Advertisement

- Taiwan

- /

- Electrical

- /

- TPEX:6222

Is Soaring TechnologyLtd (GTSM:6222) A Future Multi-bagger?

To find a multi-bagger stock, what are the underlying trends we should look for in a business? Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. So when we looked at Soaring TechnologyLtd (GTSM:6222) and its trend of ROCE, we really liked what we saw.

Return On Capital Employed (ROCE): What is it?

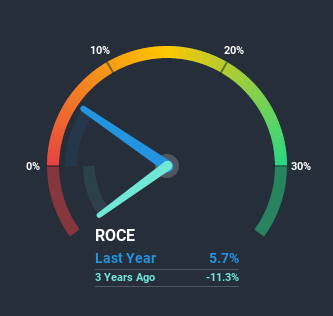

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Soaring TechnologyLtd is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.057 = NT$18m ÷ (NT$405m - NT$100m) (Based on the trailing twelve months to September 2020).

Therefore, Soaring TechnologyLtd has an ROCE of 5.7%. Ultimately, that's a low return and it under-performs the Tech industry average of 12%.

View our latest analysis for Soaring TechnologyLtd

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of Soaring TechnologyLtd, check out these free graphs here.

How Are Returns Trending?

Soaring TechnologyLtd has broken into the black (profitability) and we're sure it's a sight for sore eyes. The company was generating losses five years ago, but has managed to turn it around and as we saw earlier is now earning 5.7%, which is always encouraging. Interestingly, the capital employed by the business has remained relatively flat, so these higher returns are either from prior investments paying off or increased efficiencies. So while we're happy that the business is more efficient, just keep in mind that could mean that going forward the business is lacking areas to invest internally for growth. Because in the end, a business can only get so efficient.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 25%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. So shareholders would be pleased that the growth in returns has mostly come from underlying business performance.

The Bottom Line On Soaring TechnologyLtd's ROCE

To bring it all together, Soaring TechnologyLtd has done well to increase the returns it's generating from its capital employed. And since the stock has fallen 32% over the last five years, there might be an opportunity here. With that in mind, we believe the promising trends warrant this stock for further investigation.

One more thing: We've identified 3 warning signs with Soaring TechnologyLtd (at least 1 which doesn't sit too well with us) , and understanding these would certainly be useful.

While Soaring TechnologyLtd isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

When trading Soaring TechnologyLtd or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TPEX:6222

Li Hsuan Development & Construction

Manufactures and sells LED lighting products in Taiwan.

Flawless balance sheet with slight risk.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2542.9% undervalued

64 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$487.1% overvalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

47 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$829.5% undervalued

26 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

BR

Bravosatya on Meta Platforms ·

Meta Platforms - Zuckerberg’s investment decisions are impulsive or Prudent?

Fair Value:US$730.0216.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JU

julio on FIGS ·

Figs valuation

Fair Value:US$14.3930.2% undervalued

21 followersusers have followed this narrative

6 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on MIRAI ·

Improving NOI growth visibility on wider rent gap

Fair Value:JP¥77.06k45.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75030.3% undervalued

80 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9634.1% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative