Advertisement

- Poland

- /

- Consumer Finance

- /

- WSE:KRU

This Is The Reason Why We Think KRUK Spólka Akcyjna's (WSE:KRU) CEO Might Be Underpaid

Key Insights

- KRUK Spólka Akcyjna to hold its Annual General Meeting on 10th of May

- Total pay for CEO Piotr Krupa includes zł3.11m salary

- Total compensation is 40% below industry average

- KRUK Spólka Akcyjna's EPS grew by 128% over the past three years while total shareholder return over the past three years was 172%

Shareholders will be pleased by the impressive results for KRUK Spólka Akcyjna (WSE:KRU) recently and CEO Piotr Krupa has played a key role. This would be kept in mind at the upcoming AGM on 10th of May which will be a chance for them to hear the board review the financial results, discuss future company strategy and vote on resolutions such as executive remuneration and other matters. Here we will show why we think CEO compensation is appropriate and discuss the case for a pay rise.

See our latest analysis for KRUK Spólka Akcyjna

Comparing KRUK Spólka Akcyjna's CEO Compensation With The Industry

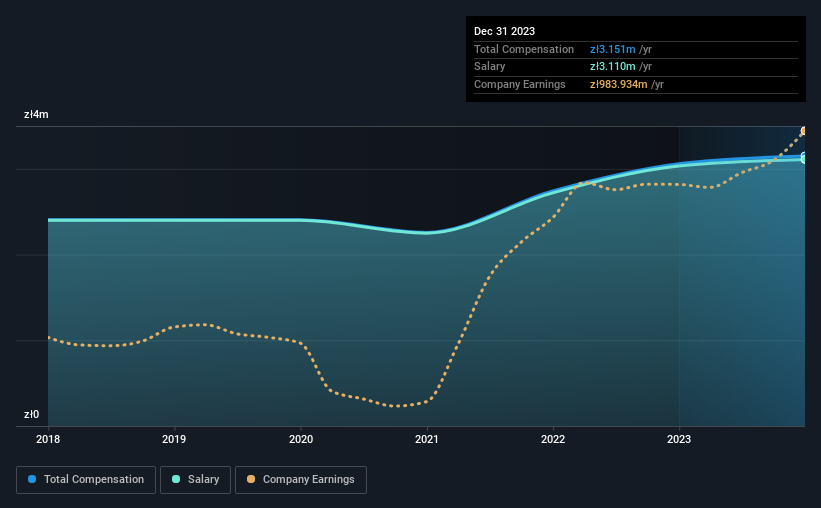

At the time of writing, our data shows that KRUK Spólka Akcyjna has a market capitalization of zł8.9b, and reported total annual CEO compensation of zł3.2m for the year to December 2023. That is, the compensation was roughly the same as last year. Notably, the salary which is zł3.11m, represents most of the total compensation being paid.

On comparing similar companies from the Poland Consumer Finance industry with market caps ranging from zł4.0b to zł13b, we found that the median CEO total compensation was zł5.3m. Accordingly, KRUK Spólka Akcyjna pays its CEO under the industry median. Moreover, Piotr Krupa also holds zł799m worth of KRUK Spólka Akcyjna stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | zł3.1m | zł3.0m | 99% |

| Other | zł40k | zł26k | 1% |

| Total Compensation | zł3.2m | zł3.1m | 100% |

On an industry level, around 57% of total compensation represents salary and 43% is other remuneration. KRUK Spólka Akcyjna is focused on going down a more traditional approach and is paying a higher portion of compensation through salary, as compared to non-salary benefits. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

KRUK Spólka Akcyjna's Growth

Over the past three years, KRUK Spólka Akcyjna has seen its earnings per share (EPS) grow by 128% per year. Its revenue is up 20% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's a real positive to see this sort of revenue growth in a single year. That suggests a healthy and growing business. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has KRUK Spólka Akcyjna Been A Good Investment?

Most shareholders would probably be pleased with KRUK Spólka Akcyjna for providing a total return of 172% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

Piotr receives almost all of their compensation through a salary. Given the company's decent performance, the CEO remuneration policy might not be shareholders' central point of focus in the AGM. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. In our study, we found 3 warning signs for KRUK Spólka Akcyjna you should be aware of, and 2 of them shouldn't be ignored.

Important note: KRUK Spólka Akcyjna is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if KRUK Spólka Akcyjna might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:KRU

KRUK Spólka Akcyjna

Engages in the management of debt in Poland, Romania, Italy, the Czech Republic, Slovakia, Germany, Spain, and internationally.

Very undervalued second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor