- Singapore

- /

- Paper and Forestry Products

- /

- SGX:BEI

Why It Might Not Make Sense To Buy LHT Holdings Limited (SGX:BEI) For Its Upcoming Dividend

It looks like LHT Holdings Limited (SGX:BEI) is about to go ex-dividend in the next 4 days. The ex-dividend date is two business days before a company's record date in most cases, which is the date on which the company determines which shareholders are entitled to receive a dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. Thus, you can purchase LHT Holdings' shares before the 19th of May in order to receive the dividend, which the company will pay on the 30th of May.

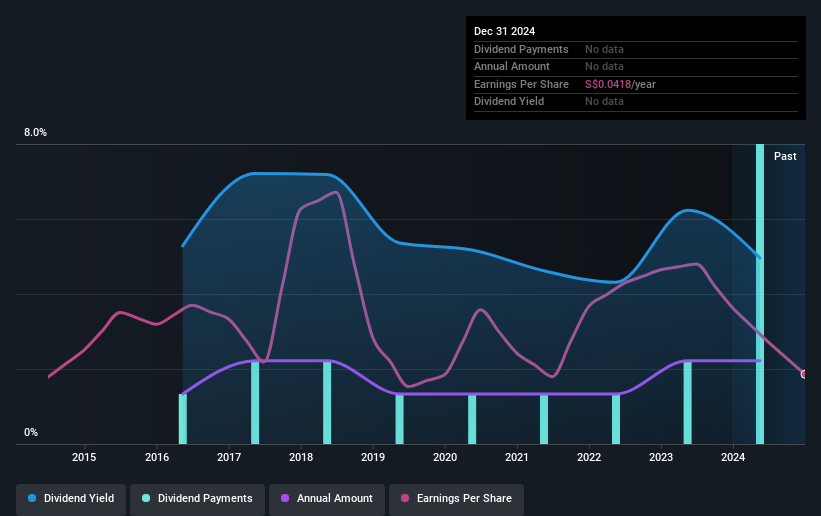

The company's next dividend payment will be S$0.05 per share. Last year, in total, the company distributed S$0.05 to shareholders. Based on the last year's worth of payments, LHT Holdings stock has a trailing yield of around 5.3% on the current share price of S$0.95. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. LHT Holdings paid out 120% of profit in the past year, which we think is typically not sustainable unless there are mitigating characteristics such as unusually strong cash flow or a large cash balance. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. Over the last year, it paid out dividends equivalent to 364% of what it generated in free cash flow, a disturbingly high percentage. It's pretty hard to pay out more than you earn, so we wonder how LHT Holdings intends to continue funding this dividend, or if it could be forced to cut the payment.

LHT Holdings does have a large net cash position on the balance sheet, which could fund large dividends for a time, if the company so chose. Still, smart investors know that it is better to assess dividends relative to the cash and profit generated by the business. Paying dividends out of cash on the balance sheet is not long-term sustainable.

As LHT Holdings's dividend was not well covered by either earnings or cash flow, we would be concerned that this dividend could be at risk over the long term.

Check out our latest analysis for LHT Holdings

Click here to see how much of its profit LHT Holdings paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies that aren't growing their earnings can still be valuable, but it is even more important to assess the sustainability of the dividend if it looks like the company will struggle to grow. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. With that in mind, we're not enthused to see that LHT Holdings's earnings per share have remained effectively flat over the past five years. We'd take that over an earnings decline any day, but in the long run, the best dividend stocks all grow their earnings per share. Minimal earnings growth, combined with concerningly high payout ratios suggests that LHT Holdings is unlikely to grow the dividend much in future, and indeed the payment could be vulnerable to a cut.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the past 10 years, LHT Holdings has increased its dividend at approximately 6.0% a year on average.

Final Takeaway

Has LHT Holdings got what it takes to maintain its dividend payments? LHT Holdings is paying out an uncomfortably high percentage of both earnings and cash flow as dividends, at the same time as its earnings per share are struggling to grow. Overall it doesn't look like the most suitable dividend stock for a long-term buy and hold investor.

So if you're still interested in LHT Holdings despite it's poor dividend qualities, you should be well informed on some of the risks facing this stock. For example, we've found 4 warning signs for LHT Holdings (2 are a bit unpleasant!) that deserve your attention before investing in the shares.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:BEI

LHT Holdings

Manufactures, imports, exports, and trades in wooden pallets and timber-related products in Singapore, Malaysia, and internationally.

Flawless balance sheet with medium-low risk and pays a dividend.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)