Advertisement

- Taiwan

- /

- Communications

- /

- TPEX:4979

Undiscovered Gems In Asia March 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate heightened uncertainty, with the U.S. Federal Reserve holding interest rates steady and mixed economic signals emerging from major economies, investors are increasingly turning their attention to Asia's dynamic landscape. In this environment, identifying promising stocks involves looking for companies that demonstrate resilience and adaptability amidst shifting economic conditions and geopolitical factors.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| QuickLtd | 0.77% | 10.02% | 16.34% | ★★★★★★ |

| Kyoritsu Electric | 7.58% | 3.45% | 12.53% | ★★★★★★ |

| Hong Tai Electric Industrial | NA | 10.19% | 6.78% | ★★★★★★ |

| Great China Metal Ind | NA | 2.41% | -4.04% | ★★★★★★ |

| Ad-Sol Nissin | NA | 7.54% | 9.63% | ★★★★★★ |

| Konishi | 0.16% | -0.13% | 13.54% | ★★★★★★ |

| Transcend Information | NA | -5.04% | 7.79% | ★★★★★★ |

| Shenzhen Jdd Tech New Material | NA | 19.07% | 20.23% | ★★★★★★ |

| Nippon Ski Resort DevelopmentLtd | 40.39% | 10.24% | 42.77% | ★★★★★☆ |

| New Asia Construction & Development | 56.11% | 6.68% | 23.77% | ★★★★☆☆ |

We'll examine a selection from our screener results.

Shandong Jincheng Pharmaceutical Group (SZSE:300233)

Simply Wall St Value Rating: ★★★★★☆

Overview: Shandong Jincheng Pharmaceutical Group Co., Ltd focuses on the research, development, production, marketing, and sale of Cephalosporin intermediates both in China and internationally with a market cap of CN¥8.25 billion.

Operations: The company generates revenue primarily from the sale of Cephalosporin intermediates. It has a market cap of CN¥8.25 billion, reflecting its position in the pharmaceutical sector.

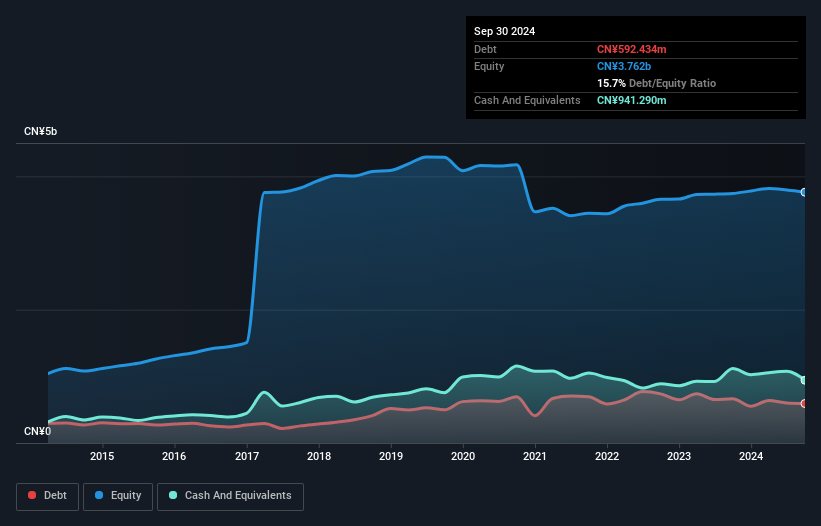

Shandong Jincheng Pharmaceutical Group has been making waves with its impressive earnings growth of 31% over the past year, outpacing the broader pharmaceutical industry which saw a -2.4% change. The company boasts high-quality earnings and maintains an impressive interest coverage ratio of 54 times, indicating strong financial health. Despite a rise in debt-to-equity from 11.6% to 15.7% over five years, it holds more cash than total debt, ensuring stability. Recent announcements include a special dividend payout plan for shareholders, reflecting confidence in their financial position and rewarding investors amidst market volatility.

- Click to explore a detailed breakdown of our findings in Shandong Jincheng Pharmaceutical Group's health report.

Understand Shandong Jincheng Pharmaceutical Group's track record by examining our Past report.

LuxNet (TPEX:4979)

Simply Wall St Value Rating: ★★★★★★

Overview: LuxNet Corporation, along with its subsidiaries, specializes in the manufacturing, processing, and sale of electric and optical communication components in Taiwan with a market capitalization of NT$27.46 billion.

Operations: LuxNet's revenue from optical communication system active components is NT$3.45 billion. The company's market capitalization stands at NT$27.46 billion.

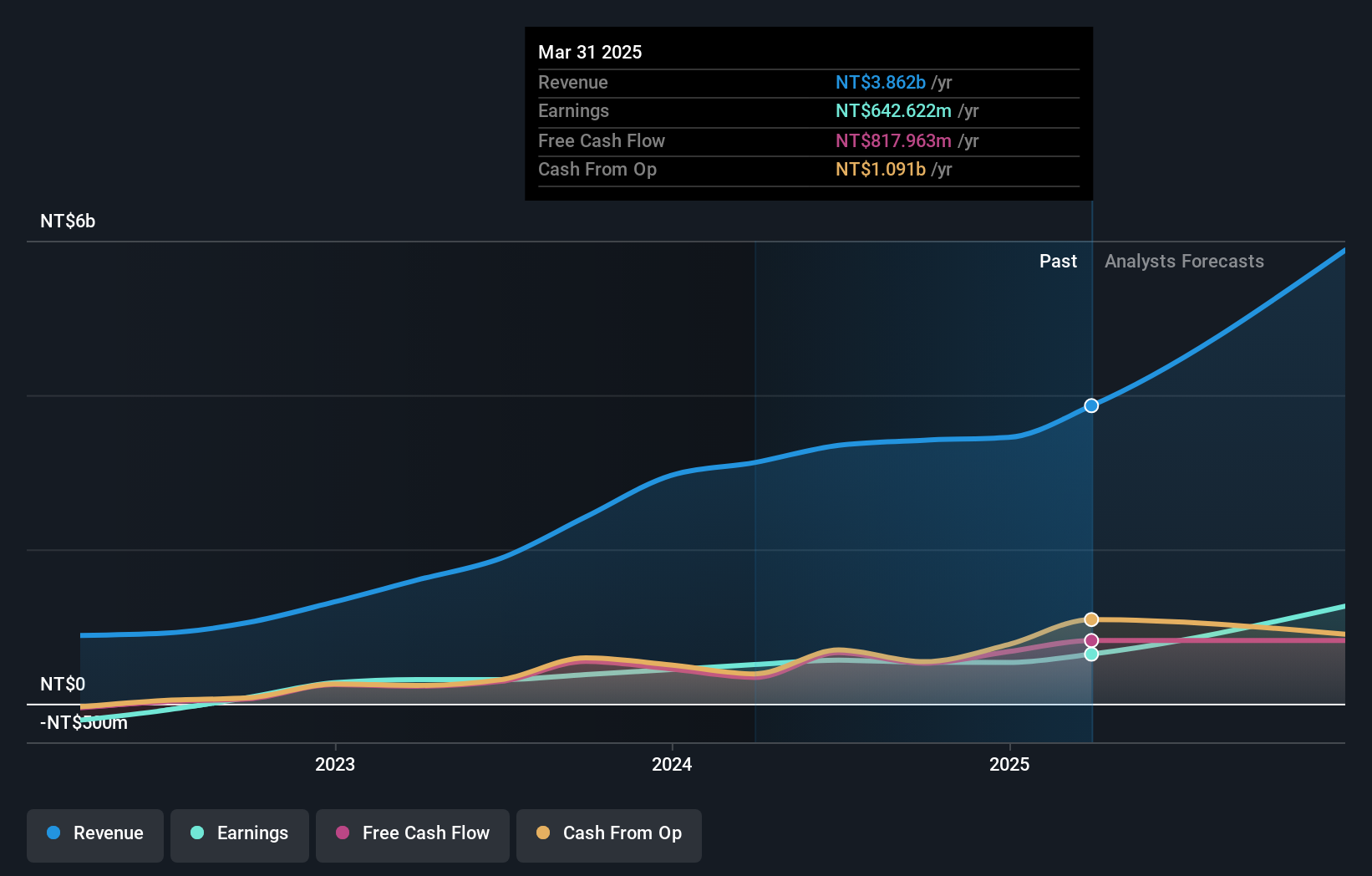

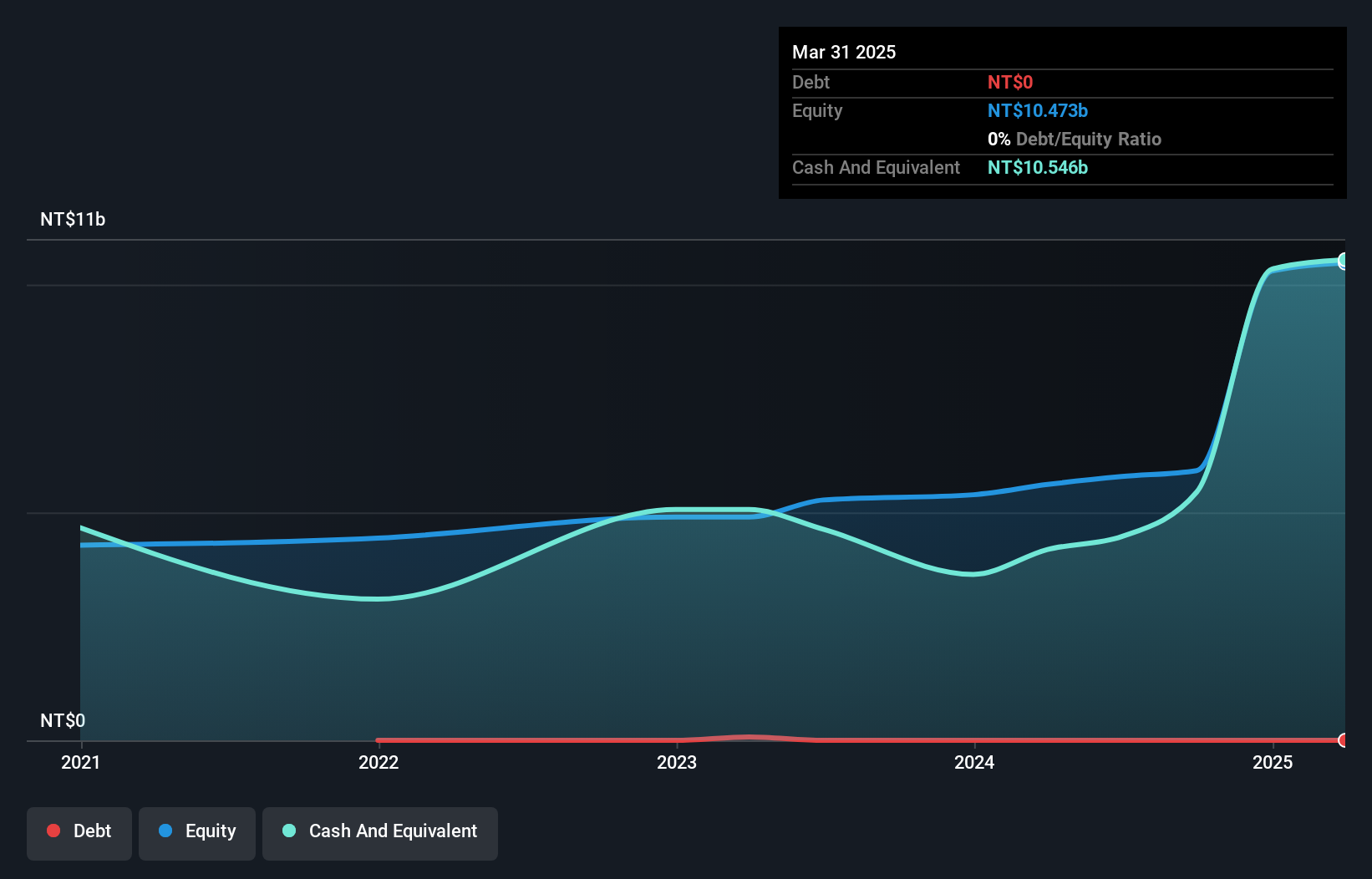

LuxNet, a nimble player in the communications sector, has shown impressive financial resilience. Its earnings surged by 20.5% last year, outpacing the industry average of 1.7%, and it boasts high-quality earnings. The company holds more cash than its total debt, reflecting a robust balance sheet with a reduced debt-to-equity ratio from 57.1% to 21.9% over five years. Despite recent share price volatility, LuxNet remains profitable with positive free cash flow and sufficient interest coverage, ensuring stability in operations without immediate liquidity concerns for investors looking at this promising entity in Asia's market landscape.

- Delve into the full analysis health report here for a deeper understanding of LuxNet.

Explore historical data to track LuxNet's performance over time in our Past section.

LINE Pay Taiwan (TWSE:7722)

Simply Wall St Value Rating: ★★★★★★

Overview: LINE Pay Taiwan Limited operates in the third-party payment sector in Taiwan and has a market capitalization of NT$48.96 billion.

Operations: The company generates revenue primarily through transaction fees from its third-party payment services. It incurs costs related to technology infrastructure and customer service operations.

LINE Pay Taiwan, a promising player in the digital payments sector, has shown notable financial progress. Recently reporting sales of TWD 6.3 billion, up from TWD 4.9 billion the previous year, the company also saw net income rise to TWD 647 million from TWD 482 million. Earnings per share increased to TWD 10.67 from TWD 8.09, reflecting robust growth potential. Despite recent service disruptions in Japan that were swiftly resolved without major impact, LINE Pay Taiwan is expanding with a new subsidiary investment of TWD 5 billion and inclusion in the Taiwan TAIEX Index highlights its growing market presence and future prospects.

- Get an in-depth perspective on LINE Pay Taiwan's performance by reading our health report here.

Assess LINE Pay Taiwan's past performance with our detailed historical performance reports.

Make It Happen

- Dive into all 2644 of the Asian Undiscovered Gems With Strong Fundamentals we have identified here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TPEX:4979

LuxNet

Manufactures, processes, and sells electric and optical communication components in Taiwan.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality Assets, Cautious Expansion and Commodity Super-cycle To Deliver Steady Revenue Growth

Fair Value US$20.44|5.0% undervalued

ST

Equity Analyst and Writer

Tullow Oil's Share Price Could Soar Up to 135% if Oil Holds at $70

Fair Value UK£0.45|63.8% undervalued

OI

Community Contributor