Advertisement

Is Yangzijiang Shipbuilding (Holdings) Ltd.'s (SGX:BS6) Stock's Recent Performance A Reflection Of Its Financial Health?

Most readers would already know that Yangzijiang Shipbuilding (Holdings)'s (SGX:BS6) stock increased by 8.1% over the past three months. Since the market usually pay for a company’s long-term financial health, we decided to study the company’s fundamentals to see if they could be influencing the market. In this article, we decided to focus on Yangzijiang Shipbuilding (Holdings)'s ROE.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

Check out our latest analysis for Yangzijiang Shipbuilding (Holdings)

How To Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Yangzijiang Shipbuilding (Holdings) is:

24% = CN¥5.4b ÷ CN¥23b (Based on the trailing twelve months to June 2024).

The 'return' is the profit over the last twelve months. One way to conceptualize this is that for each SGD1 of shareholders' capital it has, the company made SGD0.24 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Yangzijiang Shipbuilding (Holdings)'s Earnings Growth And 24% ROE

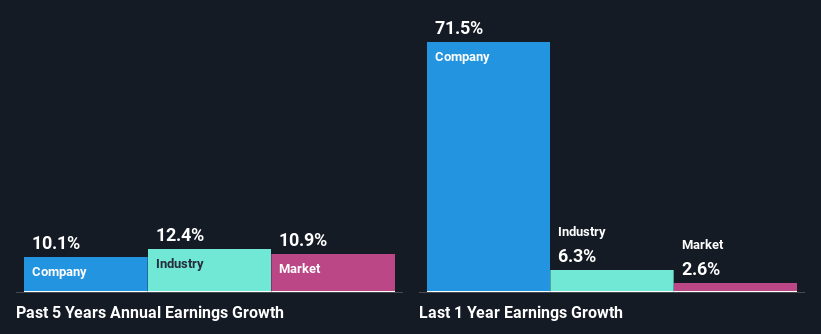

Firstly, we acknowledge that Yangzijiang Shipbuilding (Holdings) has a significantly high ROE. Second, a comparison with the average ROE reported by the industry of 7.6% also doesn't go unnoticed by us. Probably as a result of this, Yangzijiang Shipbuilding (Holdings) was able to see a decent net income growth of 10% over the last five years.

As a next step, we compared Yangzijiang Shipbuilding (Holdings)'s net income growth with the industry and found that the company has a similar growth figure when compared with the industry average growth rate of 12% in the same period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Yangzijiang Shipbuilding (Holdings) is trading on a high P/E or a low P/E, relative to its industry.

Is Yangzijiang Shipbuilding (Holdings) Making Efficient Use Of Its Profits?

With a three-year median payout ratio of 34% (implying that the company retains 66% of its profits), it seems that Yangzijiang Shipbuilding (Holdings) is reinvesting efficiently in a way that it sees respectable amount growth in its earnings and pays a dividend that's well covered.

Moreover, Yangzijiang Shipbuilding (Holdings) is determined to keep sharing its profits with shareholders which we infer from its long history of paying a dividend for at least ten years. Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 35% of its profits over the next three years. As a result, Yangzijiang Shipbuilding (Holdings)'s ROE is not expected to change by much either, which we inferred from the analyst estimate of 23% for future ROE.

Summary

On the whole, we feel that Yangzijiang Shipbuilding (Holdings)'s performance has been quite good. Specifically, we like that the company is reinvesting a huge chunk of its profits at a high rate of return. This of course has caused the company to see substantial growth in its earnings. Having said that, looking at the current analyst estimates, we found that the company's earnings are expected to gain momentum. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:BS6

Yangzijiang Shipbuilding (Holdings)

An investment holding company, engages in the shipbuilding activities in the Greater China, Canada, Japan, Italy, Greece, Germany, Bulgaria, United Kingdom, Singapore, and internationally.

Outstanding track record, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|20.1% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.5% undervalued

RO

Community Contributor