Advertisement

- Sweden

- /

- Hospitality

- /

- OM:EVO

Lacklustre Performance Is Driving Evolution AB (publ)'s (STO:EVO) Low P/E

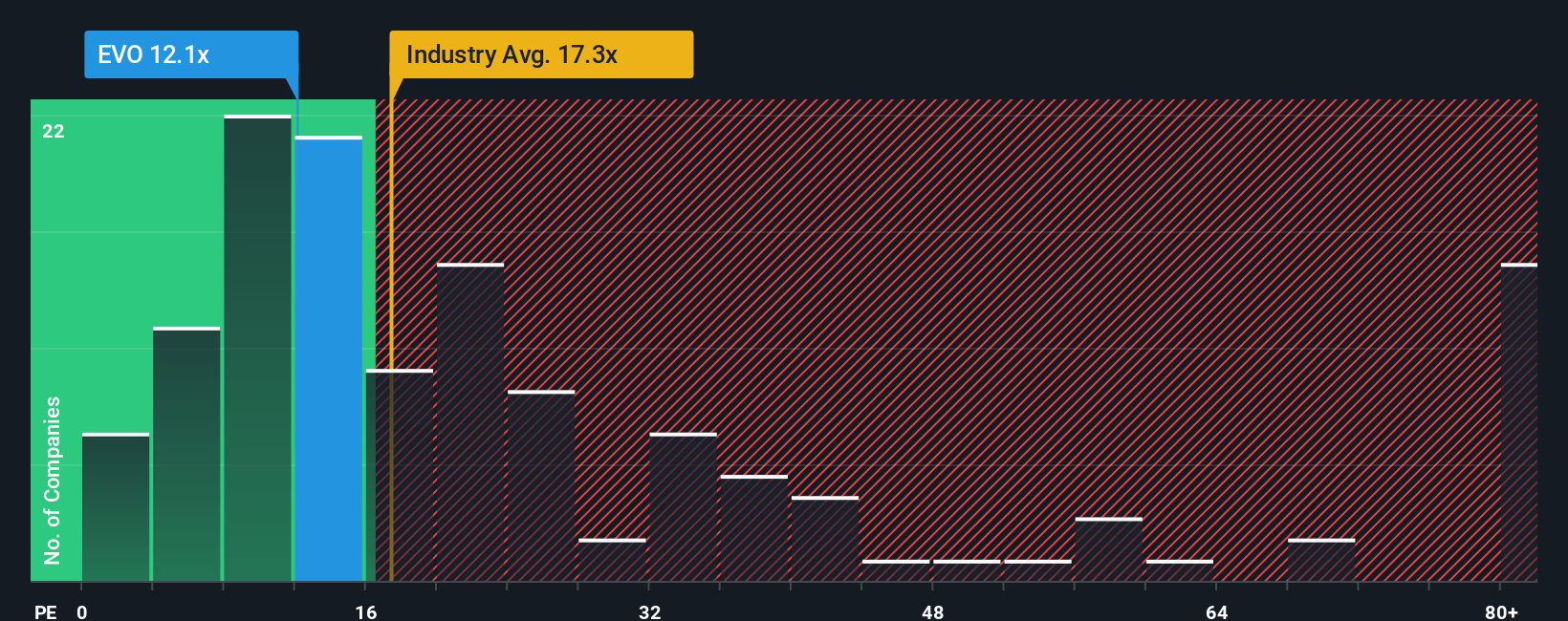

Evolution AB (publ)'s (STO:EVO) price-to-earnings (or "P/E") ratio of 12.1x might make it look like a buy right now compared to the market in Sweden, where around half of the companies have P/E ratios above 23x and even P/E's above 38x are quite common. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Evolution certainly has been doing a good job lately as it's been growing earnings more than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for Evolution

What Are Growth Metrics Telling Us About The Low P/E?

In order to justify its P/E ratio, Evolution would need to produce sluggish growth that's trailing the market.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 14% last year. Pleasingly, EPS has also lifted 77% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 3.8% each year over the next three years. Meanwhile, the rest of the market is forecast to expand by 18% per annum, which is noticeably more attractive.

With this information, we can see why Evolution is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Evolution maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

The company's balance sheet is another key area for risk analysis. Take a look at our free balance sheet analysis for Evolution with six simple checks on some of these key factors.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're here to simplify it.

Discover if Evolution might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:EVO

Evolution

Develops, produces, markets, and licenses live casino and slots solutions to gaming operators in Europe, Asia, North America, Latin America, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7061.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17036.6% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38026.3% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.8% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

Recently Updated Narratives

IM

Imthetxarbi on Maha Capital ·

Is It worth SEK 16? Arbitrage opportunity?

Fair Value:SEK 0.681.1k% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AR

ariz_scribe on Marti Technologies ·

$MRT at Roth - Pick of the Panel

Fair Value:US$1.968.7% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CJ

cjimi on Wise Group ·

Wise: A Quality Cross-Border Payments Compounder, But Not A Bargain

Fair Value:UK£12.0232.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.7% undervalued

124 followersusers have followed this narrative

2 commentsusers have commented on this narrative

36 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9722.1% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1930.3% undervalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative