In a week marked by volatility, global markets have been influenced by a mix of corporate earnings reports and geopolitical developments, with the U.S. Federal Reserve holding interest rates steady amidst ongoing inflation concerns. As investors navigate these uncertain waters, dividend stocks offer a potential source of stability and income, making them an attractive option for those seeking to balance risk with reliable returns in today's market environment.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Guaranty Trust Holding (NGSE:GTCO) | 5.97% | ★★★★★★ |

| Peoples Bancorp (NasdaqGS:PEBO) | 4.98% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 7.47% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.53% | ★★★★★★ |

| Daito Trust ConstructionLtd (TSE:1878) | 4.01% | ★★★★★★ |

| Citizens & Northern (NasdaqCM:CZNC) | 5.33% | ★★★★★★ |

| Southside Bancshares (NYSE:SBSI) | 4.66% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.46% | ★★★★★★ |

| FALCO HOLDINGS (TSE:4671) | 6.70% | ★★★★★★ |

| Premier Financial (NasdaqGS:PFC) | 4.56% | ★★★★★★ |

Click here to see the full list of 1980 stocks from our Top Dividend Stocks screener.

Let's explore several standout options from the results in the screener.

San Fang Chemical Industry (TWSE:1307)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: San Fang Chemical Industry Co., Ltd. is a company that manufactures and sells artificial leather, synthetic resin, and other materials in Taiwan, China, Hong Kong, Southeast Asia, and internationally with a market cap of NT$15.40 billion.

Operations: San Fang Chemical Industry Co., Ltd.'s revenue segments include NT$1.08 billion from GII, NT$2.55 billion from PTS, NT$1.78 billion from Sanfang Development Co., Ltd., and NT$8.03 billion from SAN Fang Chemical Industry Co., Ltd.

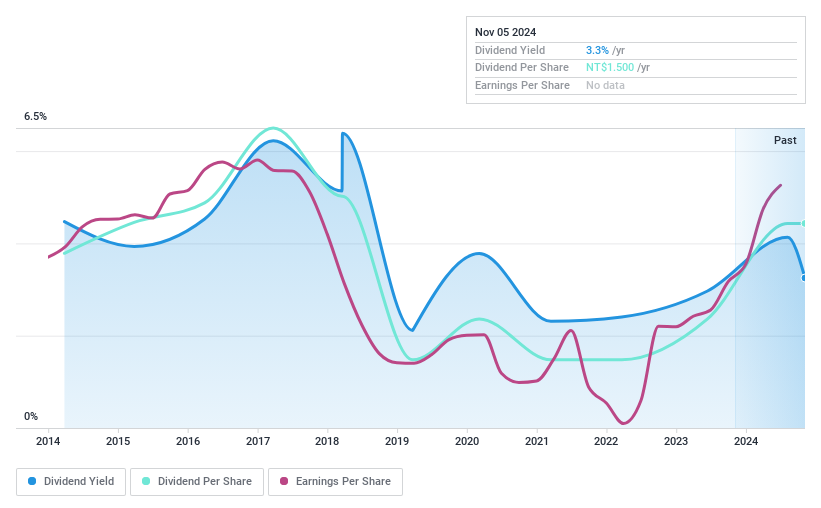

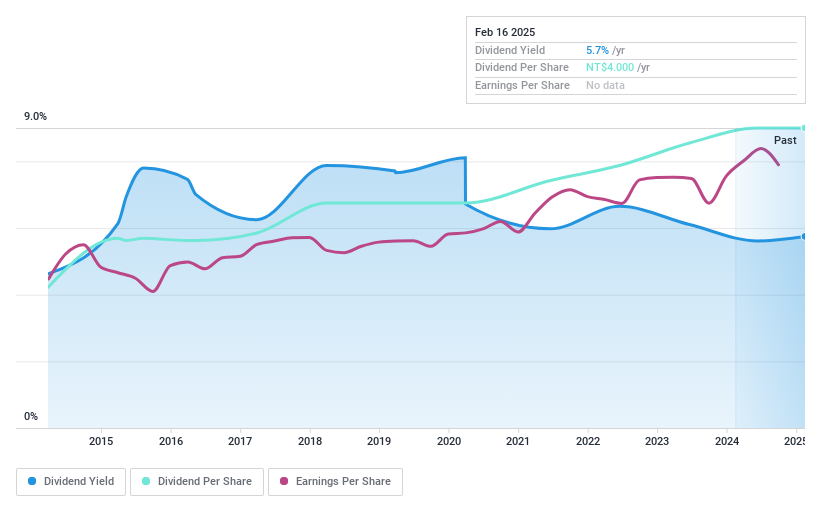

Dividend Yield: 3.9%

San Fang Chemical Industry's recent earnings report shows solid growth, with net income rising to TWD 385.86 million in Q3 2024 from TWD 314.68 million the previous year. Despite a dividend yield lower than top-tier payers, its dividends are well-covered by earnings and cash flows, with payout ratios around 49%. However, the company's dividend history is volatile and unreliable over the past decade, impacting its appeal as a stable dividend stock.

- Click here and access our complete dividend analysis report to understand the dynamics of San Fang Chemical Industry.

- Upon reviewing our latest valuation report, San Fang Chemical Industry's share price might be too pessimistic.

Synnex Technology International (TWSE:2347)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Synnex Technology International Corporation, along with its subsidiaries, distributes information system, communication, consumer, and semiconductor products and has a market cap of NT$120.76 billion.

Operations: Synnex Technology International Corporation's revenue is primarily derived from its Distribution Business Group, which accounts for NT$281.46 billion, and its Semiconductor Business Group, contributing NT$170.54 billion.

Dividend Yield: 4.1%

Synnex Technology International's recent earnings report indicates strong growth, with Q3 2024 net income rising to TWD 2.26 billion from TWD 1.70 billion a year ago. The company's dividends are well-covered by earnings and cash flows, with payout ratios of 59.3% and 53.6%, respectively, but its dividend yield is below the top tier in the TW market at 4.14%. Despite past volatility, dividends have increased over the last decade.

- Take a closer look at Synnex Technology International's potential here in our dividend report.

- Upon reviewing our latest valuation report, Synnex Technology International's share price might be too optimistic.

Audix (TWSE:2459)

Simply Wall St Dividend Rating: ★★★★★★

Overview: Audix Corporation is engaged in the manufacturing, marketing, trading, and distribution of electronic components in Taiwan with a market cap of NT$7.19 billion.

Operations: Audix Corporation's revenue primarily stems from its Manufacturing Business Group, contributing NT$3.24 billion, and the Access Business Group Department, which adds NT$2.32 billion.

Dividend Yield: 5.9%

Audix Corporation's recent earnings report shows a decline in Q3 2024 sales and revenue compared to the previous year, but net income for the nine months increased. The company offers a high dividend yield of 5.87%, placing it in the top 25% of TW market payers. Dividends are reliably covered by earnings and cash flows with payout ratios of 70.1% and 81.4%, respectively, supported by consistent growth over the past decade without volatility.

- Click here to discover the nuances of Audix with our detailed analytical dividend report.

- Our expertly prepared valuation report Audix implies its share price may be too high.

Where To Now?

- Investigate our full lineup of 1980 Top Dividend Stocks right here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:1307

San Fang Chemical Industry

Manufactures and sells artificial leather, synthetic resin, and other materials in Taiwan, China, Hong Kong, Southeast Asia, and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Community Narratives