Advertisement

- New Zealand

- /

- Food

- /

- NZSE:FCG

Shareholders May Not Be So Generous With Fonterra Co-operative Group Limited's (NZSE:FCG) CEO Compensation And Here's Why

Key Insights

- Fonterra Co-operative Group will host its Annual General Meeting on 14th of November

- Salary of NZ$2.46m is part of CEO Miles Hurrell's total remuneration

- Total compensation is 318% above industry average

- Fonterra Co-operative Group's EPS grew by 32% over the past three years while total shareholder return over the past three years was 103%

Under the guidance of CEO Miles Hurrell, Fonterra Co-operative Group Limited (NZSE:FCG) has performed reasonably well recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 14th of November. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

View our latest analysis for Fonterra Co-operative Group

How Does Total Compensation For Miles Hurrell Compare With Other Companies In The Industry?

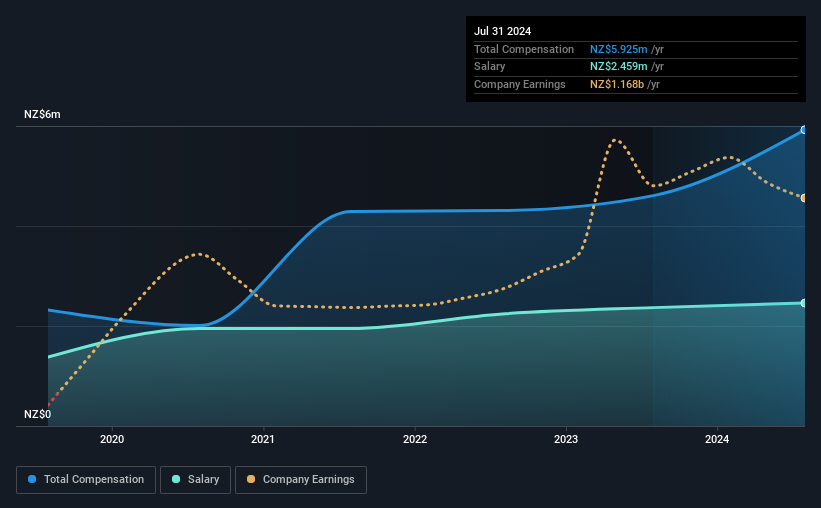

According to our data, Fonterra Co-operative Group Limited has a market capitalization of NZ$6.7b, and paid its CEO total annual compensation worth NZ$5.9m over the year to July 2024. We note that's an increase of 29% above last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at NZ$2.5m.

For comparison, other companies in the New Zealander Food industry with market capitalizations ranging between NZ$3.3b and NZ$11b had a median total CEO compensation of NZ$1.4m. Hence, we can conclude that Miles Hurrell is remunerated higher than the industry median.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | NZ$2.5m | NZ$2.4m | 42% |

| Other | NZ$3.5m | NZ$2.2m | 58% |

| Total Compensation | NZ$5.9m | NZ$4.6m | 100% |

On an industry level, roughly 65% of total compensation represents salary and 35% is other remuneration. In Fonterra Co-operative Group's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

Fonterra Co-operative Group Limited's Growth

Fonterra Co-operative Group Limited's earnings per share (EPS) grew 32% per year over the last three years. Its revenue is down 7.2% over the previous year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's always a tough situation when revenues are not growing, but ultimately profits are more important. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Fonterra Co-operative Group Limited Been A Good Investment?

We think that the total shareholder return of 103%, over three years, would leave most Fonterra Co-operative Group Limited shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 1 warning sign for Fonterra Co-operative Group that investors should think about before committing capital to this stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NZSE:FCG

Fonterra Co-operative Group

Fonterra Co-operative Group Limited, together with its subsidiaries, collects, manufactures, and sells milk and milk-derived products.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor