Advertisement

- Sweden

- /

- Consumer Finance

- /

- OM:HOFI

3 European Stocks Estimated To Be Trading At Discounts Of Up To 22.1%

Simply Wall St

Reviewed by Simply Wall St

As trade tensions show signs of easing, European markets have experienced a notable upswing, with the pan-European STOXX Europe 600 Index climbing 2.77% and major indices like Germany's DAX and France's CAC 40 posting significant gains. In this environment, identifying undervalued stocks can be particularly rewarding for investors seeking opportunities in companies that may be trading below their intrinsic value due to temporary market conditions or broader economic uncertainties.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Micro Systemation (OM:MSAB B) | SEK48.56 | SEK96.48 | 49.7% |

| Andritz (WBAG:ANDR) | €57.15 | €112.74 | 49.3% |

| Qt Group Oyj (HLSE:QTCOM) | €56.30 | €109.63 | 48.6% |

| LPP (WSE:LPP) | PLN15600.00 | PLN30445.48 | 48.8% |

| Pluxee (ENXTPA:PLX) | €18.80 | €36.93 | 49.1% |

| Stille (OM:STIL) | SEK190.00 | SEK369.93 | 48.6% |

| TF Bank (OM:TFBANK) | SEK351.50 | SEK682.26 | 48.5% |

| ATON Green Storage (BIT:ATON) | €1.93 | €3.83 | 49.6% |

| Expert.ai (BIT:EXAI) | €1.31 | €2.58 | 49.3% |

| Longino & Cardenal (BIT:LON) | €1.35 | €2.67 | 49.4% |

Here we highlight a subset of our preferred stocks from the screener.

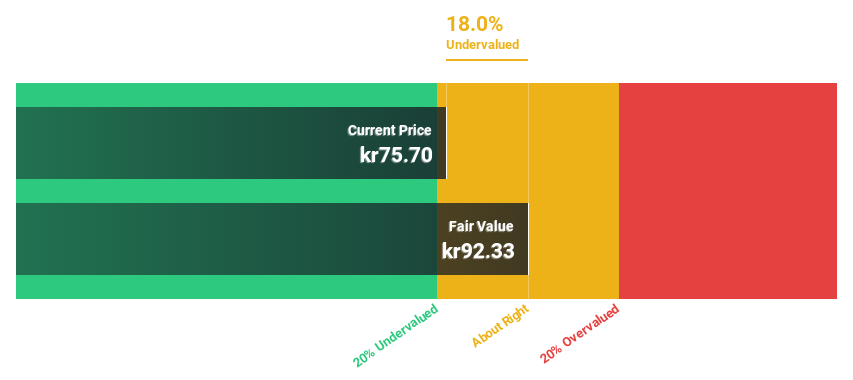

Fiskars Oyj Abp (HLSE:FSKRS)

Overview: Fiskars Oyj Abp manufactures and markets consumer products for indoor and outdoor living across Europe, the Americas, and the Asia Pacific, with a market cap of €1.20 billion.

Operations: The company's revenue segments include €606.30 million from Vita and €554.70 million from Fiskars.

Estimated Discount To Fair Value: 20.7%

Fiskars Oyj Abp, trading at €14.8, is considered undervalued with a fair value estimate of €18.65 based on discounted cash flow analysis. Despite recent challenges, including a Q1 net loss of €13.2 million and interest payments not well covered by earnings, the company's earnings are forecast to grow significantly at 41.6% annually over the next three years, outpacing the Finnish market's growth rate of 12.6%.

- The analysis detailed in our Fiskars Oyj Abp growth report hints at robust future financial performance.

- Click here and access our complete balance sheet health report to understand the dynamics of Fiskars Oyj Abp.

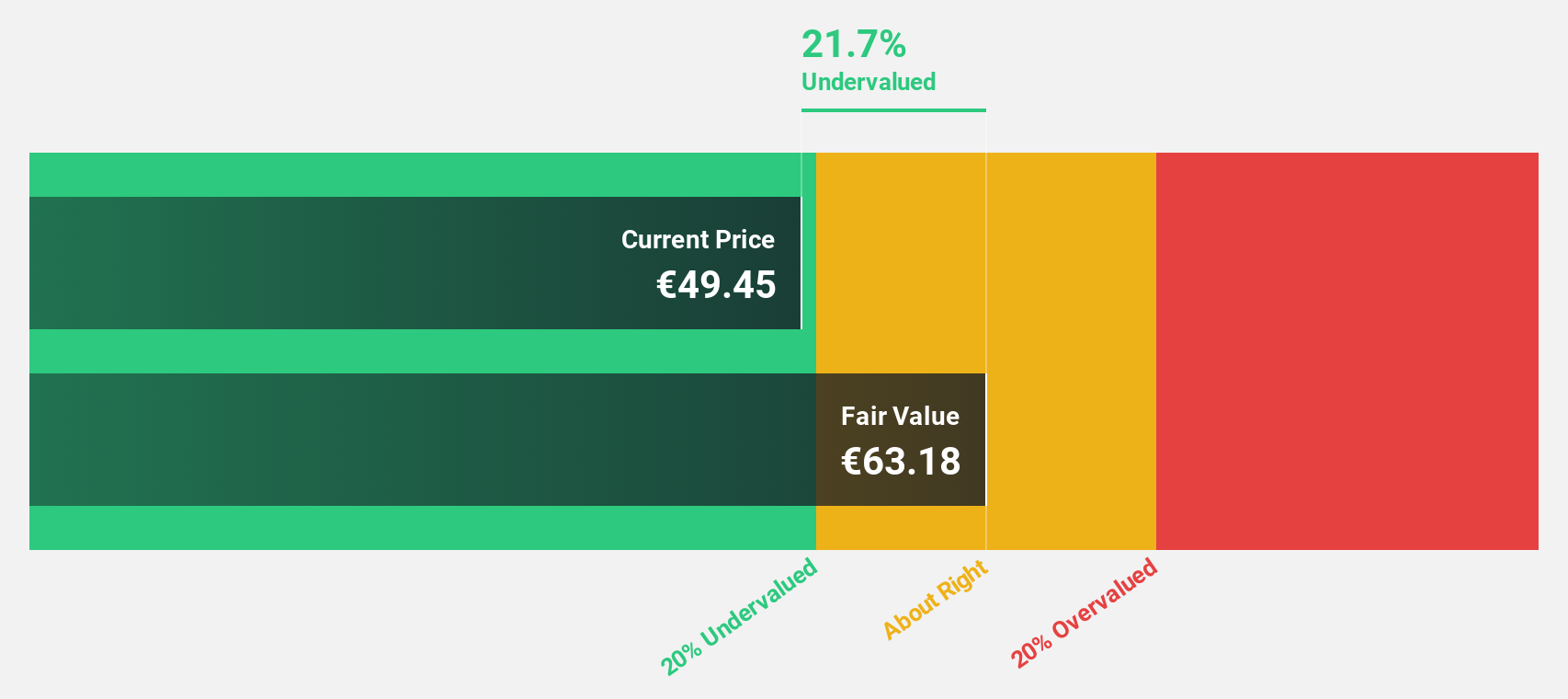

Harvia Oyj (HLSE:HARVIA)

Overview: Harvia Oyj is a company that operates in the sauna industry, with a market cap of €748.49 million.

Operations: The company's revenue is primarily generated from its Building Materials - HVAC Equipment segment, amounting to €175.21 million.

Estimated Discount To Fair Value: 22.1%

Harvia Oyj, trading at €40.05, is undervalued with a fair value estimate of €51.44 based on discounted cash flow analysis. Despite slower revenue growth at 9.5% annually compared to the Finnish market's 3.5%, its earnings are projected to grow faster than the market at 16.1% per year. Recent board changes and dividend increases reflect strategic adjustments as Harvia expands internationally and diversifies its product offerings amidst evolving business needs.

- Our earnings growth report unveils the potential for significant increases in Harvia Oyj's future results.

- Delve into the full analysis health report here for a deeper understanding of Harvia Oyj.

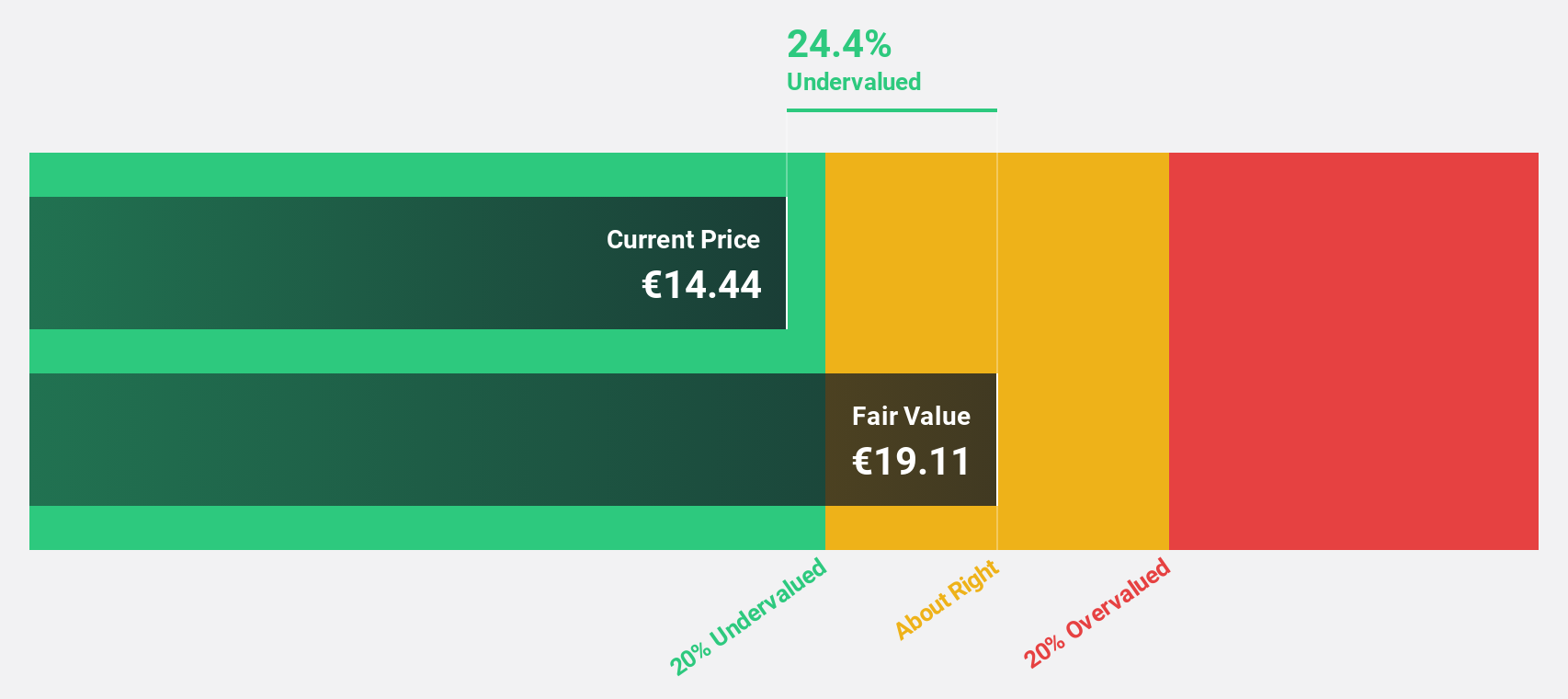

Hoist Finance (OM:HOFI)

Overview: Hoist Finance AB (publ) is a credit market company that specializes in loan acquisition and management operations across Europe, with a market capitalization of SEK7.44 billion.

Operations: Hoist Finance generates revenue from its operations in Europe through segments including Secured loans at SEK1.06 billion and Unsecured loans at SEK3.02 billion, with additional contributions from Group Items amounting to SEK97 million.

Estimated Discount To Fair Value: 15.1%

Hoist Finance, trading at SEK 85.05, is undervalued with a fair value estimate of SEK 100.22 based on discounted cash flow analysis. Despite carrying high debt levels, its earnings grew by 72% last year and are forecast to rise annually by 19.2%, outpacing the Swedish market's growth rate. Recent share buybacks and fixed-income offerings totaling SEK 1.25 billion indicate strategic financial maneuvers amidst executive changes and dividend affirmations of SEK 2 per share for May 2025.

- Our expertly prepared growth report on Hoist Finance implies its future financial outlook may be stronger than recent results.

- Click to explore a detailed breakdown of our findings in Hoist Finance's balance sheet health report.

Key Takeaways

- Click here to access our complete index of 180 Undervalued European Stocks Based On Cash Flows.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hoist Finance might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:HOFI

Hoist Finance

A credit market company, engages in the loan acquisition and management operations in Europe.

Good value average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor