- Taiwan

- /

- Construction

- /

- TWSE:3703

Continental Holdings (TWSE:3703) Is Paying Out Less In Dividends Than Last Year

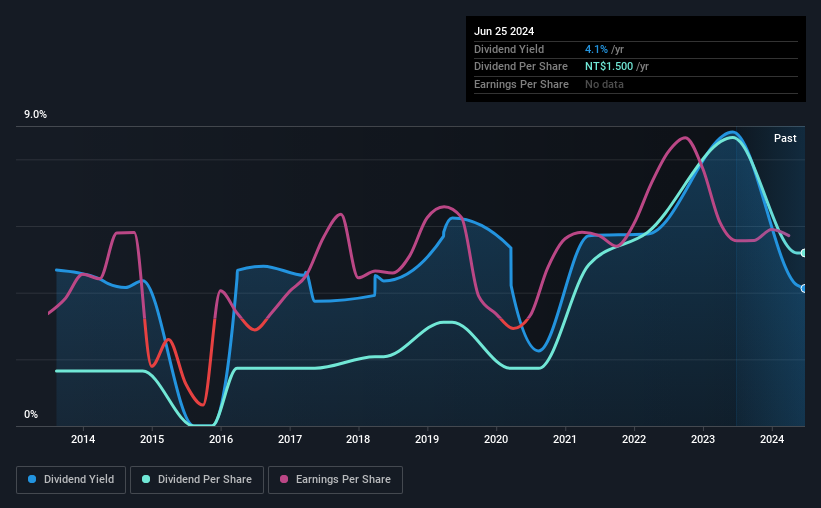

Continental Holdings Corporation's (TWSE:3703) dividend is being reduced from last year's payment covering the same period to NT$1.50 on the 31st of July. Despite the cut, the dividend yield of 4.1% will still be comparable to other companies in the industry.

View our latest analysis for Continental Holdings

Continental Holdings Doesn't Earn Enough To Cover Its Payments

Solid dividend yields are great, but they only really help us if the payment is sustainable. The last dividend made up quite a large portion of free cash flows, and this was made worse by the lack of free cash flows. We think that this practice can make the dividend quite risky in the future.

If the company can't turn things around, EPS could fall by 5.8% over the next year. Assuming the dividend continues along recent trends, we believe the payout ratio could reach 96%, which could put the dividend under pressure if earnings don't start to improve.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2014, the dividend has gone from NT$0.476 total annually to NT$1.50. This means that it has been growing its distributions at 12% per annum over that time. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

Dividend Growth Is Doubtful

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Continental Holdings has seen earnings per share falling at 5.8% per year over the last five years. A modest decline in earnings isn't great, and it makes it quite unlikely that the dividend will grow in the future unless that trend can be reversed.

The Dividend Could Prove To Be Unreliable

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. The track record isn't great, and the payments are a bit high to be considered sustainable. Overall, we don't think this company has the makings of a good income stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Just as an example, we've come across 2 warning signs for Continental Holdings you should be aware of, and 1 of them shouldn't be ignored. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:3703

Continental Holdings

Engages in civil and building construction, real estate development, environmental project development, and water treatment businesses in Taiwan and internationally.

Average dividend payer with mediocre balance sheet.

Market Insights

Community Narratives