Advertisement

- Sweden

- /

- Communications

- /

- OM:ERIC B

Uncovering Telefonaktiebolaget LM Ericsson And 2 Stocks That May Be Valued Below Their Estimated Worth

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a period of uncertainty marked by inflation fears and political shifts, investors are increasingly focused on identifying opportunities amid volatility. In such an environment, undervalued stocks can offer potential value, as they may be priced below their estimated worth due to market fluctuations or overlooked fundamentals.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Türkiye Sise Ve Cam Fabrikalari (IBSE:SISE) | TRY39.18 | TRY78.31 | 50% |

| Sudarshan Chemical Industries (BSE:506655) | ₹1115.85 | ₹2228.29 | 49.9% |

| Aguas Andinas (SNSE:AGUAS-A) | CLP290.00 | CLP578.96 | 49.9% |

| MLG Oz (ASX:MLG) | A$0.57 | A$1.14 | 50% |

| LifeMD (NasdaqGM:LFMD) | US$4.90 | US$9.77 | 49.8% |

| Dino Polska (WSE:DNP) | PLN433.60 | PLN863.86 | 49.8% |

| Cicor Technologies (SWX:CICN) | CHF59.60 | CHF118.58 | 49.7% |

| Greenworks (Jiangsu) (SZSE:301260) | CN¥13.95 | CN¥27.87 | 49.9% |

| Shinko Electric Industries (TSE:6967) | ¥5869.00 | ¥11708.96 | 49.9% |

| Prodways Group (ENXTPA:PWG) | €0.608 | €1.21 | 49.9% |

Let's take a closer look at a couple of our picks from the screened companies.

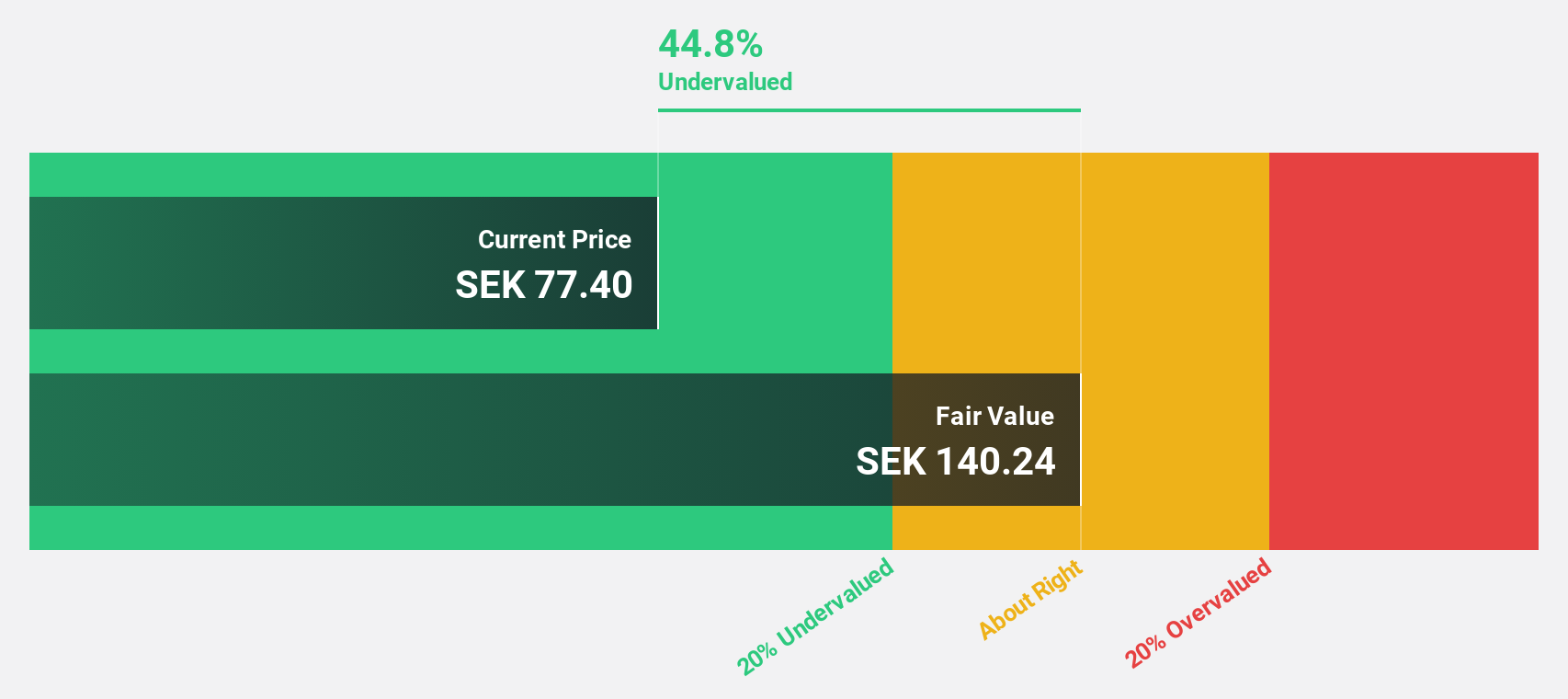

Telefonaktiebolaget LM Ericsson (OM:ERIC B)

Overview: Telefonaktiebolaget LM Ericsson (publ) offers mobile connectivity solutions for telecom operators and enterprise customers across multiple regions globally, with a market cap of approximately SEK316.67 billion.

Operations: The company's revenue segments include Networks at SEK156.41 billion, Enterprise at SEK25.47 billion, and Cloud Software and Services at SEK62.74 billion.

Estimated Discount To Fair Value: 41.5%

Telefonaktiebolaget LM Ericsson is trading at SEK95.02, significantly below its estimated fair value of SEK162.54, indicating it may be undervalued based on cash flows. The company is expected to achieve profitability within three years with a high annual earnings growth forecast of 73.16%. Recent strategic alliances and product innovations in 5G technology enhance its market position, although the dividend coverage remains weak. The appointment of Anthony Bartolo as CEO for a new venture could drive further growth initiatives.

- Our expertly prepared growth report on Telefonaktiebolaget LM Ericsson implies its future financial outlook may be stronger than recent results.

- Take a closer look at Telefonaktiebolaget LM Ericsson's balance sheet health here in our report.

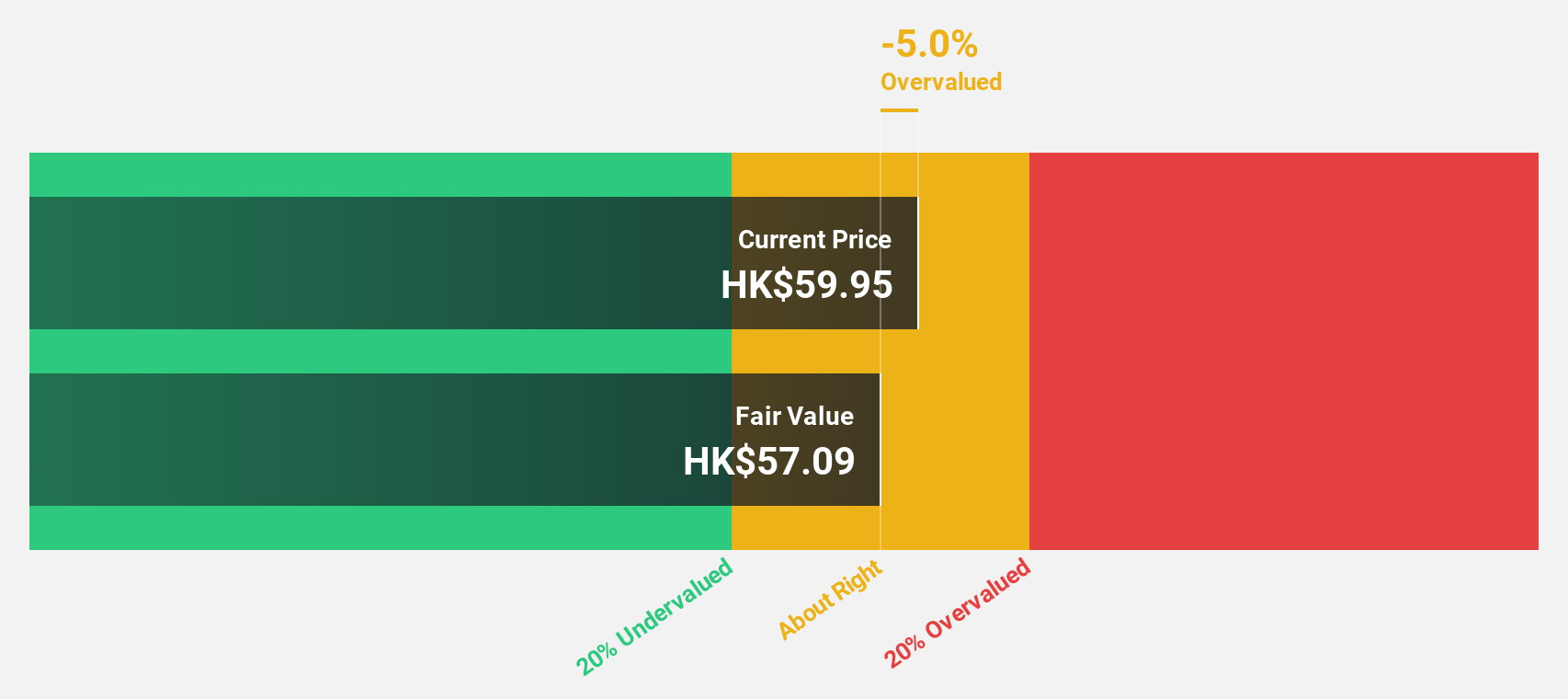

Xiaomi (SEHK:1810)

Overview: Xiaomi Corporation is an investment holding company that offers hardware and software services both in Mainland China and internationally, with a market cap of HK$841.66 billion.

Operations: The company's revenue is primarily derived from its Smartphones segment at CN¥184.68 billion, followed by IoT and Lifestyle Products at CN¥93.58 billion, and Internet Services generating CN¥32.66 billion.

Estimated Discount To Fair Value: 23.4%

Xiaomi is trading at HK$33.6, significantly below its estimated fair value of HK$43.86, suggesting it is undervalued based on cash flows. The company reported robust earnings growth with net income rising to CNY 5.35 billion in Q3 2024 from CNY 4.87 billion a year earlier, and its earnings are expected to grow significantly over the next three years at a rate faster than the Hong Kong market average.

- Insights from our recent growth report point to a promising forecast for Xiaomi's business outlook.

- Get an in-depth perspective on Xiaomi's balance sheet by reading our health report here.

