Digital Push and Acquisitions Could Be a Game Changer for ASSA ABLOY (OM:ASSA B)

Reviewed by Sasha Jovanovic

- ASSA ABLOY reported strong organic sales growth in EMEIA, Entrance Systems, Global Technologies, and Americas during the third quarter of 2025, while completing five acquisitions and experiencing a sales decline in Asia Pacific.

- The company is accelerating its transition from mechanical to electromechanical solutions, responding to growing demand for safety, digitalization, IoT, and mobile access technologies.

- We'll examine how the recent acquisitions and focus on digital technologies could reshape ASSA ABLOY's investment narrative and outlook.

Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

ASSA ABLOY Investment Narrative Recap

To be a shareholder in ASSA ABLOY, you should have confidence in the company’s ability to capitalize on the shift toward digital and smart access solutions, while balancing global demand trends. The recent organic sales growth in EMEIA and Americas boosts near-term momentum for digital access products, but the ongoing sales decline in Asia Pacific does not materially change the current catalyst: accelerating technology adoption in access solutions; the main risk remains integration and margin pressures from frequent acquisitions.

The announcement of five completed acquisitions in the third quarter is especially relevant, as it expands ASSA ABLOY’s technology and product reach and could drive additional growth in high-margin business lines if integration is successful. These ongoing additions support the company’s push for greater revenue diversification and reinforce the catalyst of expanding digital offerings and service-based solutions across multiple markets.

Yet, in contrast to these growth drivers, investors should be aware of the risk that ongoing acquisitions could increase operating costs and potentially dilute margins if...

Read the full narrative on ASSA ABLOY (it's free!)

ASSA ABLOY's narrative projects SEK176.9 billion revenue and SEK20.6 billion earnings by 2028. This requires 5.0% yearly revenue growth and a SEK6.1 billion earnings increase from SEK14.5 billion today.

Uncover how ASSA ABLOY's forecasts yield a SEK355.75 fair value, a 4% upside to its current price.

Exploring Other Perspectives

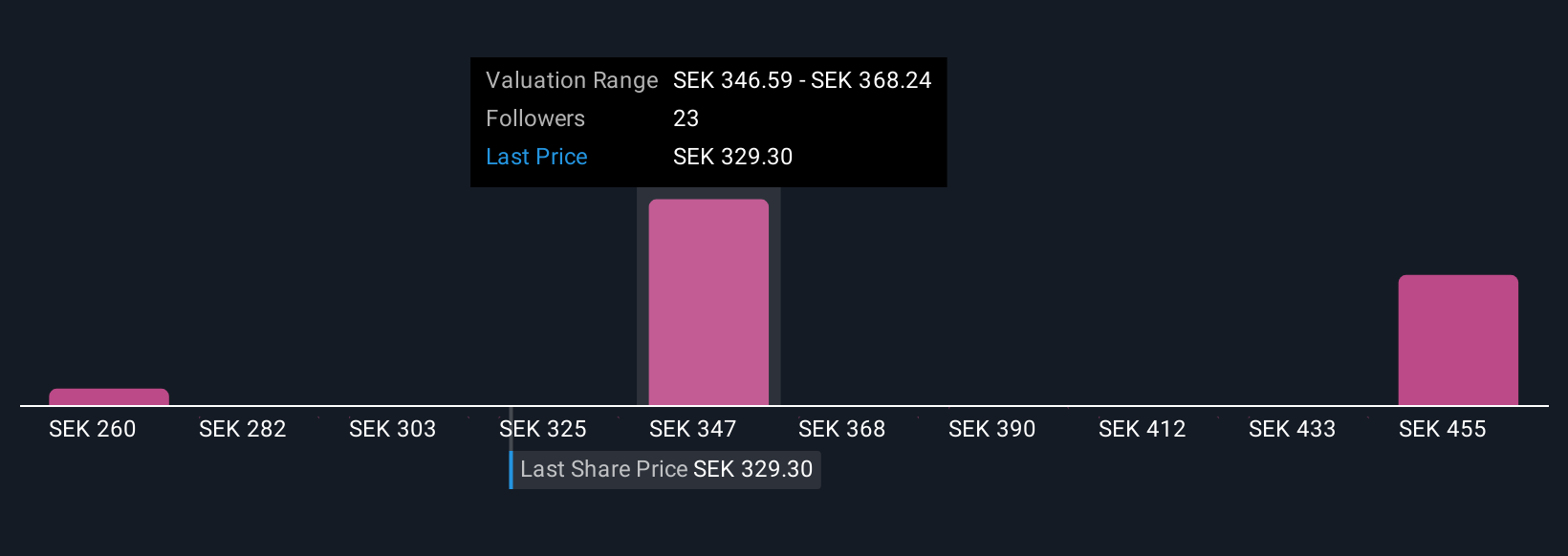

Seven different fair value estimates from the Simply Wall St Community range between SEK 260 and SEK 477,359. While many see upside in digital expansion and acquisitions, differences in forecasts show just how much opinions on ASSA ABLOY’s future earnings quality can vary.

Explore 7 other fair value estimates on ASSA ABLOY - why the stock might be worth 24% less than the current price!

Build Your Own ASSA ABLOY Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ASSA ABLOY research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ASSA ABLOY research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ASSA ABLOY's overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:ASSA B

ASSA ABLOY

Provides door opening and access products for the institutional, commercial, and residential markets.

Good value average dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)