Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, HTC Corporation (TWSE:2498) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for HTC

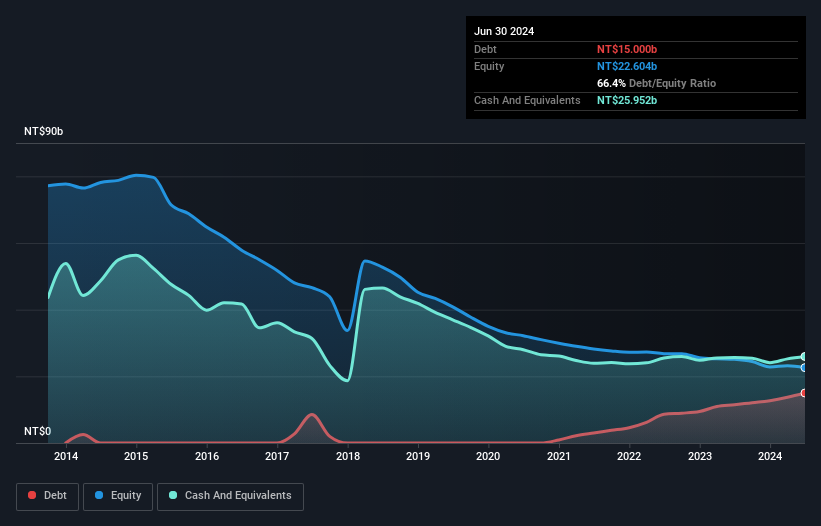

How Much Debt Does HTC Carry?

You can click the graphic below for the historical numbers, but it shows that as of June 2024 HTC had NT$15.0b of debt, an increase on NT$11.5b, over one year. However, it does have NT$26.0b in cash offsetting this, leading to net cash of NT$11.0b.

How Strong Is HTC's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that HTC had liabilities of NT$13.4b due within 12 months and liabilities of NT$11.7b due beyond that. Offsetting this, it had NT$26.0b in cash and NT$826.6m in receivables that were due within 12 months. So it can boast NT$1.73b more liquid assets than total liabilities.

This surplus suggests that HTC has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, HTC boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if HTC can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year HTC had a loss before interest and tax, and actually shrunk its revenue by 17%, to NT$3.7b. That's not what we would hope to see.

So How Risky Is HTC?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that HTC had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of NT$3.0b and booked a NT$3.5b accounting loss. While this does make the company a bit risky, it's important to remember it has net cash of NT$11.0b. That means it could keep spending at its current rate for more than two years. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. For riskier companies like HTC I always like to keep an eye on the long term profit and revenue trends. Fortunately, you can click to see our interactive graph of its profit, revenue, and operating cashflow.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if HTC might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:2498

HTC

Designs, manufactures, assembles, processes, and sells smart mobile and virtual reality devices in Taiwan and internationally.

Acceptable track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.7% undervalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

27 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on PayPal Holdings ·

The "Sleeping Giant" Wakes Up – Efficiency & Monetization

Fair Value:US$174.9264.2% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Pagaya Technologies ·

The "Rate Cut" Supercycle Winner – Profitable & Accelerating

Fair Value:US$170.685.9% undervalued

1 followerusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Archer Aviation ·

The Industrialist of the Skies – Scaling with "Automotive DNA

Fair Value:US$16.3254.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

111 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

945 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

146 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative