- Taiwan

- /

- Electronic Equipment and Components

- /

- TWSE:3090

Undiscovered Gems with Potential in November 2024

Reviewed by Simply Wall St

As global markets react to a "red sweep" in the U.S. elections, small-cap stocks have captured attention with the Russell 2000 Index leading gains despite not yet reaching record highs. This environment of anticipated economic growth and regulatory changes presents an intriguing backdrop for identifying undiscovered gems—stocks that demonstrate resilience, innovation, and potential for growth amid evolving market conditions.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| C&D Property Management Group | 1.32% | 37.15% | 41.55% | ★★★★★★ |

| Morris State Bancshares | 17.84% | 4.83% | 6.58% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| MAPFRE Middlesea | NA | 14.56% | 1.77% | ★★★★★☆ |

| Bakrie & Brothers | 22.66% | 7.78% | 13.50% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| Practic | NA | 3.63% | 6.85% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

Mitsubishi Shokuhin (TSE:7451)

Simply Wall St Value Rating: ★★★★★★

Overview: Mitsubishi Shokuhin Co., Ltd. operates as a wholesaler of processed foods, frozen and chilled foods, alcoholic beverages, and confectioneries both in Japan and internationally, with a market cap of ¥210.59 billion.

Operations: The company generates revenue primarily through the wholesale distribution of processed foods, frozen and chilled foods, alcoholic beverages, and confectioneries. The net profit margin is a key financial metric to consider when evaluating its profitability.

