Atlas Copco (OM:ATCO A) Margin Slips to 16.2%, Testing Premium Valuation Narrative

Reviewed by Simply Wall St

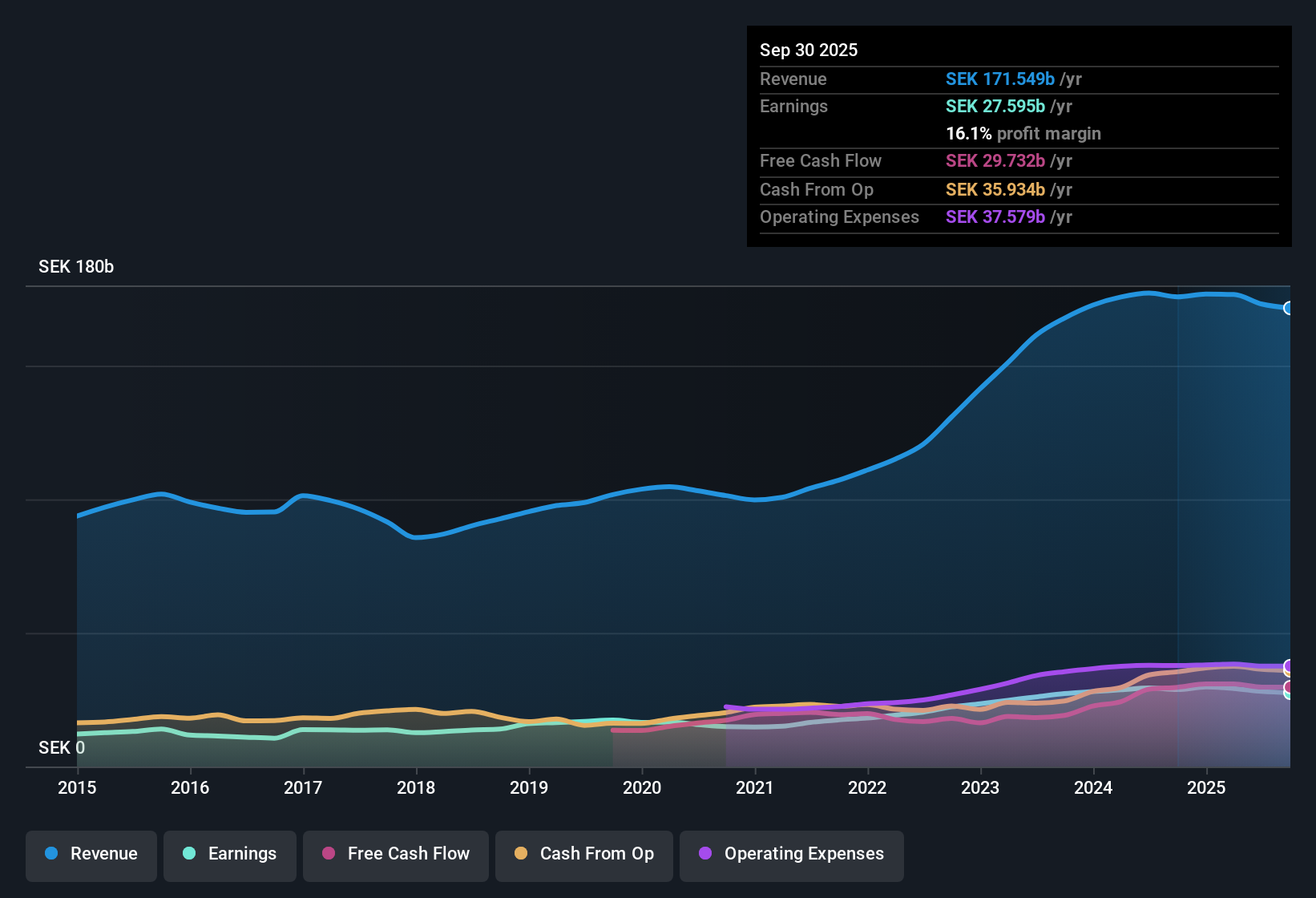

Atlas Copco (OM:ATCO A) reported earnings growth forecasts of 9% per year, which trails the projected Swedish market growth rate of 12.3%. However, the company is expected to outpace the broader market on revenue growth, with forecasts at 6.3% compared to the market’s 3.6%. Net profit margins are currently at 16.2%, slightly below last year’s 16.6%. The business continues to show high-quality earnings performance with no flagged risks from recent data.

See our full analysis for Atlas Copco.The next section puts these headline results side by side with the dominant narratives around Atlas Copco, highlighting where the numbers confirm expectations and where fresh debates could emerge.

See what the community is saying about Atlas Copco

Margins Rebound Expected by 2028

- Analysts expect profit margins to lift from 16.2% now to 16.9% by 2028, signaling confidence that cost controls and higher-margin services can offset near-term softness in equipment orders.

- According to the consensus narrative, recurring service revenue and digital innovation are seen as key levers supporting margin stability, even as large-project orders have slowed.

- Initiatives in automation and new product launches, such as the GHS pump VSD+, help differentiate Atlas Copco and sustain premium pricing through market cycles.

- Expanding high-margin service and aftermarket segments help smooth group-wide volatility, anchoring margins even if industrial demand fluctuates.

- The projected margin recovery reinforces broader analyst expectations for Atlas Copco, with the recovery directly linked to continued investment in efficiency and recurring revenue streams.

Consensus narrative suggests Atlas Copco's margin outlook is bolstered by growing service revenue, but the big question is whether innovation offsets the impact of choppier equipment demand. 📊 Read the full Atlas Copco Consensus Narrative.

Share Price Commands a Premium

- Atlas Copco trades at a price-to-earnings ratio of 28.5x, well above both the industry average of 23.5x and the peer group average of 26x. This highlights that the market rewards its growth profile with a premium valuation.

- Review of the analysts' consensus view highlights that this premium is justified given above-market revenue guidance as well as the company's record of high-quality earnings.

- The forecast annual revenue growth of 6.3% for Atlas Copco notably outpaces the broader Swedish market’s 3.6%, which helps explain the justifiable premium versus sector averages.

- Analysts estimate a DCF fair value of SEK137.66 per share compared to the current share price of SEK164.40. The premium likely hinges on belief in future upgrades or upside not yet captured by discounted cash flow estimates.

Long-Term Growth Outpaces Equipment Headwinds

- Despite a slowdown in large-order demand, analysts are forecasting annual earnings growth of 9% and revenue growth of 4.7% over the next three years, helped by robust demand for digital and energy-efficient solutions.

- The consensus narrative points out how global infrastructure spending and emerging market expansion act as tailwinds, even when some segments face cyclic slowing.

- Periods of hesitation in industrial investment, most visible in compressor and gas projects, are offset by Atlas Copco's strong ongoing project pipeline and lack of order cancellations. This signals that pent-up demand may soon rebound.

- Execution of restructuring programs and increased focus on aftermarket services are already helping stabilize group performance, even amid currency headwinds or cyclical dips in core equipment areas.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Atlas Copco on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have a unique take on the figures? You can craft your perspective and shape your own interpretation in just a few minutes. Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Atlas Copco.

See What Else Is Out There

Atlas Copco’s premium valuation hinges on future upgrades, as current DCF estimates do not justify the share price and margin recovery is still unfolding.

If you want to spot opportunities trading below intrinsic value right now, search for stronger potential with these 876 undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:ATCO A

Atlas Copco

Provides compressed air and gas, vacuum, energy, dewatering and industrial pumps, industrial power tools, and assembly and machine vision solutions in North America, South America, Europe, Africa, the Middle East, Asia, and Oceania.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)