Advertisement

- Saudi Arabia

- /

- Basic Materials

- /

- SASE:3060

Three Stocks That Might Be Trading Below Their Estimated Value

Simply Wall St

Reviewed by Simply Wall St

In a week marked by mixed performances across major global indices, growth stocks have outpaced their value counterparts significantly, highlighting the diverse sectoral movements within the market. As investors navigate these fluctuating conditions, identifying stocks that might be trading below their estimated value could present opportunities for those seeking to balance potential risks with rewards. Understanding what makes a stock potentially undervalued involves examining factors such as financial health, market position, and growth prospects relative to current price levels.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Shandong Bailong Chuangyuan Bio-Tech (SHSE:605016) | CN¥16.64 | CN¥33.16 | 49.8% |

| Hanwha Systems (KOSE:A272210) | ₩19960.00 | ₩39689.35 | 49.7% |

| Komax Holding (SWX:KOMN) | CHF120.20 | CHF240.31 | 50% |

| GREE (TSE:3632) | ¥458.00 | ¥912.32 | 49.8% |

| EnomotoLtd (TSE:6928) | ¥1445.00 | ¥2885.33 | 49.9% |

| Aguas Andinas (SNSE:AGUAS-A) | CLP289.00 | CLP576.88 | 49.9% |

| Privia Health Group (NasdaqGS:PRVA) | US$21.62 | US$43.17 | 49.9% |

| Pluxee (ENXTPA:PLX) | €20.555 | €40.82 | 49.6% |

| Visional (TSE:4194) | ¥8501.00 | ¥16991.03 | 50% |

| Cicor Technologies (SWX:CICN) | CHF58.40 | CHF116.64 | 49.9% |

Below we spotlight a couple of our favorites from our exclusive screener.

