As global markets navigate uncertainties around tariffs and economic data, investors are seeking stability amid fluctuating indices. In this climate, dividend stocks can offer a reliable income stream and potential for long-term growth, making them an attractive consideration for portfolio diversification.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Guaranty Trust Holding (NGSE:GTCO) | 5.83% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 7.54% | ★★★★★★ |

| Tsubakimoto Chain (TSE:6371) | 4.33% | ★★★★★★ |

| Daito Trust ConstructionLtd (TSE:1878) | 4.04% | ★★★★★★ |

| Nihon Parkerizing (TSE:4095) | 3.84% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.41% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.12% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 3.90% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 3.35% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.28% | ★★★★★★ |

Click here to see the full list of 1971 stocks from our Top Dividend Stocks screener.

We'll examine a selection from our screener results.

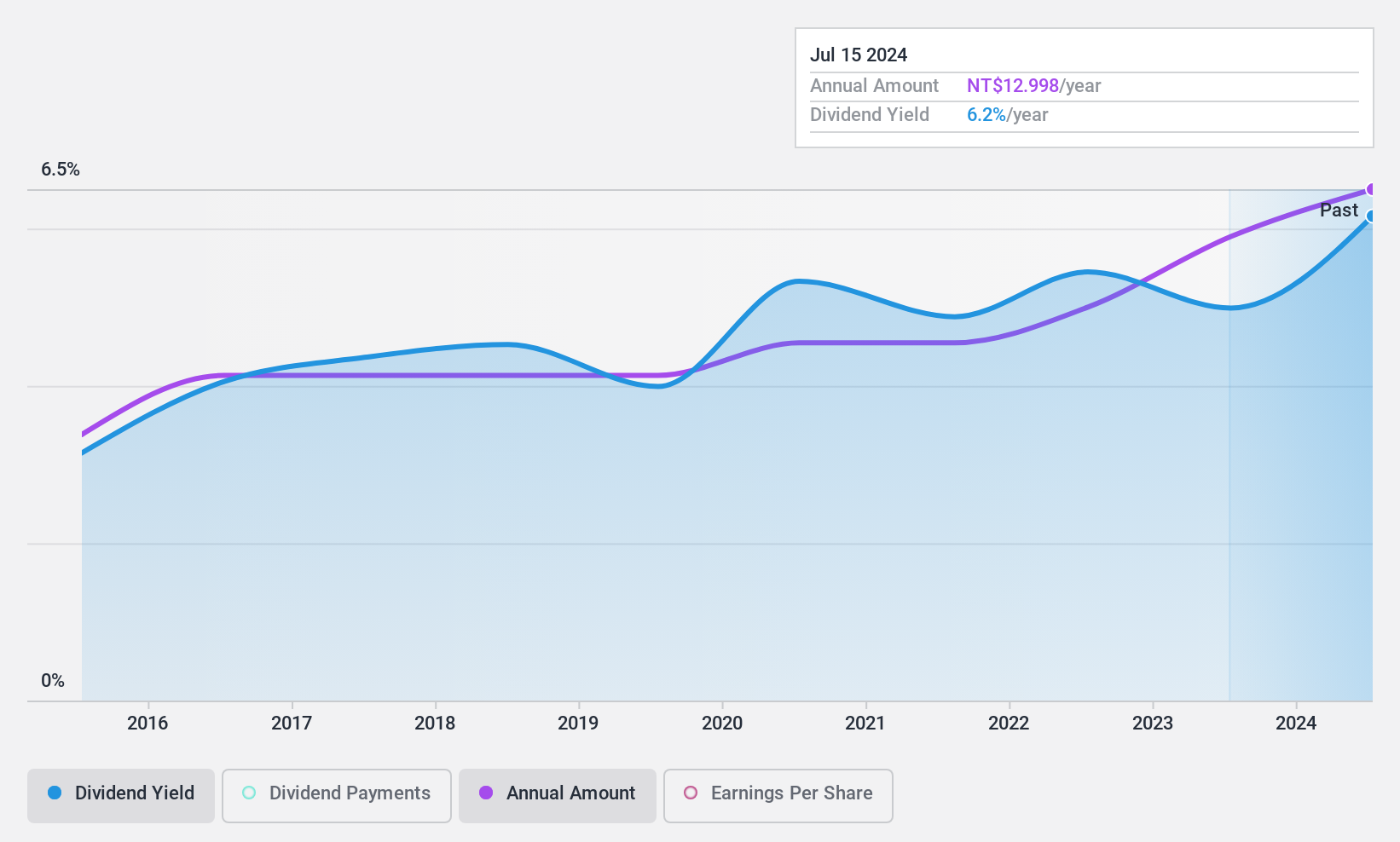

TSC Auto ID Technology (TPEX:3611)

Simply Wall St Dividend Rating: ★★★★★★

Overview: TSC Auto ID Technology Co., Ltd. manufactures and services auto-identification systems and products globally, with a market cap of NT$10.23 billion.

Operations: TSC Auto ID Technology Co., Ltd. generates revenue primarily from selling bar code printers and their spare parts (NT$4.86 billion) and various label papers and consumables for printers (NT$3.47 billion).

Dividend Yield: 6%

TSC Auto ID Technology offers a compelling dividend profile with a 6.05% yield, placing it in the top 25% of TW market payers. Dividends have been stable and growing over the past decade, supported by earnings and cash flows with payout ratios of 87.1% and 85.9%, respectively. Despite recent profit margin declines from 12.2% to 8.5%, its P/E ratio of 14.5x suggests good value relative to peers and industry standards amidst recent CFO changes effective January 2025.

- Click here to discover the nuances of TSC Auto ID Technology with our detailed analytical dividend report.

- The analysis detailed in our TSC Auto ID Technology valuation report hints at an deflated share price compared to its estimated value.

