Is Yangzijiang Shipbuilding (Holdings) (SGX:BS6) A Risky Investment?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Yangzijiang Shipbuilding (Holdings) Ltd. (SGX:BS6) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Yangzijiang Shipbuilding (Holdings)

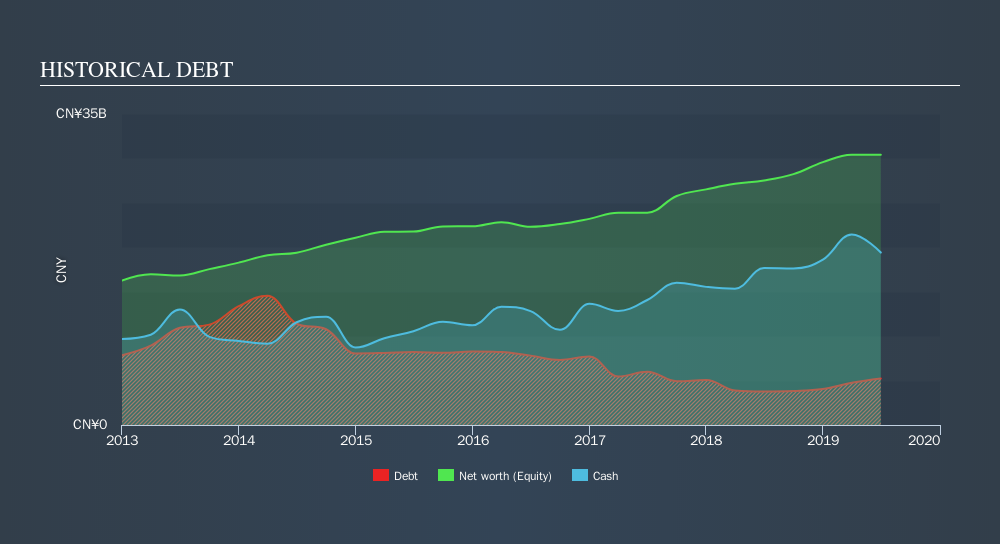

How Much Debt Does Yangzijiang Shipbuilding (Holdings) Carry?

You can click the graphic below for the historical numbers, but it shows that as of June 2019 Yangzijiang Shipbuilding (Holdings) had CN¥5.23b of debt, an increase on CN¥3.77b, over one year. However, its balance sheet shows it holds CN¥19.4b in cash, so it actually has CN¥14.2b net cash.

How Strong Is Yangzijiang Shipbuilding (Holdings)'s Balance Sheet?

The latest balance sheet data shows that Yangzijiang Shipbuilding (Holdings) had liabilities of CN¥9.70b due within a year, and liabilities of CN¥4.87b falling due after that. On the other hand, it had cash of CN¥19.4b and CN¥8.55b worth of receivables due within a year. So it can boast CN¥13.4b more liquid assets than total liabilities.

This surplus liquidity suggests that Yangzijiang Shipbuilding (Holdings)'s balance sheet could take a hit just as well as Homer Simpson's head can take a punch. With this in mind one could posit that its balance sheet is as strong as beautiful a rare rhino. Succinctly put, Yangzijiang Shipbuilding (Holdings) boasts net cash, so it's fair to say it does not have a heavy debt load!

But the other side of the story is that Yangzijiang Shipbuilding (Holdings) saw its EBIT decline by 4.3% over the last year. If earnings continue to decline at that rate the company may have increasing difficulty managing its debt load. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Yangzijiang Shipbuilding (Holdings) can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Yangzijiang Shipbuilding (Holdings) has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Yangzijiang Shipbuilding (Holdings) created free cash flow amounting to 8.1% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Summing up

While it is always sensible to investigate a company's debt, in this case Yangzijiang Shipbuilding (Holdings) has CN¥14.2b in net cash and a decent-looking balance sheet. So we don't think Yangzijiang Shipbuilding (Holdings)'s use of debt is risky. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Yangzijiang Shipbuilding (Holdings) insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SGX:BS6

Yangzijiang Shipbuilding (Holdings)

An investment holding company, engages in the shipbuilding activities in the Greater China, Canada, Japan, Italy, Greece, Germany, Bulgaria, United Kingdom, Singapore, and internationally.

Undervalued with solid track record and pays a dividend.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)