- Norway

- /

- Electric Utilities

- /

- OB:ELMRA

European Undervalued Small Caps With Insider Action In April 2025

Reviewed by Simply Wall St

As European markets experience a notable upswing, with the STOXX Europe 600 Index climbing 2.77% amid easing trade tensions and positive economic signals, small-cap stocks are drawing attention for their potential resilience and growth opportunities. In this environment, identifying promising small-cap stocks involves looking at those that may benefit from favorable market conditions while also considering factors such as insider activity, which can provide insights into the confidence levels of those closest to the companies' operations.

Top 10 Undervalued Small Caps With Insider Buying In Europe

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Morgan Advanced Materials | 10.9x | 0.5x | 41.54% | ★★★★★★ |

| Tristel | 27.2x | 3.8x | 27.82% | ★★★★★☆ |

| J D Wetherspoon | 11.7x | 0.4x | 33.83% | ★★★★★☆ |

| Savills | 23.6x | 0.5x | 43.78% | ★★★★☆☆ |

| Troax Group | 24.3x | 2.6x | 21.79% | ★★★☆☆☆ |

| Norcros | 23.9x | 0.6x | 28.80% | ★★★☆☆☆ |

| FRP Advisory Group | 12.0x | 2.1x | 12.04% | ★★★☆☆☆ |

| Speedy Hire | NA | 0.2x | -1.40% | ★★★☆☆☆ |

| FastPartner | 18.5x | 4.8x | -46.59% | ★★★☆☆☆ |

| Arendals Fossekompani | NA | 1.6x | 43.16% | ★★★☆☆☆ |

We'll examine a selection from our screener results.

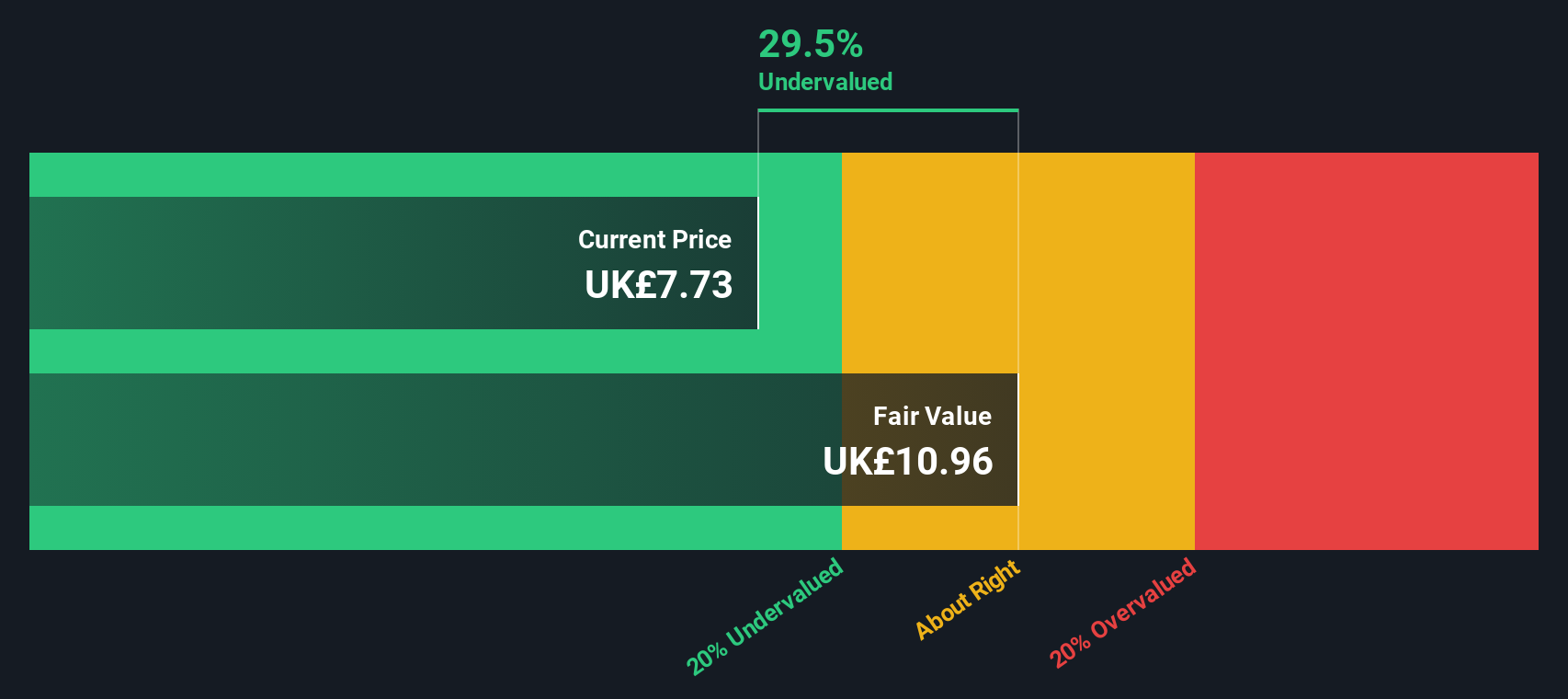

J D Wetherspoon (LSE:JDW)

Simply Wall St Value Rating: ★★★★★☆

Overview: J D Wetherspoon operates a chain of pubs across the UK and Ireland, with a market cap of approximately £1.01 billion.

Operations: The company generates revenue primarily from its pubs, with the latest reported revenue at £2.07 billion. Over recent periods, the gross profit margin has shown an upward trend, reaching 11.26% in early 2025 from a low of -24.63% in mid-2021. The cost of goods sold is a significant portion of expenses, impacting profitability alongside operating and non-operating expenses.

PE: 11.7x

J D Wetherspoon, a European company with a focus on pub operations, recently reported sales of £1.03 billion for the half-year ending January 26, 2025, up from £991 million the previous year. Net income rose to £32.23 million from £18.65 million last year, reflecting strong operational performance despite reliance on external borrowing for funding. Insider confidence is evident as insiders made share purchases in March 2025. The board declared an interim dividend of 4 pence per share after a hiatus in dividends last year, indicating cautious optimism about future prospects amidst ongoing financial challenges and growth forecasts of around 5% annually.

- Take a closer look at J D Wetherspoon's potential here in our valuation report.

Assess J D Wetherspoon's past performance with our detailed historical performance reports.

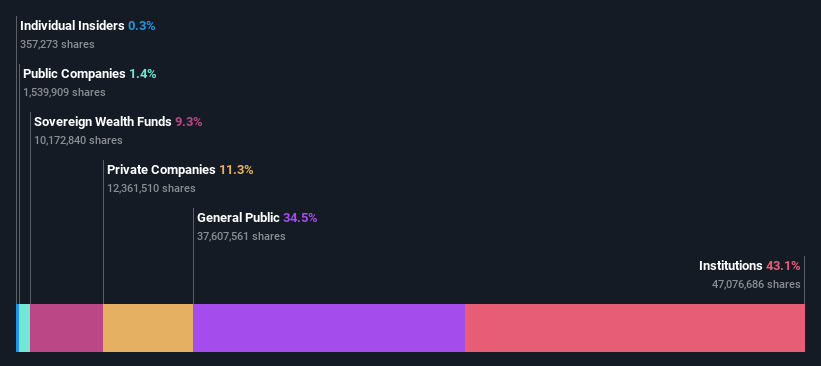

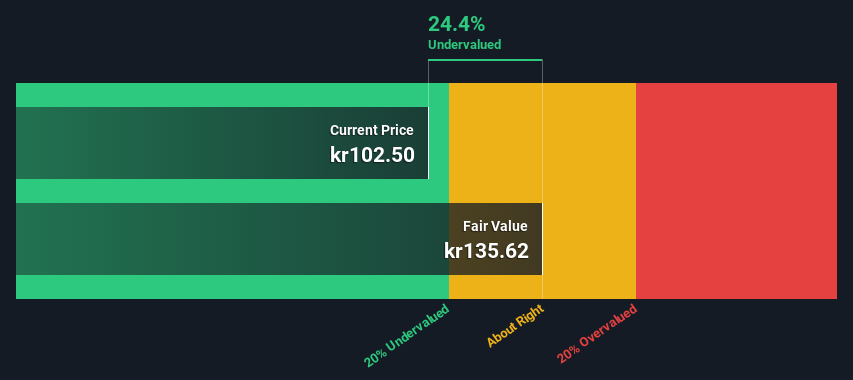

Elmera Group (OB:ELMRA)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Elmera Group operates across various segments including Nordic, Business, Consumer, and New Growth Initiatives with a focus on energy solutions and has a market capitalization of NOK 1.81 billion.

Operations: The company generates revenue primarily from its Consumer and Business segments, with significant contributions of NOK 5.46 billion and NOK 4.84 billion, respectively. Over recent periods, the gross profit margin has shown variability, reaching as high as 44.07% in December 2020 before declining to around 6.24% by June 2023 and later improving to approximately 14.53% by December 2024. Operating expenses have remained a notable component of costs, with general and administrative expenses being a consistent part of this category across various periods.

PE: 11.2x

Elmera Group, a smaller European company, has caught attention for its insider confidence with Henning Nordgulen purchasing 10,000 shares worth NOK 325,000. Despite challenges like earnings forecasted to decline by an average of 0.04% annually over the next three years and reliance on higher-risk external borrowing for funding, Elmera's recent performance shows promise. The company reported a significant increase in net income to NOK 206 million in Q4 2024 from NOK 88 million the previous year and announced a dividend of NOK 3 per share payable in May.

- Get an in-depth perspective on Elmera Group's performance by reading our valuation report here.

Review our historical performance report to gain insights into Elmera Group's's past performance.

Nordic Semiconductor (OB:NOD)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Nordic Semiconductor specializes in designing and manufacturing low-power wireless communication solutions for the Internet of Things (IoT) market, with a market capitalization of approximately NOK 21.79 billion.

Operations: The company generates revenue primarily through product sales, with recent figures showing a decline from $626.05 million in September 2023 to $591.99 million by March 2025. The gross profit margin has shown variability, peaking at 57.72% in September 2022 before decreasing to 47.81% by March 2025. Operating expenses have consistently been a significant portion of costs, impacting net income margins which turned negative starting from June 2024 onwards, reaching -11.67% by June of the same year and improving slightly to -1.96% by March 2025.

PE: -169.3x

Nordic Semiconductor's recent performance highlights its potential as an undervalued stock in Europe. Despite a volatile share price over the past three months, the company reported significant improvements in Q1 2025, with sales doubling to US$155.07 million and net income reaching US$1.15 million from a prior loss. Insider confidence is evident as CEO Vegard Wollan purchased 80,000 shares for approximately US$8.32 million, reflecting strong belief in future growth prospects amidst ongoing earnings expansion forecasts of nearly 48% annually.

Taking Advantage

- Explore the 66 names from our Undervalued European Small Caps With Insider Buying screener here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Elmera Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:ELMRA

Elmera Group

Engages in the purchase, sale, and portfolio management of electrical power to households, private and public companies, and municipalities in Norway, Sweden, and Finland.

Undervalued with high growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)