Oversea-Chinese Banking's (SGX:O39) Upcoming Dividend Will Be Larger Than Last Year's

Oversea-Chinese Banking Corporation Limited's (SGX:O39) dividend will be increasing to S$0.28 on 20th of May. This makes the dividend yield about the same as the industry average at 4.5%.

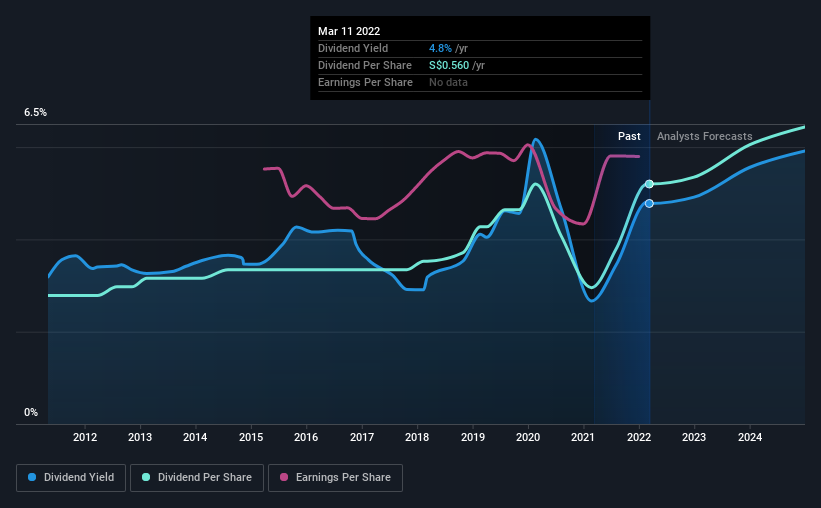

See our latest analysis for Oversea-Chinese Banking

Oversea-Chinese Banking's Payment Has Solid Earnings Coverage

We like a dividend to be consistent over the long term, so checking whether it is sustainable is important. Before making this announcement, Oversea-Chinese Banking was earning enough to cover the dividend, but it wasn't generating any free cash flows. In general, we consider cash flow to be more important than earnings, so we would be cautious about relying on the sustainability of this dividend.

Over the next year, EPS is forecast to expand by 12.4%. If the dividend continues along recent trends, we estimate the payout ratio will be 46%, which is in the range that makes us comfortable with the sustainability of the dividend.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2012, the first annual payment was S$0.30, compared to the most recent full-year payment of S$0.56. This means that it has been growing its distributions at 6.4% per annum over that time. It's good to see the dividend growing at a decent rate, but the dividend has been cut at least once in the past. Oversea-Chinese Banking might have put its house in order since then, but we remain cautious.

The Dividend Has Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. It's encouraging to see Oversea-Chinese Banking has been growing its earnings per share at 5.6% a year over the past five years. The company is paying out a lot of its cash as a dividend, but it looks okay based on the payout ratio.

In Summary

Overall, we always like to see the dividend being raised, but we don't think Oversea-Chinese Banking will make a great income stock. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. This company is not in the top tier of income providing stocks.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. To that end, Oversea-Chinese Banking has 2 warning signs (and 1 which is concerning) we think you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:O39

Oversea-Chinese Banking

Provides financial services in Singapore, Malaysia, Indonesia, Greater China, rest of the Asia Pacific, and internationally.

Flawless balance sheet, good value and pays a dividend.