Advertisement

- Poland

- /

- Entertainment

- /

- WSE:CIG

Time To Worry? Analysts Are Downgrading Their CI Games SE (WSE:CIG) Outlook

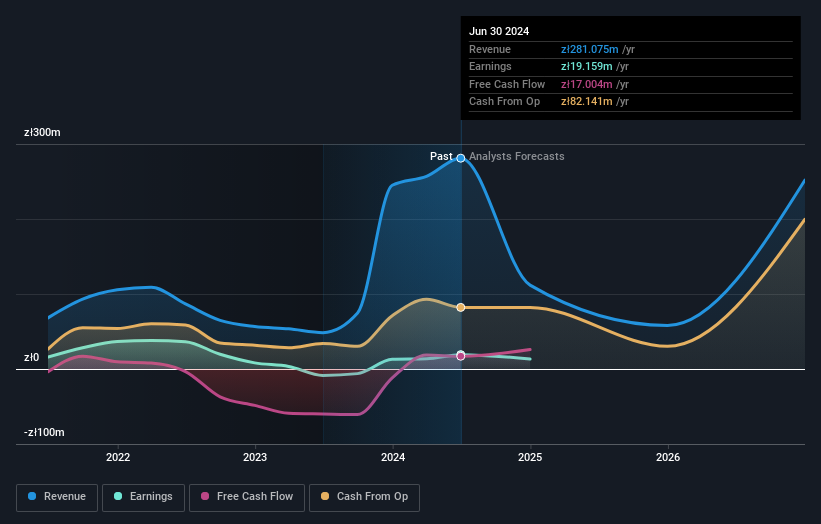

The latest analyst coverage could presage a bad day for CI Games SE (WSE:CIG), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Revenue and earnings per share (EPS) forecasts were both revised downwards, with the analysts seeing grey clouds on the horizon. At zł1.61, shares are up 7.5% in the past 7 days. It will be interesting to see if this downgrade motivates investors to start selling their holdings.

After the downgrade, the consensus from CI Games' dual analysts is for revenues of zł112m in 2024, which would reflect a substantial 60% decline in sales compared to the last year of performance. Statutory earnings per share are supposed to plummet 67% to zł0.035 in the same period. Previously, the analysts had been modelling revenues of zł140m and earnings per share (EPS) of zł0.07 in 2024. It looks like analyst sentiment has declined substantially, with a sizeable cut to revenue estimates and a large cut to earnings per share numbers as well.

See our latest analysis for CI Games

The consensus price target fell 29% to zł3.40, with the weaker earnings outlook clearly leading analyst valuation estimates.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 60% by the end of 2024. This indicates a significant reduction from annual growth of 37% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 11% per year. It's pretty clear that CI Games' revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. Given the scope of the downgrades, it would not be a surprise to see the market become more wary of the business.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At least one analyst has provided forecasts out to 2026, which can be seen for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:CIG

CI Games

Produces, publishes, and distributes video games in Europe, North and South America, Asia, and Africa.

High growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor