- Sweden

- /

- Capital Markets

- /

- OM:RATO B

Ratos AB (publ) Just Recorded A 10% EPS Beat: Here's What Analysts Are Forecasting Next

There's been a notable change in appetite for Ratos AB (publ) (STO:RATO B) shares in the week since its full-year report, with the stock down 10% to kr43.90. Revenues disappointed slightly, as sales of kr23b were 4.0% below what the analyst had predicted. Profits were a relative bright spot, with statutory per-share earnings of kr2.83 coming in 10% above what was anticipated. Following the result, the analyst has updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analyst has changed their mind on Ratos after the latest results.

Check out our latest analysis for Ratos

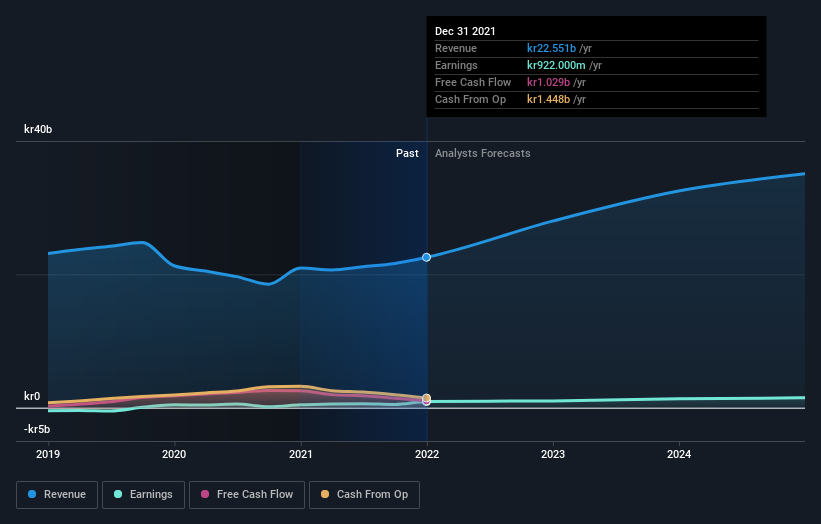

Taking into account the latest results, the most recent consensus for Ratos from lone analyst is for revenues of kr28.0b in 2022 which, if met, would be a substantial 24% increase on its sales over the past 12 months. Per-share earnings are expected to rise 9.5% to kr3.11. Before this earnings report, the analyst had been forecasting revenues of kr24.9b and earnings per share (EPS) of kr4.08 in 2022. Although revenues are expected to increase meaningfully, the analyst has acknowledged the cost of growth, given the large cut to EPS estimates following the latest report.

The consensus price target was unchanged at kr57.00, suggesting the business is performing roughly in line with expectations, despite some adjustments to profit and revenue forecasts.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. One thing stands out from these estimates, which is that Ratos is forecast to grow faster in the future than it has in the past, with revenues expected to display 24% annualised growth until the end of 2022. If achieved, this would be a much better result than the 3.9% annual decline over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue grow 13% per year. Not only are Ratos' revenues expected to improve, it seems that the analyst is also expecting it to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analyst reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Ratos. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. The consensus price target held steady at kr57.00, with the latest estimates not enough to have an impact on their price target.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Ratos going out as far as 2024, and you can see them free on our platform here.

Before you take the next step you should know about the 2 warning signs for Ratos that we have uncovered.

If you're looking to trade Ratos, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:RATO B

Ratos

A private equity firm specializing in buyouts, turnarounds, add on acquisitions, and middle market transactions.

Reasonable growth potential with mediocre balance sheet.