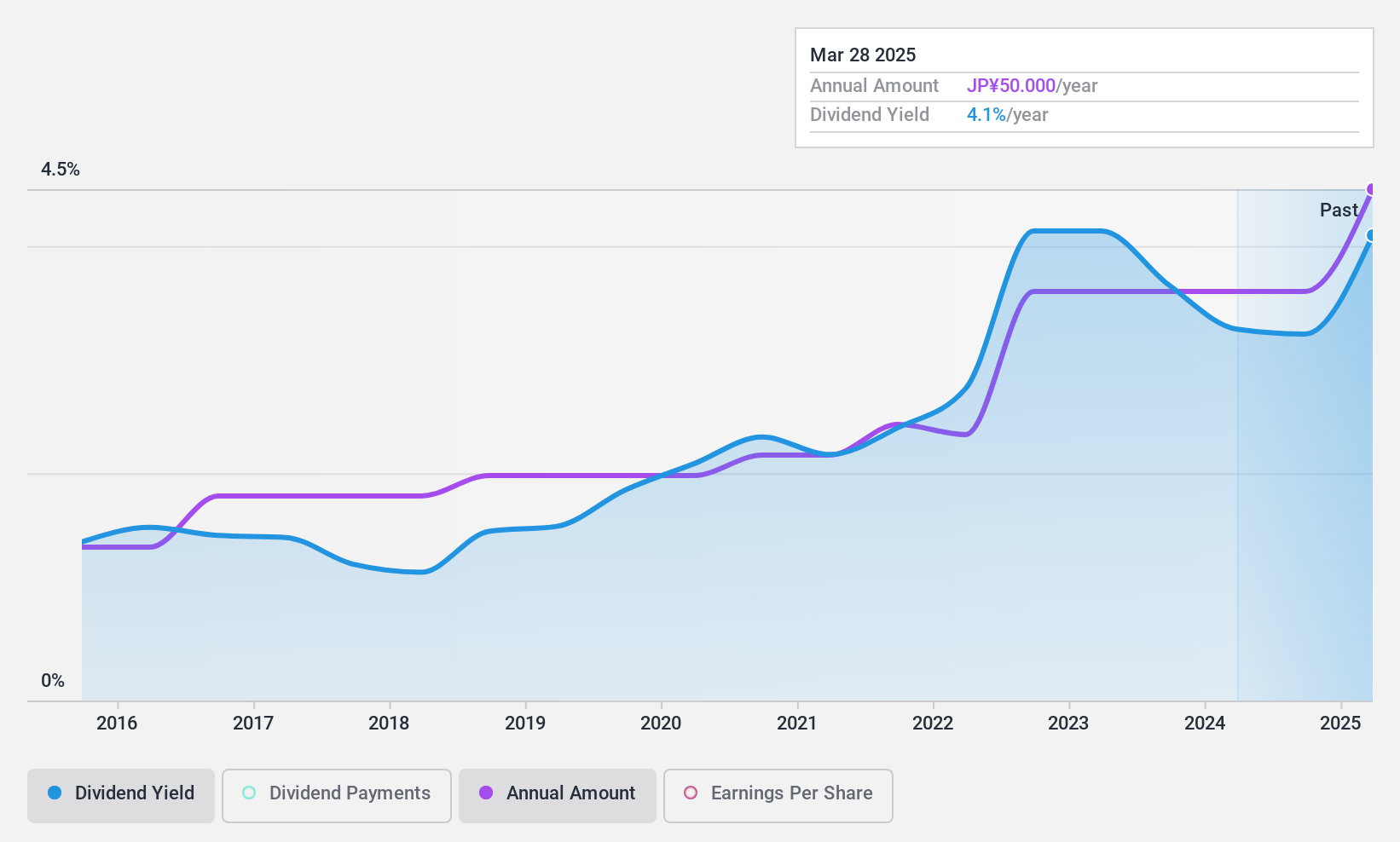

Nihon Parkerizing (TSE:4095)

Simply Wall St Dividend Rating: ★★★★★★

Overview: Nihon Parkerizing Co., Ltd. manufactures and supplies surface treatment chemicals both in Japan and internationally, with a market cap of ¥151.72 billion.

Operations: Nihon Parkerizing Co., Ltd. generates revenue through its core business of manufacturing and supplying surface treatment chemicals, serving both domestic and international markets.

Dividend Yield: 3.8%

Nihon Parkerizing offers a strong dividend profile with a 3.85% yield, ranking in the top 25% of JP market payers. Dividends are well-covered by earnings and cash flows, with payout ratios of 17.3% and 60%, respectively. The company has maintained stable and growing dividends over the past decade, supported by an 18.7% earnings growth last year. Recent share buybacks totaling ¥6.15 billion highlight management's commitment to returning value to shareholders amidst undervaluation concerns.

- Navigate through the intricacies of Nihon Parkerizing with our comprehensive dividend report here.

- Our valuation report here indicates Nihon Parkerizing may be undervalued.

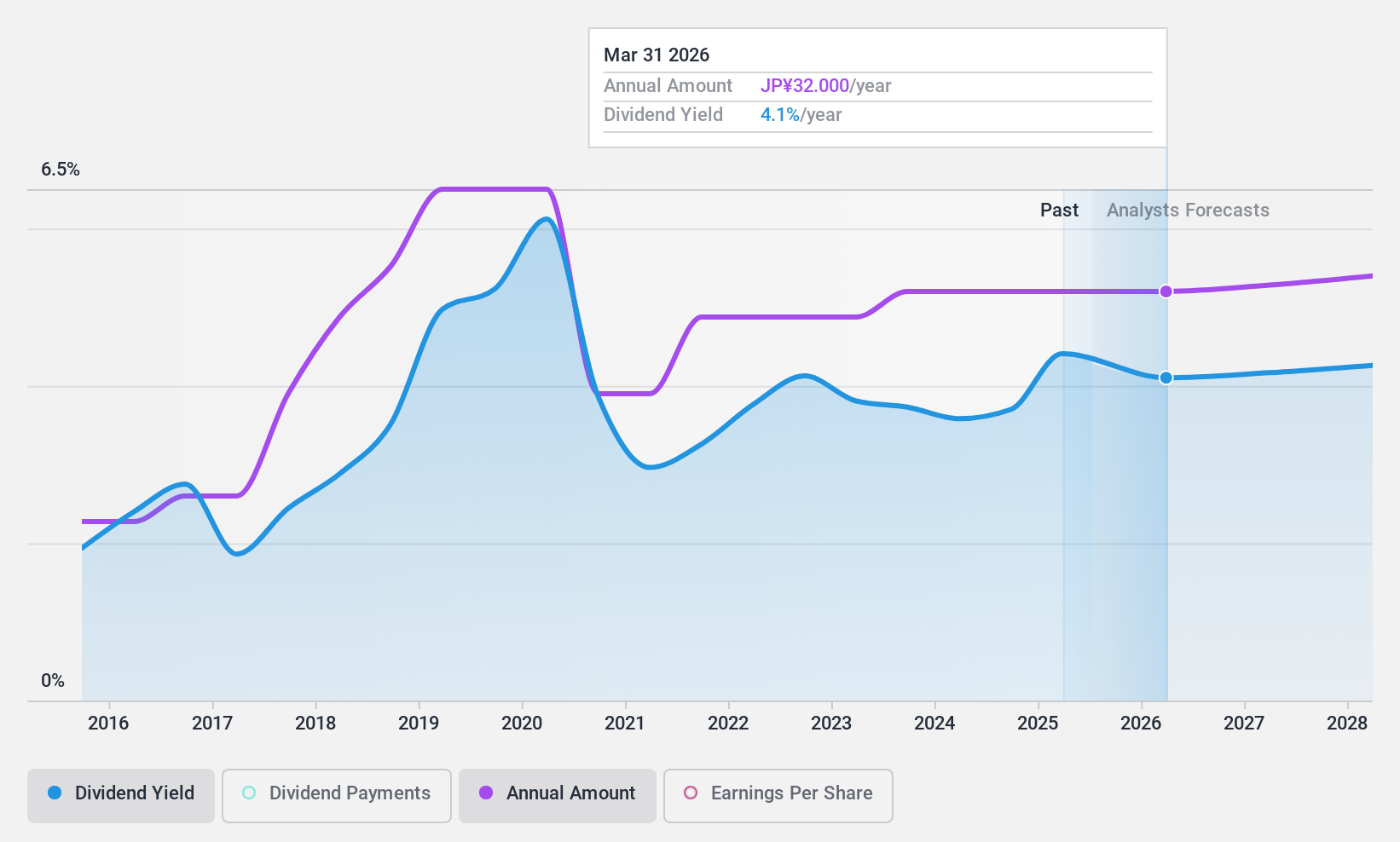

Mitsubishi Chemical Group (TSE:4188)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Mitsubishi Chemical Group Corporation is a global provider of performance products, chemicals, industrial gases, and health care products with a market cap of ¥1.10 trillion.

Operations: Mitsubishi Chemical Group Corporation's revenue is primarily derived from its Industrial Gases segment at ¥1.30 billion, Specialty Materials at ¥1.26 billion, Basic Materials & Polymers at ¥997.78 million, Pharma at ¥448.55 million, and MMA & Derivatives at ¥345.40 million.

Dividend Yield: 4.1%

Mitsubishi Chemical Group's dividend yield of 4.12% ranks in the top 25% of JP market payers, supported by a sustainable payout ratio of 60.6%. However, dividends have been volatile over the past decade despite being well-covered by cash flows with a low cash payout ratio of 22.5%. Recent earnings showed decreased net income and profit margins compared to last year, while strategic divestments like Mitsubishi Tanabe Pharma may impact future financial stability and dividend reliability.

- Get an in-depth perspective on Mitsubishi Chemical Group's performance by reading our dividend report here.

- Our valuation report unveils the possibility Mitsubishi Chemical Group's shares may be trading at a discount.

Key Takeaways

- Discover the full array of 1971 Top Dividend Stocks right here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Nihon Parkerizing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4095

Nihon Parkerizing

Engages in the manufacture and supply of surface treatment chemicals in Japan and internationally.

Flawless balance sheet average dividend payer.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Salesforce Stock: AI-Fueled Growth Is Real — But Can Margins Stay This Strong?

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)