Advertisement

- Romania

- /

- Food and Staples Retail

- /

- BVB:RMAH

Returns Are Gaining Momentum At Farmaceutica REMEDIA (BVB:RMAH)

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. So when we looked at Farmaceutica REMEDIA (BVB:RMAH) and its trend of ROCE, we really liked what we saw.

What is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Farmaceutica REMEDIA is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

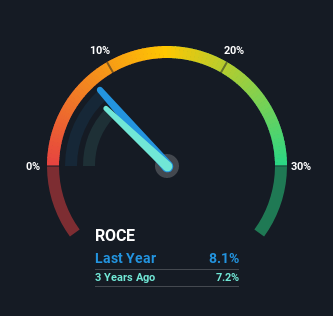

0.081 = RON6.3m ÷ (RON246m - RON168m) (Based on the trailing twelve months to March 2021).

Thus, Farmaceutica REMEDIA has an ROCE of 8.1%. On its own, that's a low figure but it's around the 9.4% average generated by the Consumer Retailing industry.

See our latest analysis for Farmaceutica REMEDIA

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Farmaceutica REMEDIA's past further, check out this free graph of past earnings, revenue and cash flow.

So How Is Farmaceutica REMEDIA's ROCE Trending?

Farmaceutica REMEDIA has recently broken into profitability so their prior investments seem to be paying off. The company was generating losses five years ago, but now it's earning 8.1% which is a sight for sore eyes. Not only that, but the company is utilizing 92% more capital than before, but that's to be expected from a company trying to break into profitability. This can tell us that the company has plenty of reinvestment opportunities that are able to generate higher returns.

On a side note, Farmaceutica REMEDIA's current liabilities are still rather high at 68% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

What We Can Learn From Farmaceutica REMEDIA's ROCE

Overall, Farmaceutica REMEDIA gets a big tick from us thanks in most part to the fact that it is now profitable and is reinvesting in its business. And with the stock having performed exceptionally well over the last five years, these patterns are being accounted for by investors. In light of that, we think it's worth looking further into this stock because if Farmaceutica REMEDIA can keep these trends up, it could have a bright future ahead.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 4 warning signs for Farmaceutica REMEDIA (of which 1 makes us a bit uncomfortable!) that you should know about.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BVB:RMAH

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|29.6% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|49.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.8% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.2% undervalued

AX

Community Contributor