- Philippines

- /

- Food and Staples Retail

- /

- PSE:KEEPR

Uncovering Hidden Opportunities Among Undiscovered Gems In November 2024

Reviewed by Simply Wall St

As global markets react to the recent U.S. election results, with major indices like the Russell 2000 showing significant gains, investors are eyeing potential benefits from anticipated economic policies that could favor small-cap stocks. Amidst this backdrop of optimism and strategic shifts, identifying promising small-cap opportunities involves looking for companies with strong fundamentals and growth potential that may not yet be fully appreciated by the broader market.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Franklin Financial Services | 222.36% | 5.55% | -1.86% | ★★★★★★ |

| Morris State Bancshares | 17.84% | 4.83% | 6.58% | ★★★★★★ |

| FRoSTA | 8.18% | 4.36% | 16.00% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Arab Banking Corporation (B.S.C.) | 213.15% | 18.58% | 29.63% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

Sonaecom SGPS (ENXTLS:SNC)

Simply Wall St Value Rating: ★★★★★★

Overview: Sonaecom SGPS, S.A. operates globally in the technology, media, and telecommunications sectors through its subsidiaries and has a market capitalization of €764.42 million.

Operations: Sonaecom SGPS generates revenue primarily from its media segment, contributing €16.33 million, and technology segment, adding €3.15 million.

Sonaecom SGPS, a nimble player in the telecom sector, shows promise with its price-to-earnings ratio at 9.7x, undercutting the Portuguese market's 12.7x. This company has outpaced industry peers with an impressive earnings growth of 73.5% over the past year, significantly higher than the Wireless Telecom industry's 2.7%. Sonaecom boasts high-quality earnings and is debt-free now compared to a debt-to-equity ratio of 0.6 five years ago, which underscores financial prudence despite share price volatility recently observed over three months. While not free cash flow positive currently, its profitability suggests potential for future stability and growth.

- Get an in-depth perspective on Sonaecom SGPS' performance by reading our health report here.

Assess Sonaecom SGPS' past performance with our detailed historical performance reports.

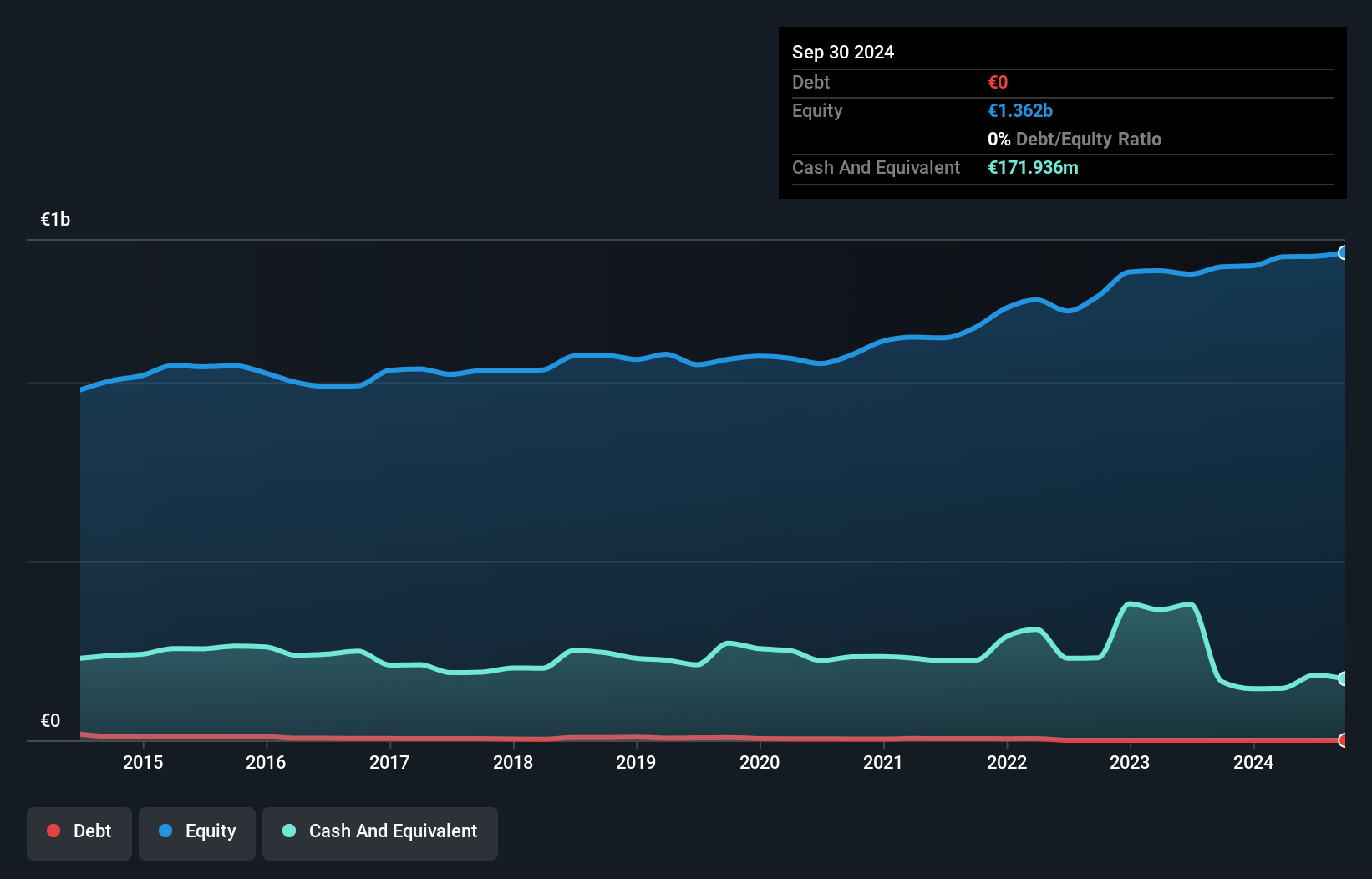

Keepers Holdings (PSE:KEEPR)

Simply Wall St Value Rating: ★★★★★★

Overview: The Keepers Holdings, Inc. is an investment holding company involved in the distribution of liquor, wine, and specialty beverages in the Philippines with a market capitalization of ₱30.90 billion.

Operations: Keepers Holdings generates revenue primarily through the distribution of liquor, wine, and specialty beverages in the Philippines. The company's financial performance is highlighted by its net profit margin trend over recent periods.

Keepers Holdings, a small company in the consumer retailing sector, has been making strides with its earnings growing by 34% over the past year. This growth outpaces the industry average of 8%. Notably, Keepers is debt-free now, a significant improvement from five years ago when its debt to equity ratio was 42.8%. The stock trades at a compelling valuation, approximately 62% below estimated fair value. Recent financial results show sales of PHP 11.71 billion and net income of PHP 2.17 billion for nine months ending September 2024. A potential acquisition of Booze On-Line could further enhance its market position.

- Click here and access our complete health analysis report to understand the dynamics of Keepers Holdings.

Evaluate Keepers Holdings' historical performance by accessing our past performance report.

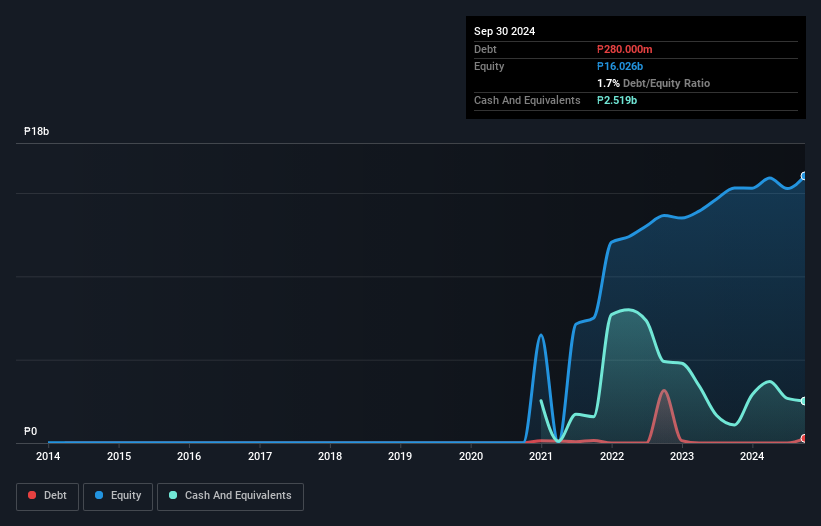

Ditto (Thailand) (SET:DITTO)

Simply Wall St Value Rating: ★★★★★★

Overview: Ditto (Thailand) Public Company Limited specializes in distributing data and document management solutions in Thailand, with a market capitalization of THB13.11 billion.

Operations: Ditto (Thailand) generates revenue primarily from three segments: Technology Engineering Services (THB926.39 million), Data and Document Management Solutions (THB709.59 million), and Photocopiers, Printers, and Technology Products (THB551.91 million).

Ditto, a dynamic player in Thailand's electronics sector, has showcased remarkable financial health with its debt-to-equity ratio plummeting from 65.1% to 0.08% over five years, suggesting prudent financial management. Its earnings growth of 36.7% last year outpaced the industry average of 12%, highlighting robust performance and potential for future expansion. Despite recent shareholder dilution, Ditto remains free cash flow positive and trades at a slight discount of 2.6% below estimated fair value, hinting at possible undervaluation in the market. The company’s high-quality earnings and strong interest coverage further underscore its solid foundation amidst market volatility.

Key Takeaways

- Discover the full array of 4666 Undiscovered Gems With Strong Fundamentals right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Keepers Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About PSE:KEEPR

Keepers Holdings

An investment holding company, engages in the liquor, wine, and specialty beverage distribution business in the Philippines.

Outstanding track record with flawless balance sheet and pays a dividend.