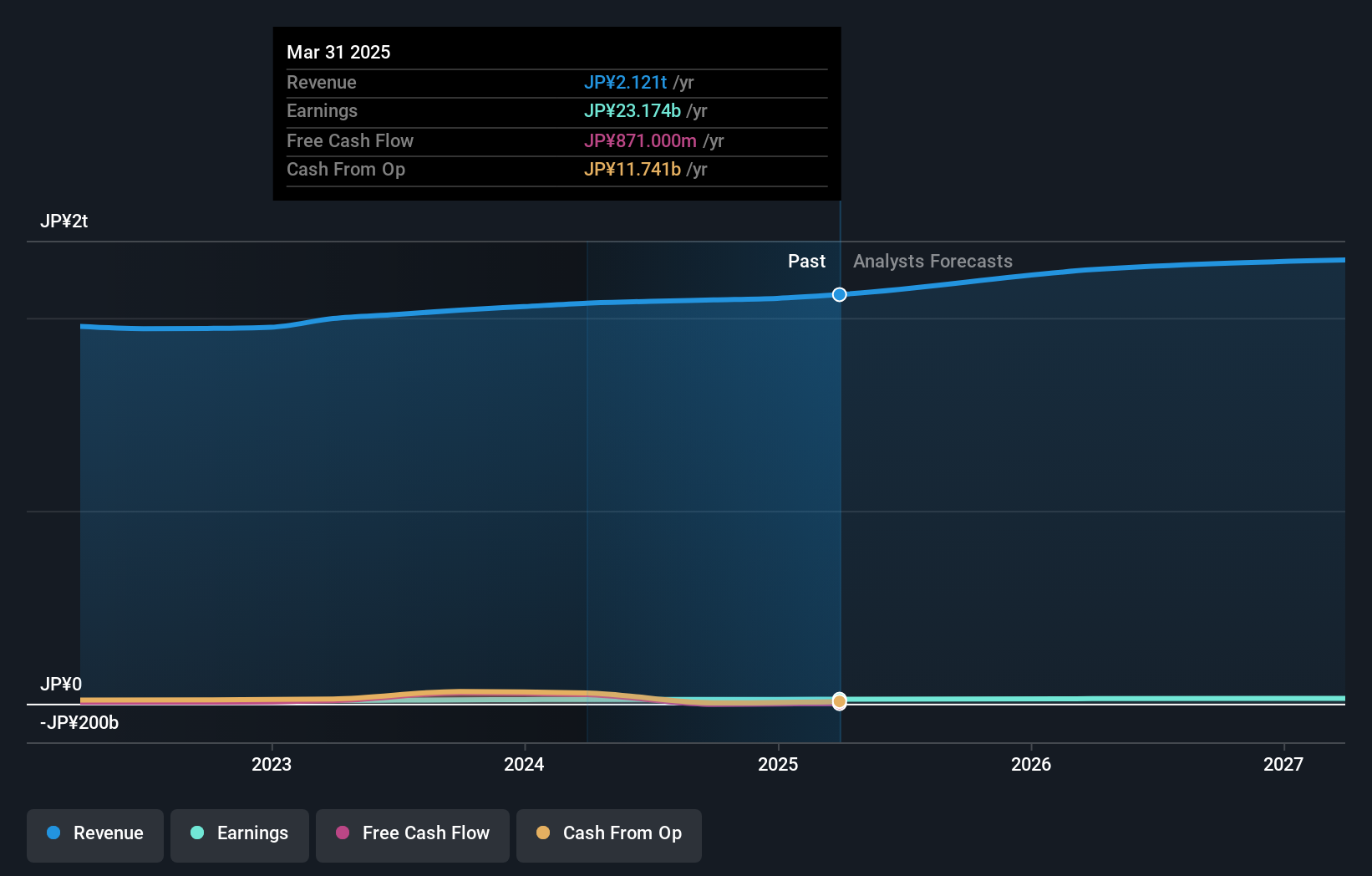

Mitsubishi Shokuhin showcases a compelling profile with its debt-free status over the last five years, ensuring no worries about interest payments. This company has demonstrated robust earnings growth of 16.9% annually over the past five years, though it slightly lags behind industry peers with a recent 13.2% growth compared to the Consumer Retailing industry's 14.8%. Trading at approximately 3.3% below its estimated fair value, Mitsubishi Shokuhin appears attractively priced against competitors and industry standards. The company anticipates net sales of ¥2,130 billion for FY2025 and plans to increase dividends from ¥80 to ¥90 per share by December 2024.

Hold-Key Electric Wire & Cable (TWSE:1618)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Hold-Key Electric Wire & Cable Co., Ltd. operates in Taiwan, focusing on the manufacturing, importing, and selling of cable products with a market capitalization of approximately NT$8.64 billion.

Operations: Hold-Key Electric Wire & Cable generates revenue primarily from its wire and cable segment, amounting to NT$4.66 billion.

Hold-Key Electric Wire & Cable, a smaller player in the electrical industry, has shown impressive growth with earnings surging by 112.9% over the past year, outpacing the industry's modest 0.1%. The company's price-to-earnings ratio of 17.2x suggests it is valued attractively compared to the TW market's 21.2x benchmark. Despite a rise in its debt-to-equity ratio from 0% to 9.8% over five years, Hold-Key maintains more cash than total debt, indicating financial stability. Recent results reveal net income for Q2 at TWD175 million and EPS at TWD0.91, reflecting strong operational performance and potential for continued success.

Nichidenbo (TWSE:3090)

Simply Wall St Value Rating: ★★★★★★

Overview: Nichidenbo Corporation is involved in the global distribution of electronic components, with a market cap of NT$13.29 billion.

Operations: Nichidenbo Corporation generates revenue through the global distribution of electronic components. The company has a market capitalization of NT$13.29 billion.

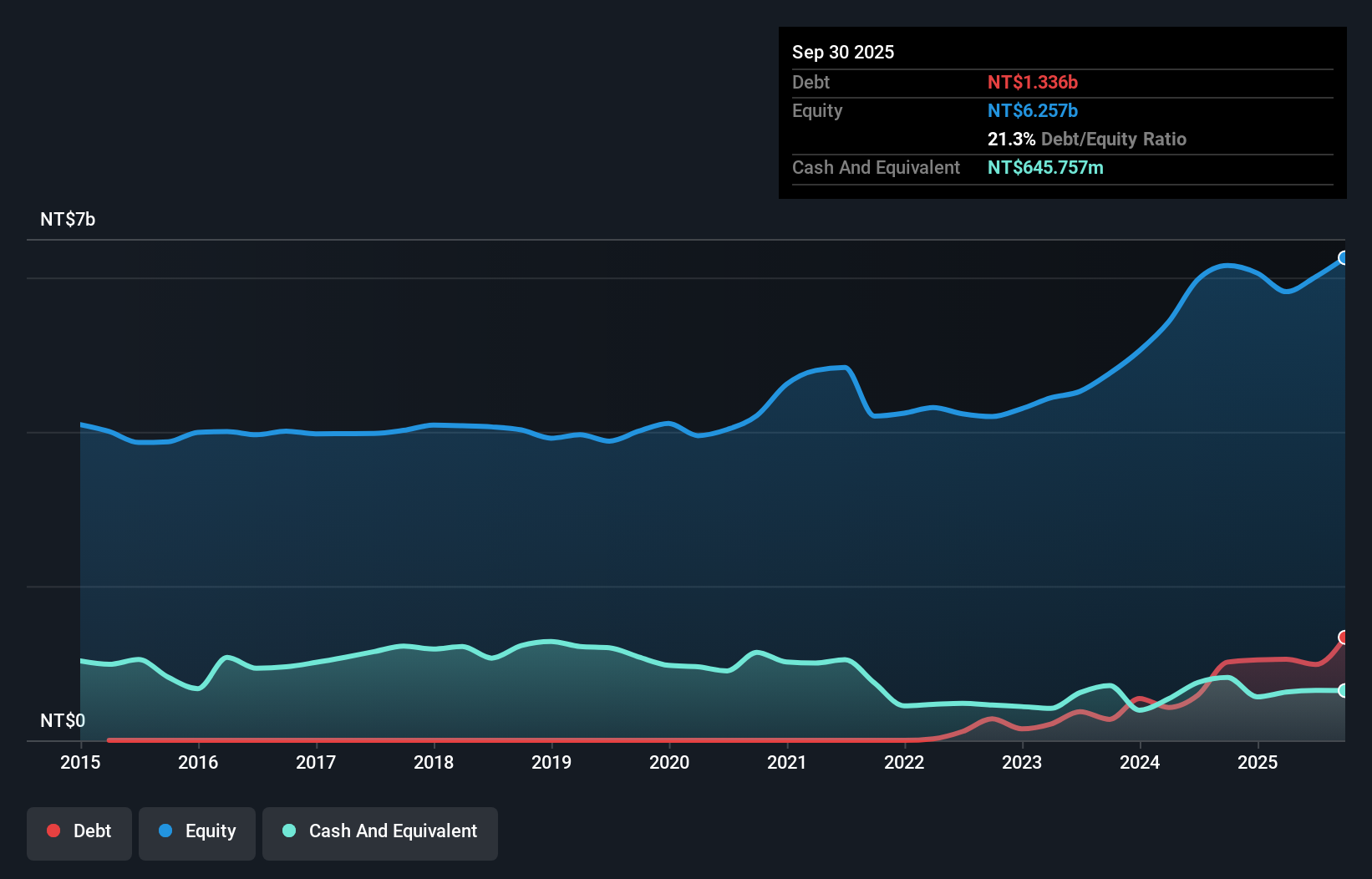

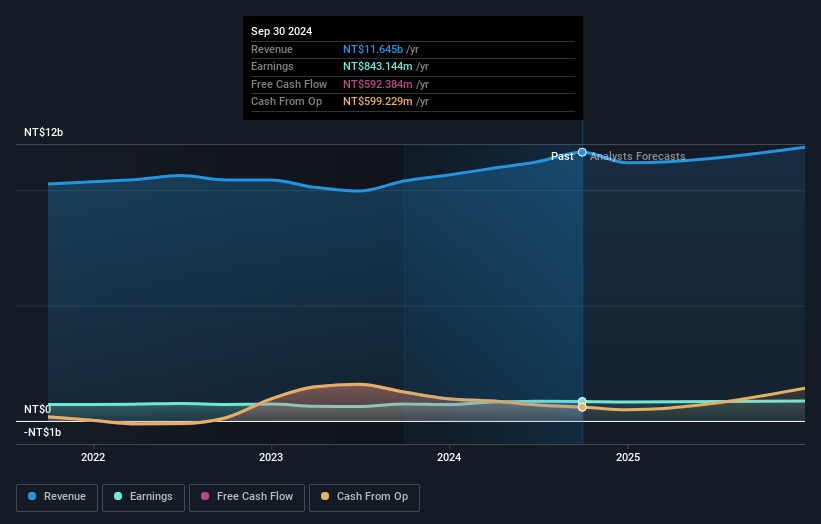

Nichidenbo, a notable player in the electronics sector, has demonstrated impressive earnings growth of 14.2% over the past year, surpassing the industry average of 5.8%. The company's debt management appears robust, with a reduction in its debt-to-equity ratio from 38.8% to 32.4% over five years and interest payments well-covered by EBIT at an impressive 41.2x coverage. Recent financial results show sales for Q3 at TWD 3,294 million compared to TWD 2,879 million last year; however, net income slightly dipped to TWD 259 million from TWD 267 million despite increased nine-month sales reaching TWD 8,987 million from TWD 7,998 million previously.

- Unlock comprehensive insights into our analysis of Nichidenbo stock in this health report.

Gain insights into Nichidenbo's historical performance by reviewing our past performance report.

Seize The Opportunity

- Dive into all 4643 of the Undiscovered Gems With Strong Fundamentals we have identified here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nichidenbo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:3090

Nichidenbo

Engages in the distribution of electronic components worldwide.

Flawless balance sheet with solid track record and pays a dividend.