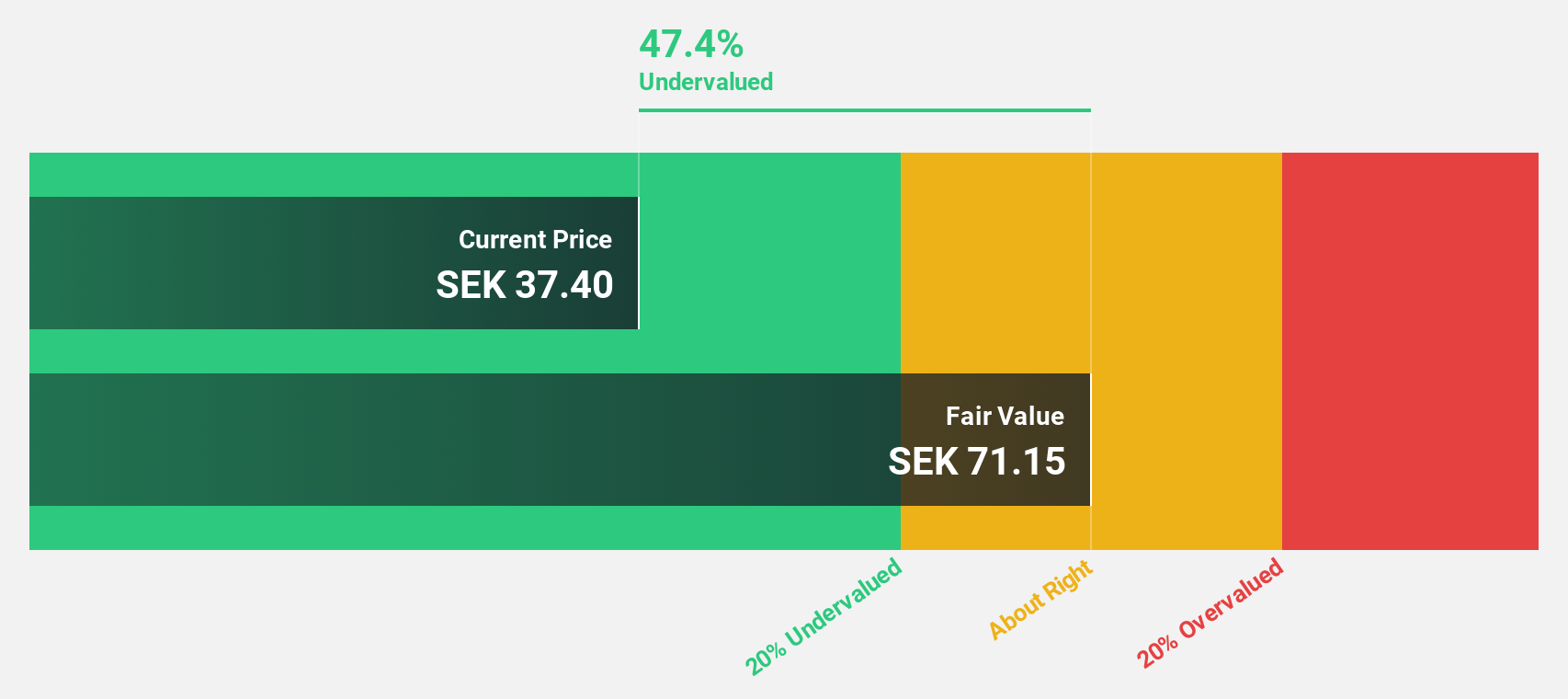

Fagerhult Group (OM:FAG)

Overview: Fagerhult Group AB, along with its subsidiaries, manufactures and sells professional lighting solutions globally and has a market cap of SEK10.26 billion.

Operations: The company's revenue segments include Premium at SEK2.87 billion, Collection at SEK3.91 billion, Professional at SEK1.03 billion, and Infrastructure at SEK843.90 million.

Estimated Discount To Fair Value: 40.3%

Fagerhult Group is trading at SEK58.2, significantly below its estimated fair value of SEK97.53, highlighting its potential undervaluation based on discounted cash flow analysis. Despite a challenging market and declining recent earnings—Q3 sales at SEK1.92 billion down from SEK2.08 billion last year—the company forecasts significant annual earnings growth of 24.4%, outpacing the Swedish market's 15.2%. However, revenue growth remains modest at 2.1% annually, with an unstable dividend history noted amidst ongoing strategic M&A initiatives.

- The analysis detailed in our Fagerhult Group growth report hints at robust future financial performance.

- Get an in-depth perspective on Fagerhult Group's balance sheet by reading our health report here.

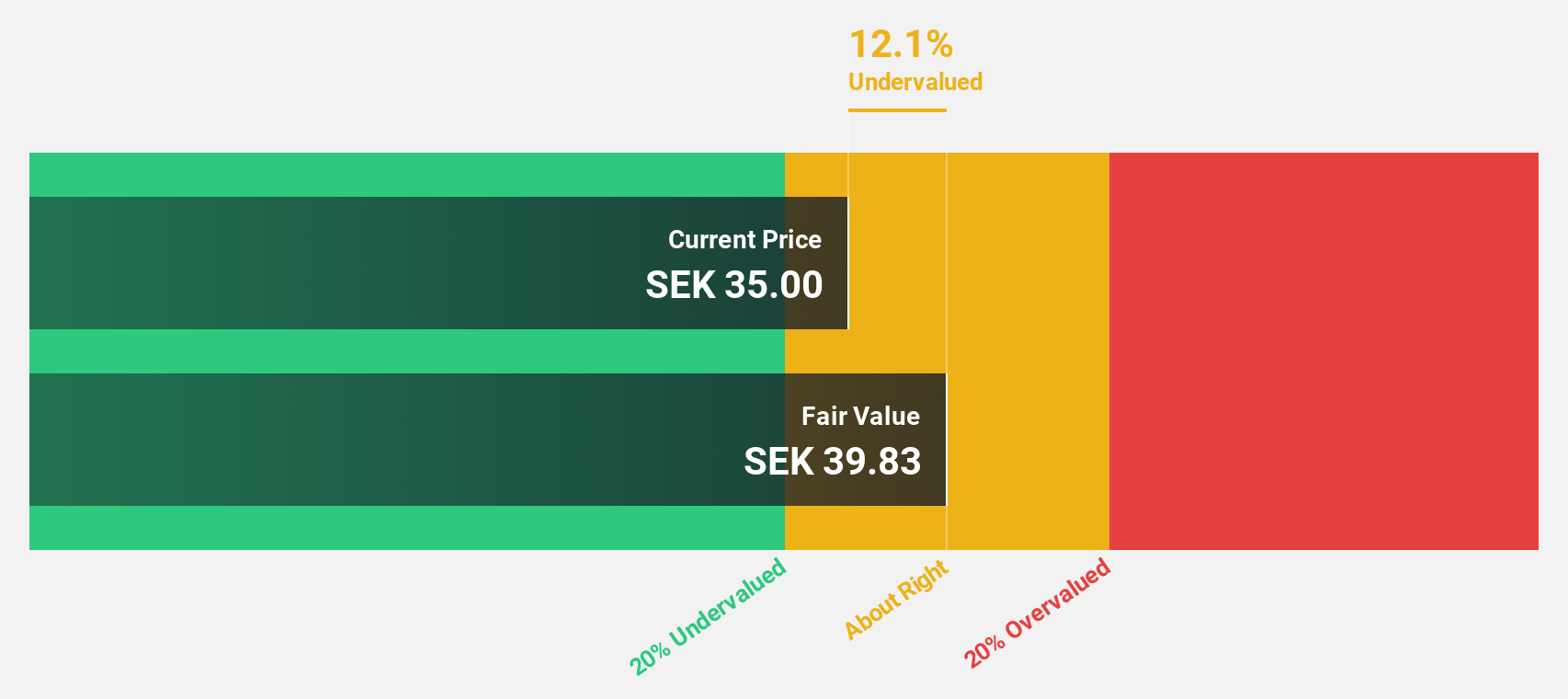

Ratos (OM:RATO B)

Overview: Ratos AB (publ) is a private equity firm that focuses on buyouts, turnarounds, add-on acquisitions, and middle market transactions with a market cap of approximately SEK11.01 billion.

Operations: The company's revenue is divided into three main segments: Consumer at SEK5.46 billion, Industry at SEK10.41 billion, and Construction & Services at SEK16.49 billion.

Estimated Discount To Fair Value: 27.5%

Ratos is trading at SEK33.3, 27.5% below its estimated fair value of SEK45.91, suggesting significant undervaluation based on discounted cash flow analysis. Despite recent financial challenges—Q3 sales dropped to SEK7.45 billion from SEK7.97 billion and a net loss of SEK146 million—the company forecasts robust earnings growth of 23.9% annually, surpassing the Swedish market's average growth rate, though revenue growth remains moderate at 4.5%, with an unstable dividend history noted.

- According our earnings growth report, there's an indication that Ratos might be ready to expand.

- Dive into the specifics of Ratos here with our thorough financial health report.

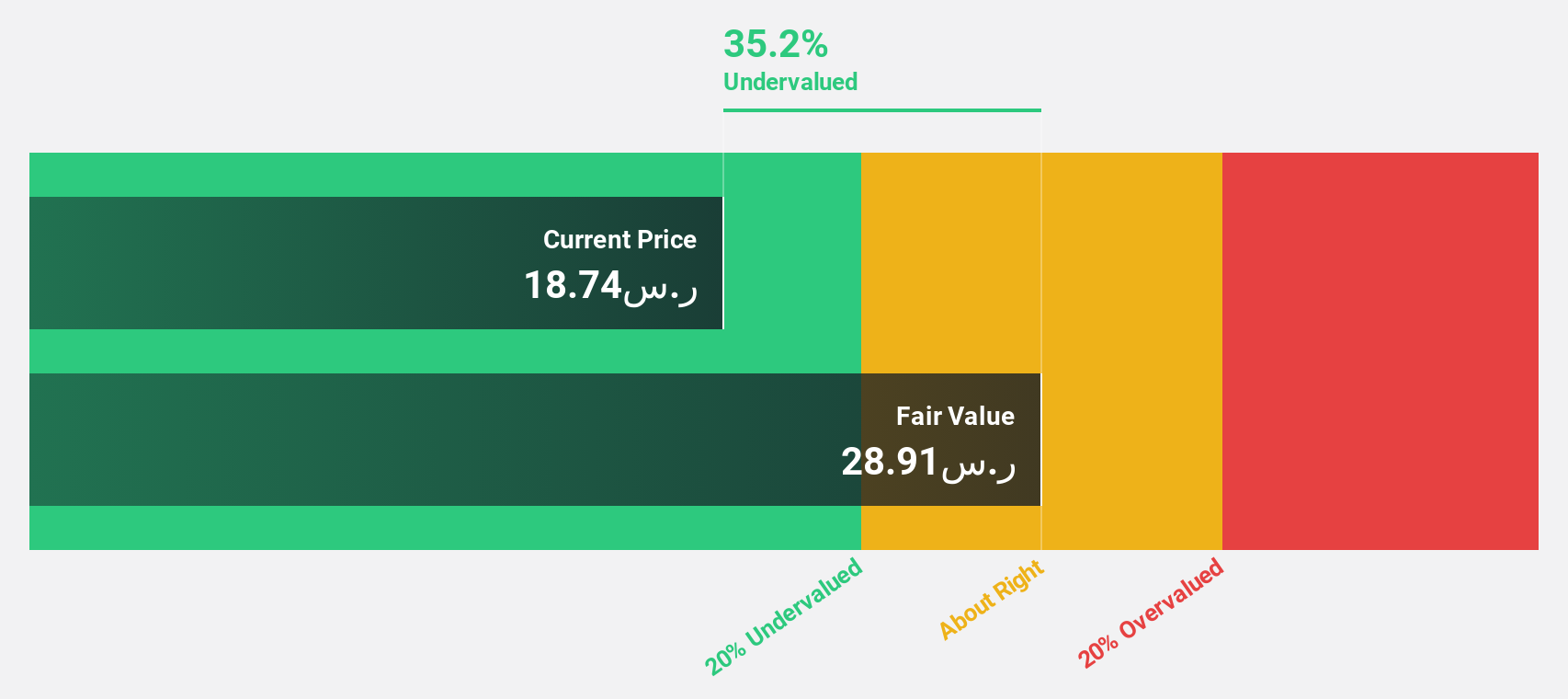

Yanbu Cement (SASE:3060)

Overview: Yanbu Cement Company, with a market cap of SAR3.84 billion, is involved in the manufacturing, production, and trading of cement and related products both within Saudi Arabia and internationally.

Operations: The company generates revenue primarily through its manufacturing cement segment, which accounts for SAR822.17 million.

Estimated Discount To Fair Value: 42.1%

Yanbu Cement, trading below its estimated fair value of SAR 42.12 at SAR 24.4, appears significantly undervalued based on discounted cash flow analysis. Recent earnings report shows Q3 sales of SAR 199.87 million and net income of SAR 31.1 million, with basic EPS at SAR 0.2. While earnings are expected to grow significantly at 23.19% annually, surpassing the SA market's growth rate, the dividend yield is not well covered by free cash flows.

- Insights from our recent growth report point to a promising forecast for Yanbu Cement's business outlook.

- Click here to discover the nuances of Yanbu Cement with our detailed financial health report.

Seize The Opportunity

- Investigate our full lineup of 901 Undervalued Stocks Based On Cash Flows right here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SASE:3060

Yanbu Cement

Engages in manufacturing, producing, and trading of cement and related products in the Kingdom of Saudi Arabia and internationally.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor