Advertisement

- Sweden

- /

- Industrials

- /

- OM:LIFCO B

We Think Shareholders Will Probably Be Generous With Lifco AB (publ)'s (STO:LIFCO B) CEO Compensation

Key Insights

- Lifco to hold its Annual General Meeting on 25th of April

- Salary of kr31.6m is part of CEO Per Waldemarson's total remuneration

- The overall pay is comparable to the industry average

- Lifco's EPS grew by 11% over the past three years while total shareholder return over the past three years was 65%

It would be hard to discount the role that CEO Per Waldemarson has played in delivering the impressive results at Lifco AB (publ) (STO:LIFCO B) recently. Shareholders will have this at the front of their minds in the upcoming AGM on 25th of April. It is likely that the focus will be on company strategy going forward as shareholders hear from the board and cast their votes on resolutions such as executive remuneration and other matters. In light of the great performance, we discuss the case why we think CEO compensation is not excessive.

See our latest analysis for Lifco

How Does Total Compensation For Per Waldemarson Compare With Other Companies In The Industry?

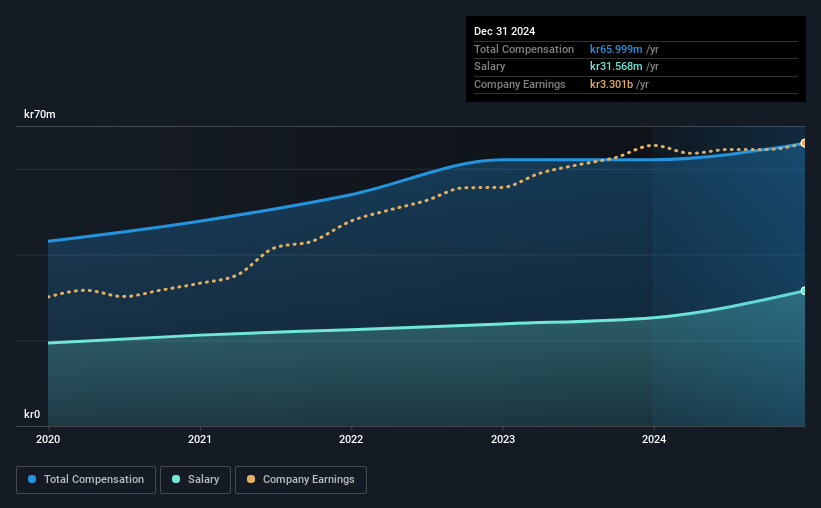

Our data indicates that Lifco AB (publ) has a market capitalization of kr158b, and total annual CEO compensation was reported as kr66m for the year to December 2024. That's a modest increase of 6.2% on the prior year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at kr32m.

On comparing similar companies in the Swedish Industrials industry with market capitalizations above kr77b, we found that the median total CEO compensation was kr66m. This suggests that Lifco remunerates its CEO largely in line with the industry average. Moreover, Per Waldemarson also holds kr304m worth of Lifco stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | kr32m | kr25m | 48% |

| Other | kr34m | kr37m | 52% |

| Total Compensation | kr66m | kr62m | 100% |

On an industry level, around 60% of total compensation represents salary and 40% is other remuneration. Lifco sets aside a smaller share of compensation for salary, in comparison to the overall industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Lifco AB (publ)'s Growth Numbers

Over the past three years, Lifco AB (publ) has seen its earnings per share (EPS) grow by 11% per year. Its revenue is up 6.9% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's good to see a bit of revenue growth, as this suggests the business is able to grow sustainably. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Lifco AB (publ) Been A Good Investment?

Boasting a total shareholder return of 65% over three years, Lifco AB (publ) has done well by shareholders. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

Given the company's decent performance, the CEO remuneration policy might not be shareholders' central point of focus in the AGM. In fact, strategic decisions that could impact the future of the business might be a far more interesting topic for investors as it would help them set their longer-term expectations.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 1 warning sign for Lifco that you should be aware of before investing.

Switching gears from Lifco, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:LIFCO B

Lifco

Engages in the dental, demolition and tools, and systems solutions businesses in Sweden, Norway, Germany, rest of Europe, the United Kingdom, Asia, Australia, Italy, North America, and internationally.

Acceptable track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor