- Saudi Arabia

- /

- Transportation

- /

- SASE:4260

Can Mixed Financials Have A Negative Impact on United International Transportation Company's 's (TADAWUL:4260) Current Price Momentum?

United International Transportation's (TADAWUL:4260) stock up by 8.2% over the past three months. However, we decided to study the company's mixed-bag of fundamentals to assess what this could mean for future share prices, as stock prices tend to be aligned with a company's long-term financial performance. In this article, we decided to focus on United International Transportation's ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

View our latest analysis for United International Transportation

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for United International Transportation is:

13% = ر.س157m ÷ ر.س1.2b (Based on the trailing twelve months to September 2020).

The 'return' is the yearly profit. That means that for every SAR1 worth of shareholders' equity, the company generated SAR0.13 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

United International Transportation's Earnings Growth And 13% ROE

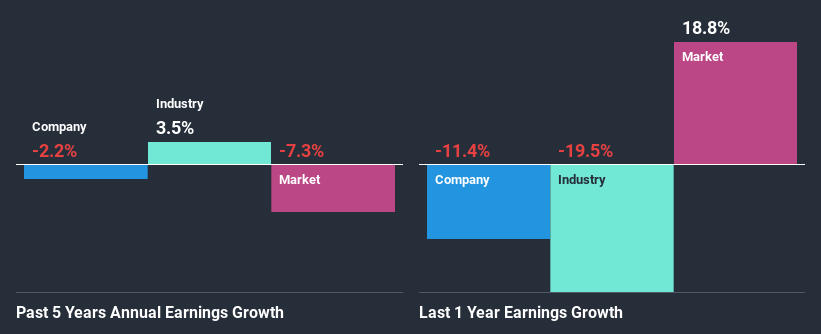

When you first look at it, United International Transportation's ROE doesn't look that attractive. However, the fact that the company's ROE is higher than the average industry ROE of 6.0%, is definitely interesting. But then again, seeing that United International Transportation's net income shrunk at a rate of 2.2% in the past five years, makes us think again. Bear in mind, the company does have a slightly low ROE. It is just that the industry ROE is lower. Therefore, the decline in earnings could also be the result of this.

However, when we compared United International Transportation's growth with the industry we found that while the company's earnings have been shrinking, the industry has seen an earnings growth of 5.8% in the same period. This is quite worrisome.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. If you're wondering about United International Transportation's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is United International Transportation Efficiently Re-investing Its Profits?

With a high three-year median payout ratio of 63% (implying that 37% of the profits are retained), most of United International Transportation's profits are being paid to shareholders, which explains the company's shrinking earnings. The business is only left with a small pool of capital to reinvest - A vicious cycle that doesn't benefit the company in the long-run.

Additionally, United International Transportation has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 69% of its profits over the next three years. As a result, United International Transportation's ROE is not expected to change by much either, which we inferred from the analyst estimate of 16% for future ROE.

Summary

In total, we're a bit ambivalent about United International Transportation's performance. Specifically, the low earnings growth is a bit concerning, especially given that the company has a respectable rate of return. Investors may have benefitted, had the company been reinvesting more of its earnings. As discussed earlier, the company is retaining a small portion of its profits. With that said, we studied the latest analyst forecasts and found that while the company has shrunk its earnings in the past, analysts expect its earnings to grow in the future. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

If you decide to trade United International Transportation, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SASE:4260

United International Transportation

Engages in the leasing and rental of vehicles, and used car sales under the Budget Rent a Car name in Saudi Arabia.

Proven track record and fair value.

Similar Companies

Market Insights

Community Narratives