- Poland

- /

- Healthcare Services

- /

- WSE:NEU

We Think Shareholders May Want To Consider A Review Of NEUCA S.A.'s (WSE:NEU) CEO Compensation Package

Key Insights

- NEUCA's Annual General Meeting to take place on 17th of June

- Salary of zł1.16m is part of CEO Piotr Sucharski's total remuneration

- The overall pay is comparable to the industry average

- NEUCA's three-year loss to shareholders was 2.0% while its EPS was down 3.9% over the past three years

NEUCA S.A. (WSE:NEU) has not performed well recently and CEO Piotr Sucharski will probably need to up their game. Shareholders can take the chance to hold the board and management accountable for the unsatisfactory performance at the next AGM on 17th of June. They will also get a chance to influence managerial decision-making through voting on resolutions such as executive remuneration, which may impact firm value in the future. From our analysis, we think CEO compensation may need a review in light of the recent performance.

Check out our latest analysis for NEUCA

Comparing NEUCA S.A.'s CEO Compensation With The Industry

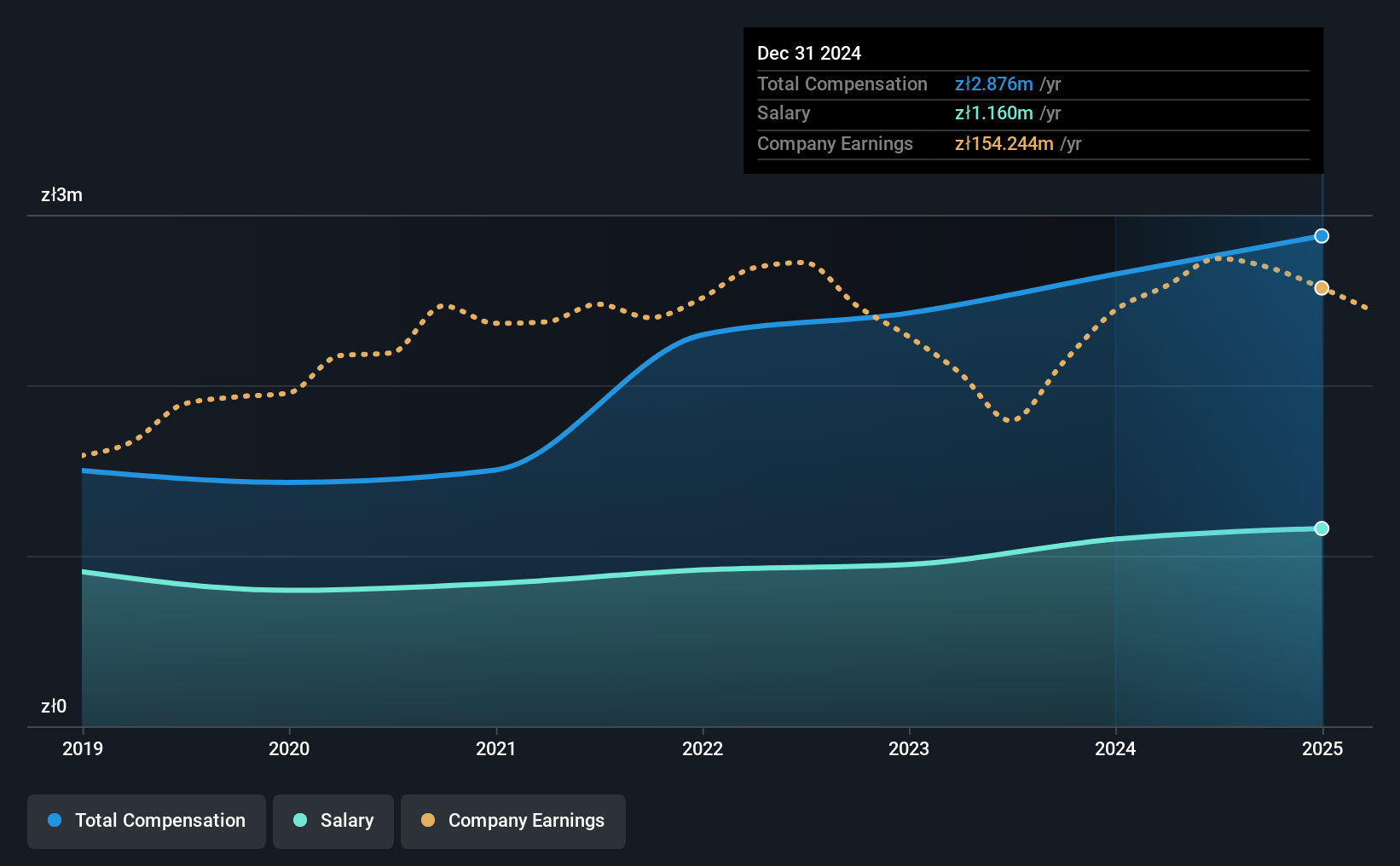

Our data indicates that NEUCA S.A. has a market capitalization of zł3.1b, and total annual CEO compensation was reported as zł2.9m for the year to December 2024. We note that's an increase of 8.5% above last year. We think total compensation is more important but our data shows that the CEO salary is lower, at zł1.2m.

For comparison, other companies in the Poland Healthcare industry with market capitalizations ranging between zł1.5b and zł6.0b had a median total CEO compensation of zł3.8m. This suggests that NEUCA remunerates its CEO largely in line with the industry average. Moreover, Piotr Sucharski also holds zł45m worth of NEUCA stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | zł1.2m | zł1.1m | 40% |

| Other | zł1.7m | zł1.6m | 60% |

| Total Compensation | zł2.9m | zł2.7m | 100% |

Speaking on an industry level, nearly 57% of total compensation represents salary, while the remainder of 43% is other remuneration. In NEUCA's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

NEUCA S.A.'s Growth

Over the last three years, NEUCA S.A. has shrunk its earnings per share by 3.9% per year. In the last year, its revenue is up 7.0%.

The decline in EPS is a bit concerning. And the modest revenue growth over 12 months isn't much comfort against the reduced EPS. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has NEUCA S.A. Been A Good Investment?

With a three year total loss of 2.0% for the shareholders, NEUCA S.A. would certainly have some dissatisfied shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

Shareholders may want to check for free if NEUCA insiders are buying or selling shares.

Switching gears from NEUCA, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if NEUCA might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:NEU

NEUCA

Engages in the wholesale distribution of pharmaceuticals in Poland.

Average dividend payer and fair value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)