Advertisement

Here's Why Munters Group AB (publ)'s (STO:MTRS) CEO May Deserve A Raise

Key Insights

- Munters Group to hold its Annual General Meeting on 21st of March

- CEO Klas Forsstrom's total compensation includes salary of kr8.14m

- The total compensation is 44% less than the average for the industry

- Over the past three years, Munters Group's EPS grew by 22% and over the past three years, the total shareholder return was 155%

The solid performance at Munters Group AB (publ) (STO:MTRS) has been impressive and shareholders will probably be pleased to know that CEO Klas Forsstrom has delivered. At the upcoming AGM on 21st of March, they will get a chance to hear the board review the company results, discuss future strategy and cast their vote on any resolutions such as executive remuneration. We think the CEO has done a pretty decent job and probably deserves a well-earned pay rise.

See our latest analysis for Munters Group

Comparing Munters Group AB (publ)'s CEO Compensation With The Industry

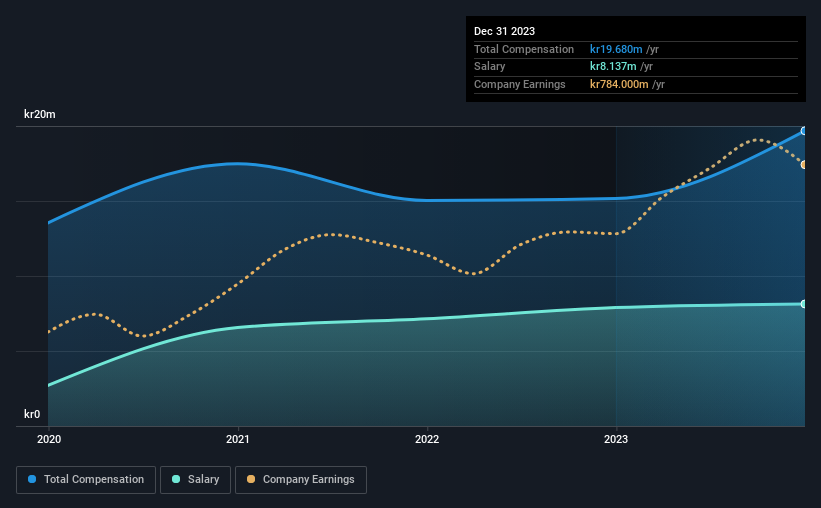

Our data indicates that Munters Group AB (publ) has a market capitalization of kr35b, and total annual CEO compensation was reported as kr20m for the year to December 2023. We note that's an increase of 30% above last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at kr8.1m.

In comparison with other companies in the Swedish Building industry with market capitalizations ranging from kr21b to kr66b, the reported median CEO total compensation was kr35m. Accordingly, Munters Group pays its CEO under the industry median. What's more, Klas Forsstrom holds kr15m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | kr8.1m | kr7.9m | 41% |

| Other | kr12m | kr7.3m | 59% |

| Total Compensation | kr20m | kr15m | 100% |

Speaking on an industry level, salary and non-salary portions, both make up 50% each of the total remuneration. It's interesting to note that Munters Group allocates a smaller portion of compensation to salary in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Munters Group AB (publ)'s Growth Numbers

Munters Group AB (publ)'s earnings per share (EPS) grew 22% per year over the last three years. Its revenue is up 34% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's great to see that revenue growth is strong, too. These metrics suggest the business is growing strongly. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Munters Group AB (publ) Been A Good Investment?

Most shareholders would probably be pleased with Munters Group AB (publ) for providing a total return of 155% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

Seeing that the company has put in a relatively good performance, the CEO remuneration policy may not be the focus at the AGM. In fact, strategic decisions that could impact the future of the business might be a far more interesting topic for investors as it would help them set their longer-term expectations.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We did our research and spotted 1 warning sign for Munters Group that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:MTRS

Munters Group

Provides climate solutions in the Americas, Europe, the Middle East, Africa, and Asia.

Undervalued with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|24.5% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|24.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.2% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|97.7% undervalued

RO

Community Contributor