The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Rejlers AB (publ) (STO:REJL B) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Rejlers

How Much Debt Does Rejlers Carry?

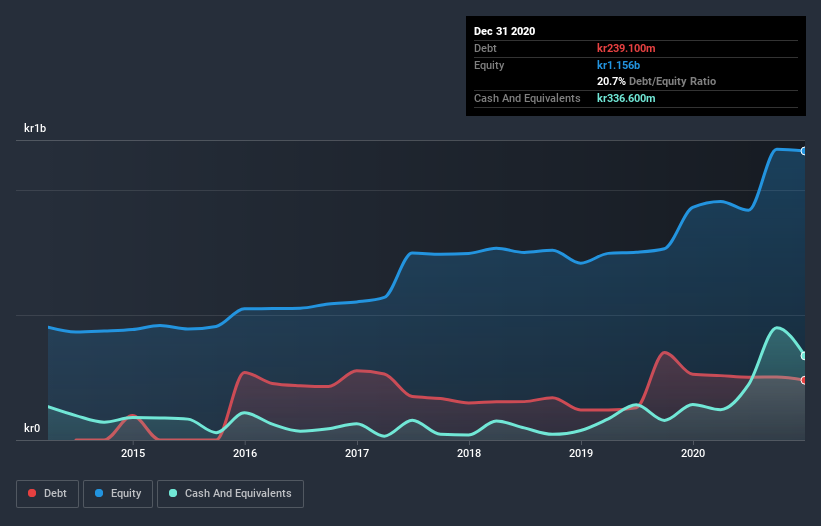

The image below, which you can click on for greater detail, shows that Rejlers had debt of kr239.1m at the end of December 2020, a reduction from kr262.8m over a year. However, its balance sheet shows it holds kr336.6m in cash, so it actually has kr97.5m net cash.

A Look At Rejlers' Liabilities

Zooming in on the latest balance sheet data, we can see that Rejlers had liabilities of kr658.2m due within 12 months and liabilities of kr424.5m due beyond that. Offsetting this, it had kr336.6m in cash and kr621.2m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by kr124.9m.

Of course, Rejlers has a market capitalization of kr3.12b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. While it does have liabilities worth noting, Rejlers also has more cash than debt, so we're pretty confident it can manage its debt safely.

The good news is that Rejlers has increased its EBIT by 5.0% over twelve months, which should ease any concerns about debt repayment. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Rejlers can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Rejlers may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Rejlers actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Rejlers has kr97.5m in net cash. The cherry on top was that in converted 225% of that EBIT to free cash flow, bringing in kr284m. So we don't think Rejlers's use of debt is risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 2 warning signs we've spotted with Rejlers .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

When trading Rejlers or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OM:REJL B

Rejlers

Engages in the provision of technical and engineering consultancy services in Sweden, Finland, Norway, and the United Arab Emirates.

Excellent balance sheet, good value and pays a dividend.