I-Tech (OM:ITECH) Delivers 68% Earnings Growth, Reinforcing Profitability Narrative Despite Valuation Concerns

Reviewed by Simply Wall St

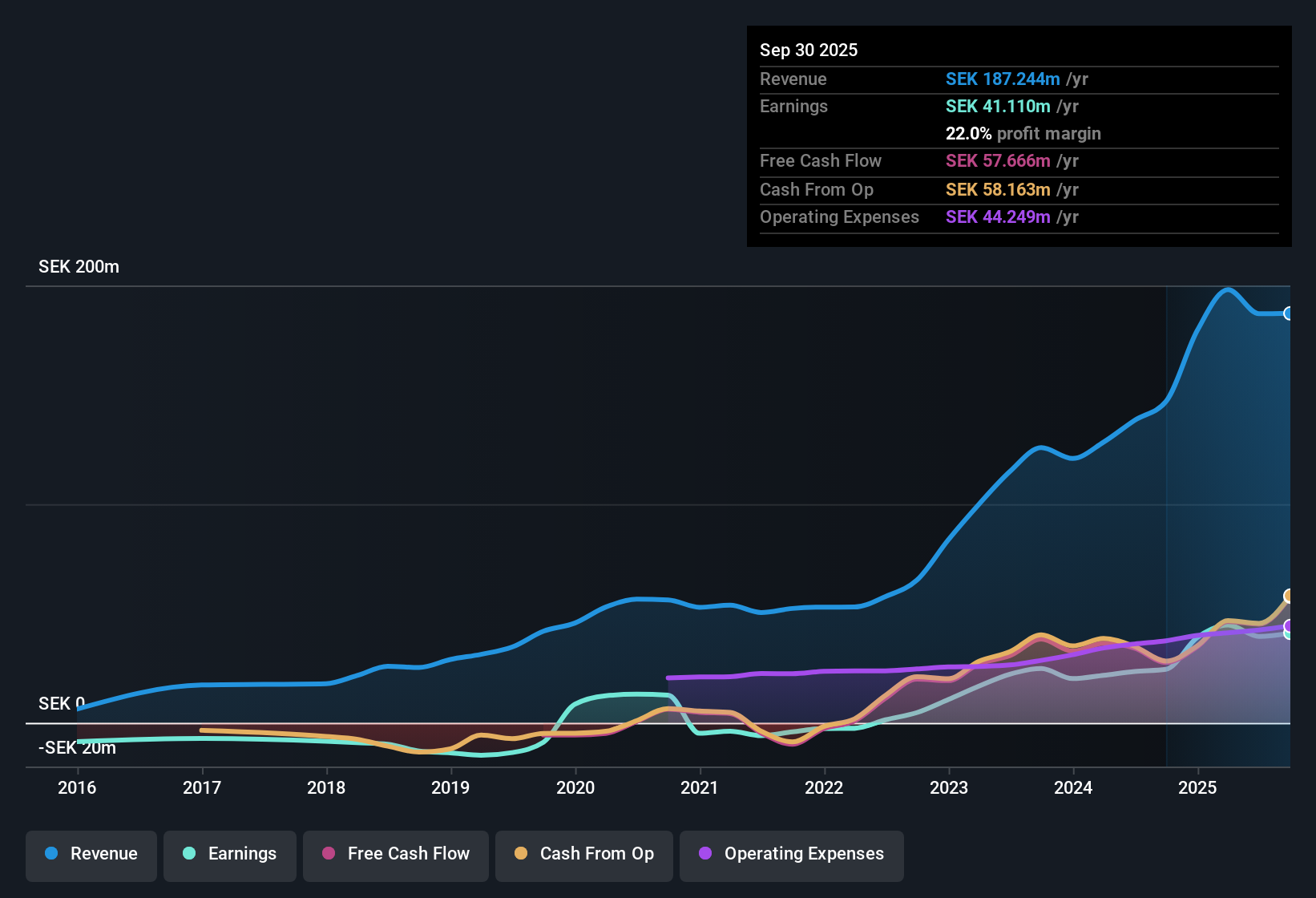

I-Tech (OM:ITECH) posted standout numbers this period, delivering annual earnings growth of 68.4% and pushing net profit margins up to 21.1% from last year’s 17%. With earnings forecast to grow 24.99% and revenue expected to climb 16.4% annually, both outpacing the Swedish market, investors saw a stock trading at SEK84, well below its estimated fair value of SEK310.67. While the company’s strong growth and robust margins are drawing positive attention, some are weighing these results against a relatively high P/E ratio of 25.5x and minor recent risks identified around dividends and short-term share price moves.

See our full analysis for I-Tech.Now let’s test these headline results against the bigger narrative. We’ll see where the latest earnings reinforce community expectations and where they push the story in a new direction.

See what the community is saying about I-Tech

Margins Powered by Operational Efficiencies

- Net profit margins reached 21.1%, a sizable increase from last year’s 17%, reflecting improved operational efficiencies and cost management that are specifically called out in management comments.

- Analysts' consensus view: the consensus narrative highlights that rising recurring revenue from a broadening customer base and process improvements are expected to support stronger operating margins moving forward.

- Higher margin visibility is supported by expectations of improved gross margins from supply chain optimization and strengthening recurring revenue streams.

- Consensus also expects product innovation and efficiency initiatives to further drive margin improvement over the next several years.

Risks Cluster Around Regulation and Revenue Mix

- Dependency on the eco-friendly Selektope product and a customer concentration of 99% revenue share in Asia expose I-Tech to significant regulatory and regional risks, especially if EU reregistration or market access is delayed or denied.

- Analysts' consensus view: bears argue that ongoing regulatory uncertainty and regional concentration pose genuine threats to revenue stability and future earnings growth.

- Consensus specifically flags that a delay or negative outcome in Selektope’s reregistration process could restrict key market access and slow overall revenue momentum.

- Currency volatility and shifting sales dynamics in Asia, including a drop in China with offsetting increases in Korea, add to earnings unpredictability according to the consensus narrative.

DCF Fair Value Sits Triple Current Price

- Despite the stock trading at SEK84.0, well beneath both the analyst price target of SEK86.0 and the DCF fair value of SEK310.67, I-Tech’s Price-to-Earnings ratio of 25.5x stands far above its peer group at 13.7x and the European Chemicals industry average of 16.8x.

- Analysts' consensus view: the consensus narrative balances this valuation gap by noting that while growth outlook is strong, the market is already pricing in much of it, leaving only a 0.2% upside to the analyst target and challenging the idea of a deep bargain.

- Analysts estimate that, to justify the current stock price and meet the price target, I-Tech would need to achieve SEK303.3 million in revenues and SEK97.4 million in earnings by 2028, reducing its PE to 12.4x, below the present sector average.

- The modest difference between current share price and analyst target suggests market participants largely agree on a fair price, despite the big headline DCF fair value number.

Consensus is increasingly focused on whether I-Tech's impressive profit growth and fair value gap can outweigh margin risks and a demanding valuation. See the full Consensus Narrative for a detailed breakdown of both sides. 📊 Read the full I-Tech Consensus Narrative.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for I-Tech on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have a distinct take on the latest results? Shape your insight and create your own narrative in just a few minutes. Do it your way

A great starting point for your I-Tech research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Despite rapid profit growth, I-Tech’s valuation looks stretched. Any disappointment in regulation or margins could leave investors facing limited near-term upside.

If you want to avoid valuation traps and find opportunities trading well below fair value, check out these 878 undervalued stocks based on cash flows for stocks with more attractive price-to-value gaps right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:ITECH

I-Tech

A biotechnology company, develops, markets, and sells antifouling coating products in Sweden.

Outstanding track record with flawless balance sheet.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Salesforce Stock: AI-Fueled Growth Is Real — But Can Margins Stay This Strong?

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)