Advertisement

- United Kingdom

- /

- Retail REITs

- /

- LSE:SUPR

Global Undervalued Small Caps With Insider Action

Simply Wall St

Reviewed by Simply Wall St

As global markets grapple with trade policy uncertainties and fluctuating economic indicators, small-cap stocks have experienced notable volatility, with indices like the Russell 2000 seeing significant declines. Amid these turbulent conditions, identifying promising small-cap opportunities involves looking for companies that demonstrate resilience through strong fundamentals and strategic insider actions, which may signal confidence in their long-term potential.

Top 10 Undervalued Small Caps With Insider Buying Globally

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Bytes Technology Group | 19.0x | 4.8x | 25.97% | ★★★★★★ |

| Nexus Industrial REIT | 5.4x | 2.8x | 25.07% | ★★★★★★ |

| 4imprint Group | 15.7x | 1.3x | 37.73% | ★★★★★☆ |

| Speedy Hire | NA | 0.2x | 25.96% | ★★★★★☆ |

| Robert Walters | NA | 0.2x | 45.70% | ★★★★★☆ |

| Chorus Aviation | NA | 0.4x | 5.40% | ★★★★★☆ |

| Hong Leong Asia | 8.9x | 0.2x | 46.31% | ★★★★☆☆ |

| Franchise Brands | 38.3x | 2.0x | 26.82% | ★★★★☆☆ |

| Sing Investments & Finance | 7.2x | 3.7x | 36.69% | ★★★★☆☆ |

| Optima Health | NA | 1.5x | 45.68% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

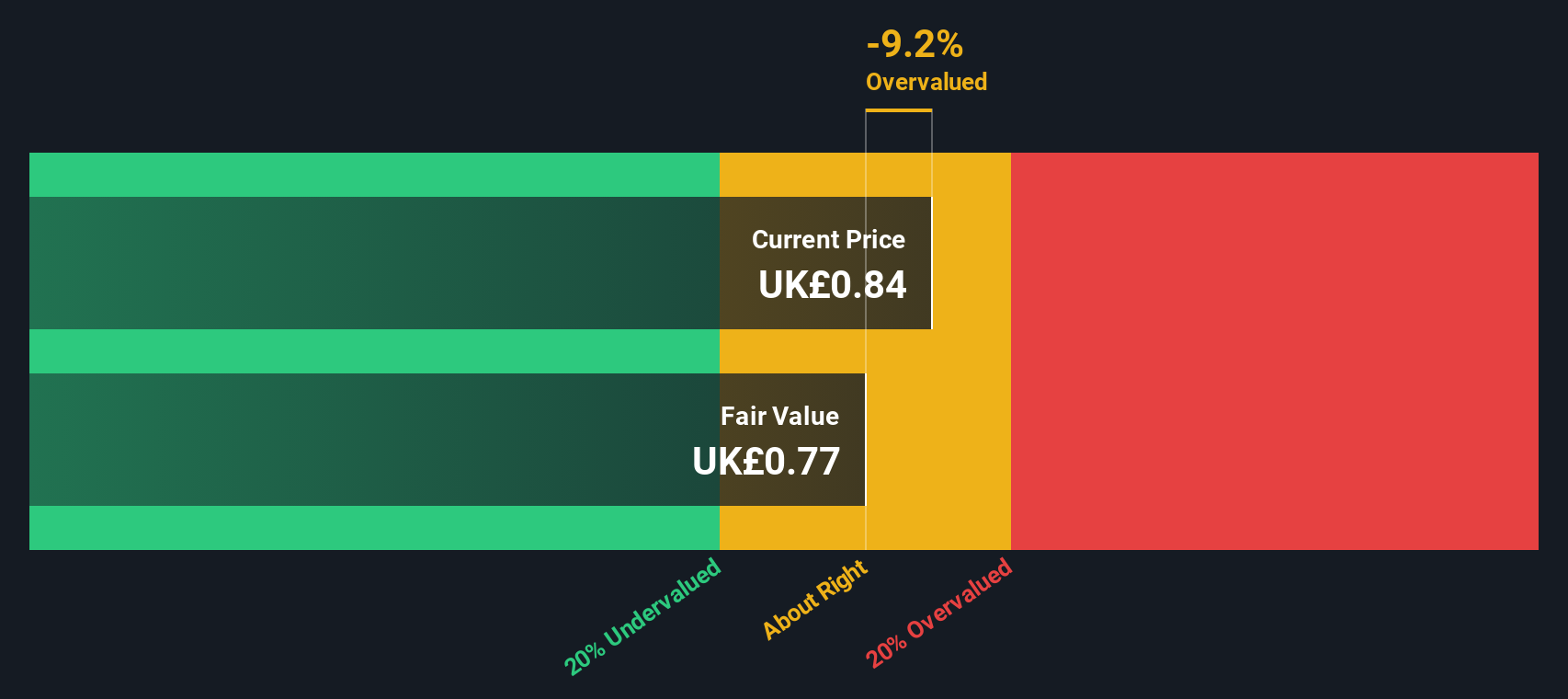

Supermarket Income REIT (LSE:SUPR)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Supermarket Income REIT is a UK-based real estate investment trust focused on acquiring and managing supermarket properties, with a market cap of approximately £1.48 billion.

Operations: The primary revenue stream is from real estate investment, with a gross profit margin consistently at 100%. Operating expenses include general and administrative costs, which have shown fluctuations over time. Net income margins have varied significantly, with recent periods reflecting both positive and negative figures.

PE: 13.2x

Supermarket Income REIT, a smaller player in the real estate investment sector, recently reported a significant turnaround with net income of £36.53 million for the half-year ending December 31, 2024, compared to a loss last year. Insider confidence is evident from recent share purchases within the past year. Despite relying entirely on external borrowing for funding, earnings are projected to grow by 13% annually. The appointment of Roger Blundell as an independent director adds experienced leadership to navigate future opportunities and challenges in their niche market segment.

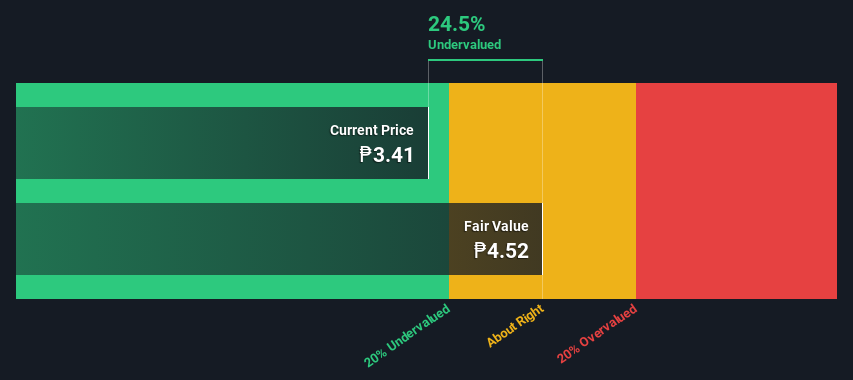

Bloomberry Resorts (PSE:BLOOM)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Bloomberry Resorts operates integrated resort facilities, focusing on gaming and entertainment, with a market capitalization of approximately ₱100.29 billion.

Operations: The company's primary revenue stream is from its Integrated Resort Facility, generating ₱52.76 billion. The gross profit margin has shown fluctuations, reaching 78.46% in December 2023 and then decreasing to 72.72% by December 2024.

PE: 14.9x

Bloomberry Resorts, a smaller player in the market, has seen insider confidence with Cyrus Sherafat acquiring over 9 million shares. Despite recent volatility and a challenging financial position with high external borrowing, the company is navigating its debt through strategic refinancing. Recent earnings showed increased sales but a net loss for Q4 2024. The board's decision to declare cash dividends indicates some optimism about future prospects despite current pressures on profit margins and share price stability.

- Take a closer look at Bloomberry Resorts' potential here in our valuation report.

Understand Bloomberry Resorts' track record by examining our Past report.

Robinsons Land (PSE:RLC)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Robinsons Land is a diversified real estate company operating in various segments including malls, offices, hotels and resorts, destination estates, logistics and industrial facilities, with a market capitalization of ₱101.92 billion.

Operations: Robinsons Land generates revenue primarily from its Malls, Residential Division, and Offices segments, with the Malls contributing ₱17.63 billion and the Residential Division adding ₱10.03 billion. The company's cost of goods sold (COGS) for the most recent period was ₱19.48 billion, leading to a gross profit margin of 55.30%. Operating expenses were recorded at ₱5.51 billion, while non-operating expenses amounted to ₱5.36 billion in the latest quarter ending March 2025.

PE: 4.4x

Robinsons Land, a key player in the hospitality sector, is expanding its Grand Summit hotel brand in Panglao, Bohol. This move aligns with the area's tourism growth and positions the company for potential revenue increases. Insider confidence is evident as they have been purchasing shares recently. However, reliance on external borrowing presents financial risks. Leadership changes with Maria Socorro Isabelle V. Aragon-GoBio as CEO might bring fresh strategic directions to capitalize on these opportunities and challenges.

- Get an in-depth perspective on Robinsons Land's performance by reading our valuation report here.

Assess Robinsons Land's past performance with our detailed historical performance reports.

Seize The Opportunity

- Gain an insight into the universe of 134 Undervalued Global Small Caps With Insider Buying by clicking here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:SUPR

Supermarket Income REIT

Supermarket Income REIT plc (LSE: SUPR) is a real estate investment trust dedicated to investing in grocery properties which are an essential part of the UK's feed the nation infrastructure.

Good value with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Enterprise, AI & Cloud Growth Ahead, Waiting For the Right Price 💸

Fair Value US$204.74|9.5% overvalued

FR

Community Contributor

Good foundation, but now it's all about the next steps

Fair Value US$147.87|27.6% undervalued

TO

Community Contributor

XTB's Path to 100–120 PLN by 2028 Amid Market Volatility

Fair Value zł100.96|36.6% undervalued

DZ

Community Contributor