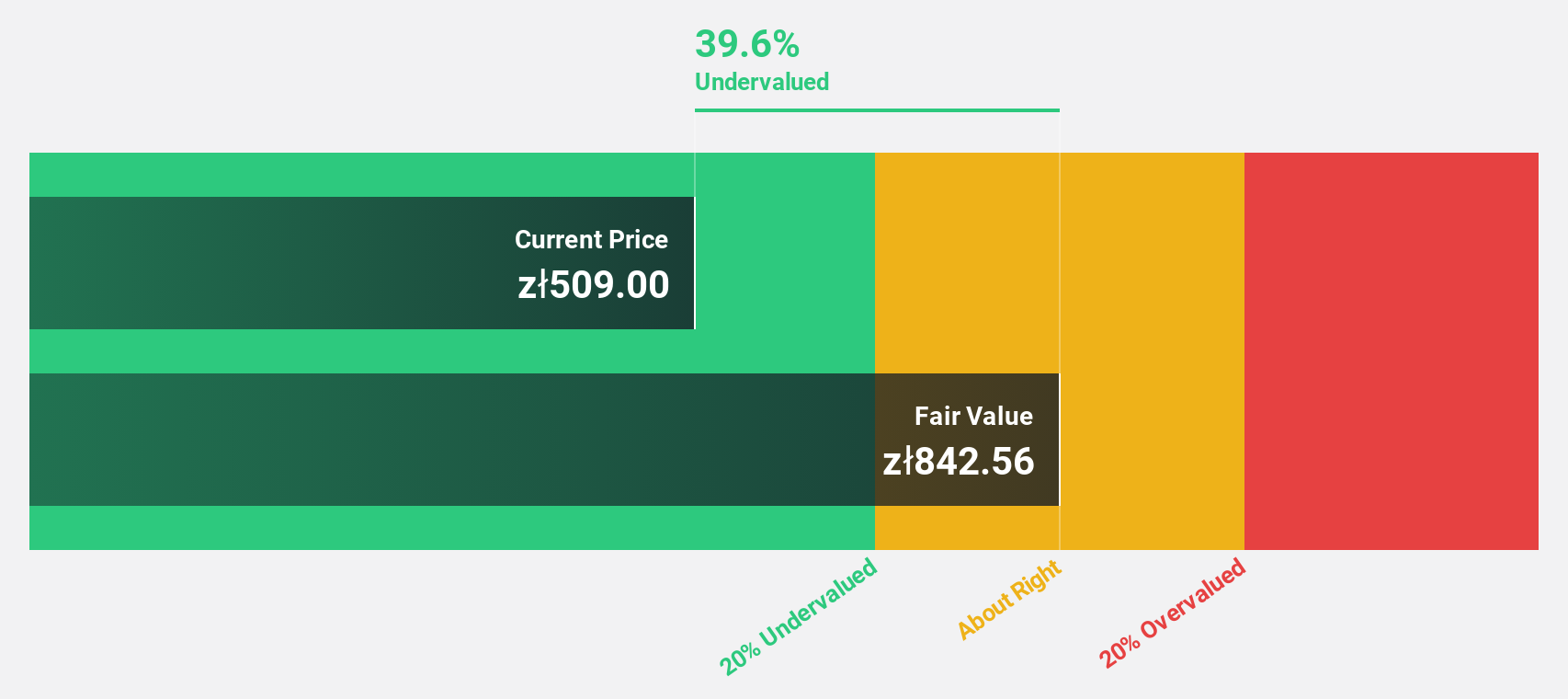

Dino Polska (WSE:DNP)

Overview: Dino Polska S.A. operates a network of mid-sized grocery supermarkets under the Dino brand in Poland, with a market cap of PLN42.51 billion.

Operations: The company's revenue segments include its network of mid-sized grocery supermarkets in Poland.

Estimated Discount To Fair Value: 49.8%

Dino Polska is trading at PLN 433.6, substantially below its estimated fair value of PLN 863.86, highlighting its undervaluation based on cash flows. Recent earnings show solid growth with Q3 net income of PLN 438.21 million, up from PLN 424.04 million year-on-year. The company's earnings and revenue are forecast to grow faster than the Polish market averages, contributing to its appeal as an undervalued investment opportunity in the region.

- In light of our recent growth report, it seems possible that Dino Polska's financial performance will exceed current levels.

- Unlock comprehensive insights into our analysis of Dino Polska stock in this financial health report.

Key Takeaways

- Click here to access our complete index of 880 Undervalued Stocks Based On Cash Flows.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Telefonaktiebolaget LM Ericsson might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:ERIC B

Telefonaktiebolaget LM Ericsson

Provides mobile connectivity solutions to communications service providers, enterprises, and the public sector.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor