Advertisement

- Poland

- /

- Food and Staples Retail

- /

- WSE:ORG

ORGANIC Farma Zdrowia S.A.'s (WSE:ORG) 28% Price Boost Is Out Of Tune With Earnings

ORGANIC Farma Zdrowia S.A. (WSE:ORG) shares have had a really impressive month, gaining 28% after a shaky period beforehand. The annual gain comes to 260% following the latest surge, making investors sit up and take notice.

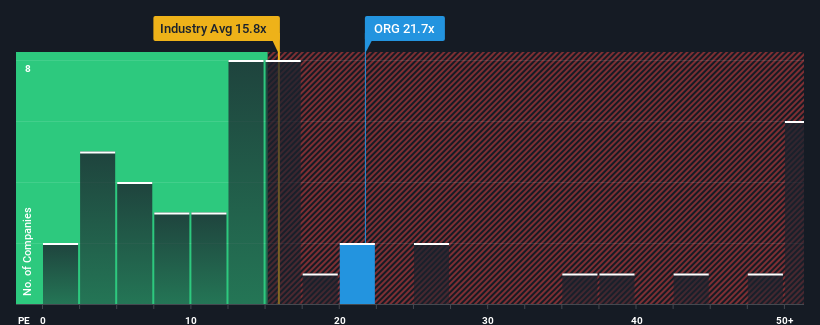

Since its price has surged higher, ORGANIC Farma Zdrowia may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 21.7x, since almost half of all companies in Poland have P/E ratios under 11x and even P/E's lower than 7x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

For instance, ORGANIC Farma Zdrowia's receding earnings in recent times would have to be some food for thought. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. If not, then existing shareholders may be quite nervous about the viability of the share price.

See our latest analysis for ORGANIC Farma Zdrowia

Is There Enough Growth For ORGANIC Farma Zdrowia?

ORGANIC Farma Zdrowia's P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

Retrospectively, the last year delivered a frustrating 51% decrease to the company's bottom line. This has erased any of its gains during the last three years, with practically no change in EPS being achieved in total. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 13% shows it's noticeably less attractive on an annualised basis.

With this information, we find it concerning that ORGANIC Farma Zdrowia is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with recent growth rates.

The Key Takeaway

Shares in ORGANIC Farma Zdrowia have built up some good momentum lately, which has really inflated its P/E. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that ORGANIC Farma Zdrowia currently trades on a much higher than expected P/E since its recent three-year growth is lower than the wider market forecast. When we see weak earnings with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 5 warning signs with ORGANIC Farma Zdrowia (at least 3 which are significant), and understanding these should be part of your investment process.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:ORG

ORGANIC Farma Zdrowia

Operates a retail chain of organic products in Poland and internationally.

Adequate balance sheet slight.

Market Insights

Advertisement

Community Narratives

Quality Assets, Cautious Expansion and Commodity Super-cycle To Deliver Steady Revenue Growth

Fair Value US$20.44|13.7% undervalued

ST

Equity Analyst and Writer

Tullow Oil's Share Price Could Soar Up to 135% if Oil Holds at $70

Fair Value UK£0.45|69.6% undervalued

OI

Community Contributor