for now

Key Insights

- Worksport's Annual General Meeting to take place on 6th of December

- Total pay for CEO Steve Rossi includes US$374.2k salary

- Total compensation is 205% above industry average

- Worksport's EPS declined by 6.3% over the past three years while total shareholder loss over the past three years was 84%

Shareholders of Worksport Ltd. (NASDAQ:WKSP) will have been dismayed by the negative share price return over the last three years. Per share earnings growth is also poor, despite revenues growing. In light of this performance, shareholders will have a chance to question the board in the upcoming AGM on 6th of December, where they can impact on future company performance by voting on resolutions, including executive compensation. Here's our take on why we think shareholders might be hesitant about approving a raise at the moment.

Check out our latest analysis for Worksport

Comparing Worksport Ltd.'s CEO Compensation With The Industry

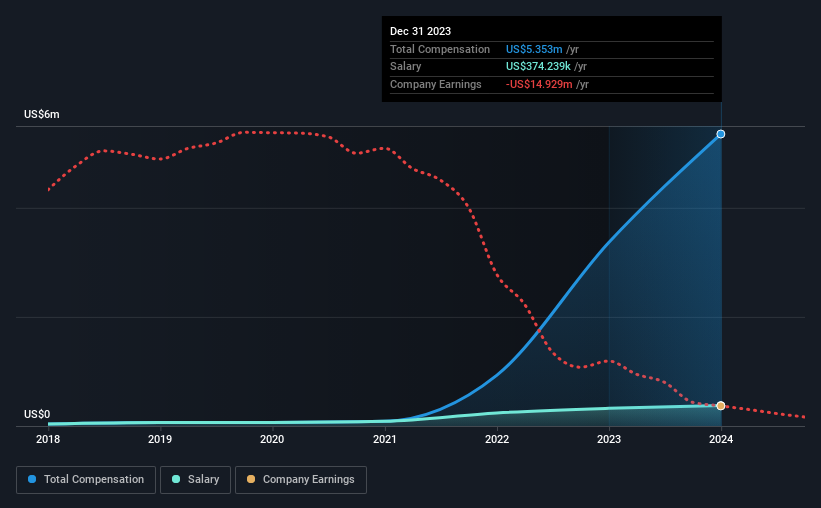

According to our data, Worksport Ltd. has a market capitalization of US$19m, and paid its CEO total annual compensation worth US$5.4m over the year to December 2023. We note that's an increase of 59% above last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$374k.

For comparison, other companies in the American Auto Components industry with market capitalizations below US$200m, reported a median total CEO compensation of US$1.8m. Hence, we can conclude that Steve Rossi is remunerated higher than the industry median. What's more, Steve Rossi holds US$1.5m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$374k | US$324k | 7% |

| Other | US$5.0m | US$3.0m | 93% |

| Total Compensation | US$5.4m | US$3.4m | 100% |

Talking in terms of the industry, salary represented approximately 12% of total compensation out of all the companies we analyzed, while other remuneration made up 88% of the pie. In Worksport's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Worksport Ltd.'s Growth Numbers

Over the last three years, Worksport Ltd. has shrunk its earnings per share by 6.3% per year. It achieved revenue growth of 777% over the last year.

Investors would be a bit wary of companies that have lower EPS But in contrast the revenue growth is strong, suggesting future potential for EPS growth. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Worksport Ltd. Been A Good Investment?

Few Worksport Ltd. shareholders would feel satisfied with the return of -84% over three years. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

The returns to shareholders is disappointing along with lack of earnings growth, which goes some way in explaining the poor returns. In the upcoming AGM, shareholders will get the opportunity to discuss any issues with the board, including those related to CEO remuneration and assess if the board's plan is in line with their expectations.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 4 warning signs for Worksport (of which 2 shouldn't be ignored!) that you should know about in order to have a holistic understanding of the stock.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if Worksport might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:WKSP

Worksport

Together with its subsidiary, designs and distributes truck tonneau covers in Canada and the United States.

Moderate risk with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative