Advertisement

Industry Analysts Just Made An Upgrade To Their LINK Mobility Group Holding ASA (OB:LINK) Revenue Forecasts

LINK Mobility Group Holding ASA (OB:LINK) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's statutory forecasts. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects. LINK Mobility Group Holding has also found favour with investors, with the stock up a notable 12% to kr37.79 over the past week. Could this upgrade be enough to drive the stock even higher?

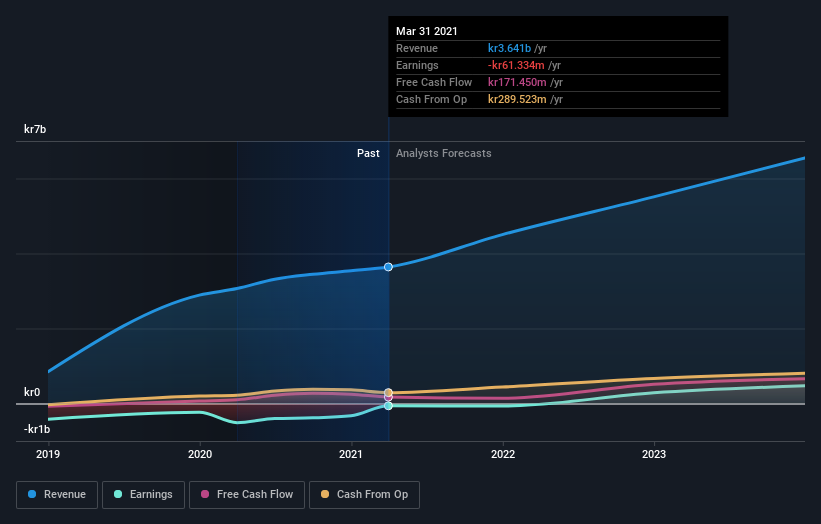

After this upgrade, LINK Mobility Group Holding's twin analysts are now forecasting revenues of kr4.5b in 2021. This would be a substantial 24% improvement in sales compared to the last 12 months. The loss per share is anticipated to greatly reduce in the near future, narrowing 85% to kr0.18. Previously, the analysts had been modelling revenues of kr4.3b and earnings per share (EPS) of kr0.05 in 2021. Yet despite a slight bump in revenues, the analysts are now forecasting a loss instead of a profit, which looks like an overall reduction in sentiment.

View our latest analysis for LINK Mobility Group Holding

The consensus price target stayed unchanged at kr51.00, seeming to suggest that higher forecast losses are not expected to have a long term impact on the valuation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on LINK Mobility Group Holding, with the most bullish analyst valuing it at kr58.00 and the most bearish at kr44.00 per share. Still, with such a tight range of estimates, it suggests the analysts have a pretty good idea of what they think the company is worth.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. The analysts are definitely expecting LINK Mobility Group Holding's growth to accelerate, with the forecast 53% annualised growth to the end of 2021 ranking favourably alongside historical growth of 19% per annum over the past year. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 21% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect LINK Mobility Group Holding to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that analysts are expecting LINK Mobility Group Holding to become unprofitable this year. They also upgraded their revenue estimates for this year, and sales are expected to grow faster than the wider market. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at LINK Mobility Group Holding.

That's a pretty serious upgrade, but shareholders might be even more pleased to know that forecasts expect LINK Mobility Group Holding to be able to reach break-even within the next few years. You can learn more about these forecasts, for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you decide to trade LINK Mobility Group Holding, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OB:LINK

LINK Mobility Group Holding

Provides mobile and communication-platform-as-a-service solutions.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1359.3% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

99 followersusers have followed this narrative

10 commentsusers have commented on this narrative

19 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative