Advertisement

- Norway

- /

- Specialty Stores

- /

- OB:ELIMP

Elektroimportøren (OB:ELIMP) Will Be Hoping To Turn Its Returns On Capital Around

What trends should we look for it we want to identify stocks that can multiply in value over the long term? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. However, after briefly looking over the numbers, we don't think Elektroimportøren (OB:ELIMP) has the makings of a multi-bagger going forward, but let's have a look at why that may be.

Our free stock report includes 1 warning sign investors should be aware of before investing in Elektroimportøren. Read for free now.Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Elektroimportøren, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

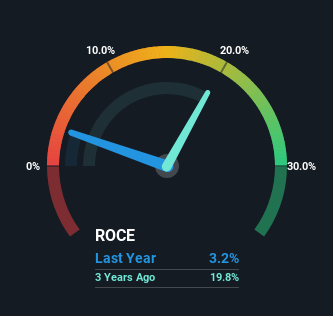

0.032 = kr39m ÷ (kr1.6b - kr358m) (Based on the trailing twelve months to December 2024).

Thus, Elektroimportøren has an ROCE of 3.2%. In absolute terms, that's a low return and it also under-performs the Specialty Retail industry average of 10%.

See our latest analysis for Elektroimportøren

Above you can see how the current ROCE for Elektroimportøren compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for Elektroimportøren .

What The Trend Of ROCE Can Tell Us

The trend of ROCE doesn't look fantastic because it's fallen from 15% five years ago, while the business's capital employed increased by 281%. Usually this isn't ideal, but given Elektroimportøren conducted a capital raising before their most recent earnings announcement, that would've likely contributed, at least partially, to the increased capital employed figure. It's unlikely that all of the funds raised have been put to work yet, so as a consequence Elektroimportøren might not have received a full period of earnings contribution from it. It's also worth noting the company's latest EBIT figure is within 10% of the previous year, so it's fair to assign the ROCE drop largely to the capital raise.

On a related note, Elektroimportøren has decreased its current liabilities to 23% of total assets. So we could link some of this to the decrease in ROCE. What's more, this can reduce some aspects of risk to the business because now the company's suppliers or short-term creditors are funding less of its operations. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.

What We Can Learn From Elektroimportøren's ROCE

In summary, Elektroimportøren is reinvesting funds back into the business for growth but unfortunately it looks like sales haven't increased much just yet. It seems that investors have little hope of these trends getting any better and that may have partly contributed to the stock collapsing 79% in the last three years. Therefore based on the analysis done in this article, we don't think Elektroimportøren has the makings of a multi-bagger.

If you want to continue researching Elektroimportøren, you might be interested to know about the 1 warning sign that our analysis has discovered.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if Elektroimportøren might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:ELIMP

Elektroimportøren

Engages in the sale of electrical installation products to private and professional customers in Norway.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|33.9% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|26.5% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.3% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor