Advertisement

- Singapore

- /

- Professional Services

- /

- SGX:CHZ

New Forecasts: Here's What Analysts Think The Future Holds For HRnetGroup Limited (SGX:CHZ)

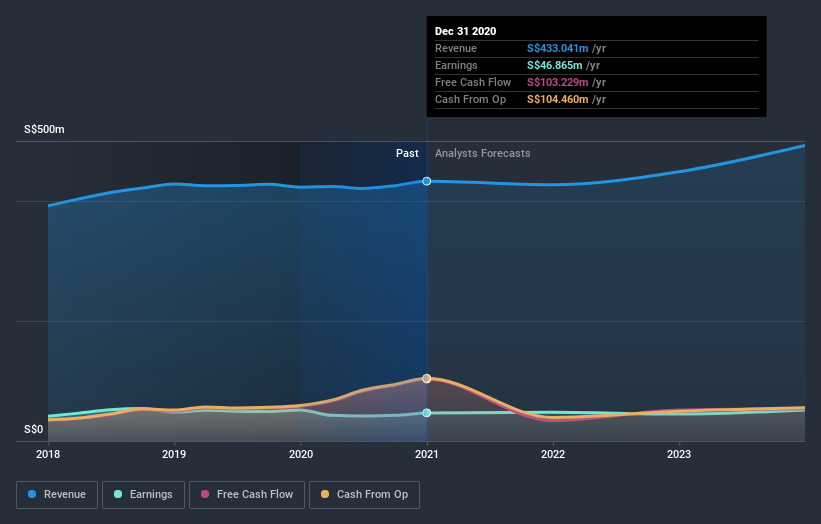

Shareholders in HRnetGroup Limited (SGX:CHZ) may be thrilled to learn that the analysts have just delivered a major upgrade to their near-term forecasts. Consensus estimates suggest investors could expect greatly increased statutory revenues and earnings per share, with the analysts modelling a real improvement in business performance.

Following the upgrade, the latest consensus from HRnetGroup's three analysts is for revenues of S$473m in 2021, which would reflect a solid 9.3% improvement in sales compared to the last 12 months. Per-share earnings are expected to accumulate 3.8% to S$0.049. Prior to this update, the analysts had been forecasting revenues of S$418m and earnings per share (EPS) of S$0.039 in 2021. So we can see there's been a pretty clear increase in analyst sentiment in recent times, with both revenues and earnings per share receiving a decent lift in the latest estimates.

Check out our latest analysis for HRnetGroup

With these upgrades, we're not surprised to see that the analysts have lifted their price target 16% to S$0.64 per share. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on HRnetGroup, with the most bullish analyst valuing it at S$0.72 and the most bearish at S$0.50 per share. This shows there is still some diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. The analysts are definitely expecting HRnetGroup's growth to accelerate, with the forecast 9.3% annualised growth to the end of 2021 ranking favourably alongside historical growth of 4.0% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 11% per year. It seems obvious that, while the future growth outlook is brighter than the recent past, HRnetGroup is expected to grow slower than the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that analysts upgraded their earnings per share estimates for this year, expecting improving business conditions. Fortunately, they also upgraded their revenue estimates, and are forecasting revenues to grow slower than the wider market. Given that the consensus looks almost universally bullish, with a substantial increase to forecasts and a higher price target, HRnetGroup could be worth investigating further.

Using these estimates as a starting point, we've run a discounted cash flow calculation (DCF) on HRnetGroup that suggests the company could be somewhat undervalued. For more information, you can click through to our platform to learn more about our valuation approach.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you’re looking to trade HRnetGroup, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if HRnetGroup might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SGX:CHZ

HRnetGroup

An investment holding company, engages in the recruitment and staffing business in Singapore, Hong Kong, Taiwan, the People’s Republic of China, Japan, South Korea, Malaysia, Thailand, and Indonesia.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|30.1% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|25.6% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|63.2% undervalued

ME

Community Contributor