Advertisement

- Singapore

- /

- Consumer Services

- /

- SGX:RQ1

Overseas Education (SGX:RQ1) Is Paying Out Less In Dividends Than Last Year

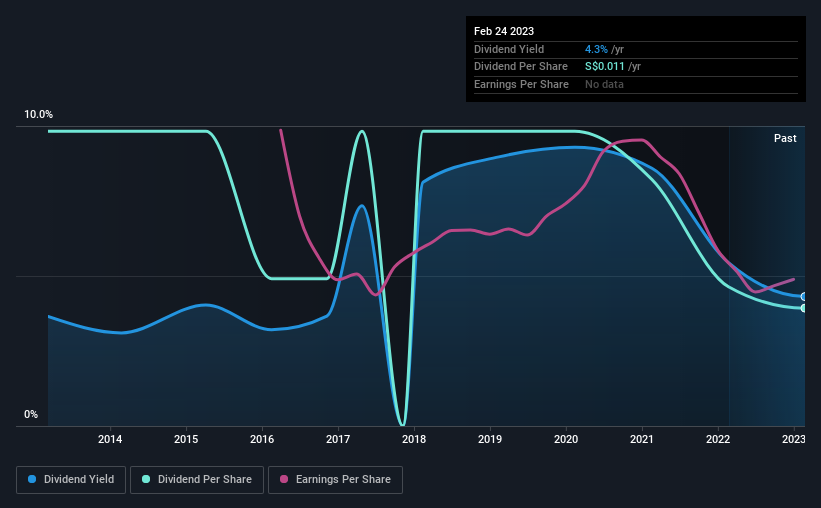

The board of Overseas Education Limited (SGX:RQ1) has announced that the dividend on 19th of May will be reduced by 15% from last year's SGD0.013 to SGD0.011. This means the annual payment is 4.3% of the current stock price, which is above the average for the industry.

See our latest analysis for Overseas Education

Overseas Education's Payment Has Solid Earnings Coverage

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. The last payment made up 87% of earnings, but cash flows were much higher. Since the dividend is just paying out cash to shareholders, we care more about the cash payout ratio from which we can see plenty is being left over for reinvestment in the business.

If the company can't turn things around, EPS could fall by 3.3% over the next year. Assuming the dividend continues along recent trends, we think the payout ratio could reach 86%, which is definitely on the higher side.

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. Since 2013, the annual payment back then was SGD0.0275, compared to the most recent full-year payment of SGD0.011. Doing the maths, this is a decline of about 8.8% per year. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

The Dividend's Growth Prospects Are Limited

Given that the track record hasn't been stellar, we really want to see earnings per share growing over time. In the last five years, Overseas Education's earnings per share has shrunk at approximately 3.3% per annum. Declining earnings will inevitably lead to the company paying a lower dividend in line with lower profits.

Our Thoughts On Overseas Education's Dividend

In summary, dividends being cut isn't ideal, however it can bring the payment into a more sustainable range. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We would be a touch cautious of relying on this stock primarily for the dividend income.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. Case in point: We've spotted 4 warning signs for Overseas Education (of which 1 is a bit unpleasant!) you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:RQ1

Overseas Education

An investment holding company, operates a foreign system school in Singapore.

Adequate balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor