- Saudi Arabia

- /

- Wireless Telecom

- /

- SASE:7020

Etihad Etisalat Company's (TADAWUL:7020) Stock On An Uptrend: Could Fundamentals Be Driving The Momentum?

Most readers would already be aware that Etihad Etisalat's (TADAWUL:7020) stock increased significantly by 15% over the past three months. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to study its financial indicators more closely to see if they had a hand to play in the recent price move. Specifically, we decided to study Etihad Etisalat's ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

See our latest analysis for Etihad Etisalat

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Etihad Etisalat is:

16% = ر.س2.9b ÷ ر.س18b (Based on the trailing twelve months to September 2024).

The 'return' is the yearly profit. So, this means that for every SAR1 of its shareholder's investments, the company generates a profit of SAR0.16.

Why Is ROE Important For Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Etihad Etisalat's Earnings Growth And 16% ROE

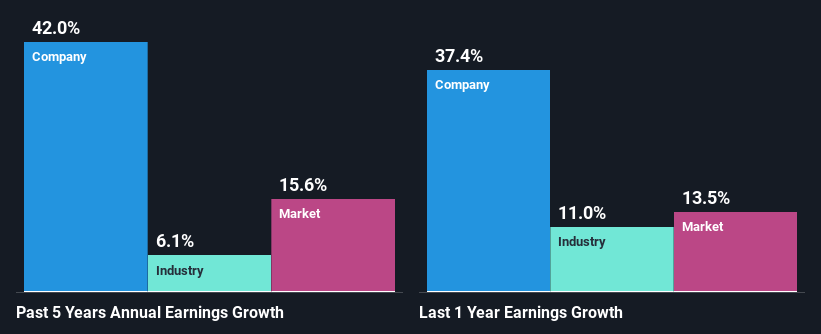

As you can see, Etihad Etisalat's ROE looks pretty weak. However, when compared to the industry average of 12%, we do feel there's definitely more to the company. Particularly, the substantial 42% net income growth seen by Etihad Etisalat over the past five years is impressive . That being said, the company does have a low ROE to begin with, just that its higher than the industry average. Therefore, the growth in earnings could also be the result of other factors. For instance, the company has a low payout ratio or is being managed efficiently

As a next step, we compared Etihad Etisalat's net income growth with the industry, and pleasingly, we found that the growth seen by the company is higher than the average industry growth of 6.1%.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. Is 7020 fairly valued? This infographic on the company's intrinsic value has everything you need to know.

Is Etihad Etisalat Using Its Retained Earnings Effectively?

The high three-year median payout ratio of 50% (implying that it keeps only 50% of profits) for Etihad Etisalat suggests that the company's growth wasn't really hampered despite it returning most of the earnings to its shareholders.

Besides, Etihad Etisalat has been paying dividends for at least ten years or more. This shows that the company is committed to sharing profits with its shareholders. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to rise to 61% over the next three years. However, the company's ROE is not expected to change by much despite the higher expected payout ratio.

Conclusion

Overall, we feel that Etihad Etisalat certainly does have some positive factors to consider. Namely, its significant earnings growth, to which its moderate rate of return likely contributed. While the company is paying out most of its earnings as dividends, it has been able to grow its earnings in spite of it, so that's probably a good sign. With that said, the latest industry analyst forecasts reveal that the company's earnings growth is expected to slow down. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

Valuation is complex, but we're here to simplify it.

Discover if Etihad Etisalat might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:7020

Etihad Etisalat

Through its subsidiaries, establishes and operates mobile wireless telecommunication and fiber optic networks in the Kingdom of Saudi Arabia.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives