- Sweden

- /

- Professional Services

- /

- OM:REJL B

Here's Why Rejlers (STO:REJL B) Can Manage Its Debt Responsibly

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Rejlers AB (publ) (STO:REJL B) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Rejlers

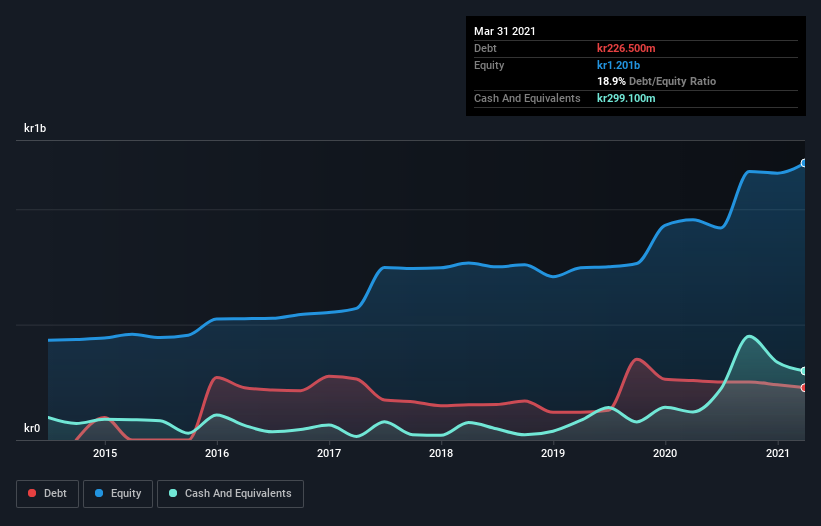

What Is Rejlers's Net Debt?

As you can see below, Rejlers had kr226.5m of debt at March 2021, down from kr257.5m a year prior. However, it does have kr299.1m in cash offsetting this, leading to net cash of kr72.6m.

A Look At Rejlers' Liabilities

Zooming in on the latest balance sheet data, we can see that Rejlers had liabilities of kr702.3m due within 12 months and liabilities of kr426.6m due beyond that. On the other hand, it had cash of kr299.1m and kr663.1m worth of receivables due within a year. So its liabilities total kr166.7m more than the combination of its cash and short-term receivables.

Of course, Rejlers has a market capitalization of kr2.96b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Rejlers also has more cash than debt, so we're pretty confident it can manage its debt safely.

In fact Rejlers's saving grace is its low debt levels, because its EBIT has tanked 25% in the last twelve months. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Rejlers can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Rejlers may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, Rejlers actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Rejlers has kr72.6m in net cash. And it impressed us with free cash flow of kr297m, being 263% of its EBIT. So we don't have any problem with Rejlers's use of debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 1 warning sign for Rejlers you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

When trading Rejlers or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OM:REJL B

Rejlers

Engages in the provision of technical and engineering consultancy services in Sweden, Finland, Norway, and the United Arab Emirates.

Excellent balance sheet, good value and pays a dividend.