Advertisement

European Market: 3 Stocks That Might Be Priced Below Their Estimated Worth

Simply Wall St

Reviewed by Simply Wall St

As European markets grapple with the impact of new U.S. trade tariffs and broader economic uncertainties, investors are increasingly focused on identifying opportunities in stocks that may be trading below their intrinsic value. In this context, understanding the fundamentals and potential resilience of a company can be crucial for spotting undervalued stocks that could offer long-term growth despite current market challenges.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Micro Systemation (OM:MSAB B) | SEK51.20 | SEK101.51 | 49.6% |

| Bonesupport Holding (OM:BONEX) | SEK294.00 | SEK585.95 | 49.8% |

| Melhus Sparebank (OB:MELG) | NOK167.00 | NOK329.29 | 49.3% |

| Cavotec (OM:CCC) | SEK16.90 | SEK33.71 | 49.9% |

| F-Secure Oyj (HLSE:FSECURE) | €1.754 | €3.48 | 49.7% |

| Carasent (OM:CARA) | SEK20.75 | SEK41.08 | 49.5% |

| Dino Polska (WSE:DNP) | PLN451.40 | PLN887.95 | 49.2% |

| Metsä Board Oyj (HLSE:METSB) | €3.45 | €6.76 | 49% |

| W5 Solutions (OM:W5) | SEK71.60 | SEK142.57 | 49.8% |

| MedinCell (ENXTPA:MEDCL) | €14.40 | €28.62 | 49.7% |

Here's a peek at a few of the choices from the screener.

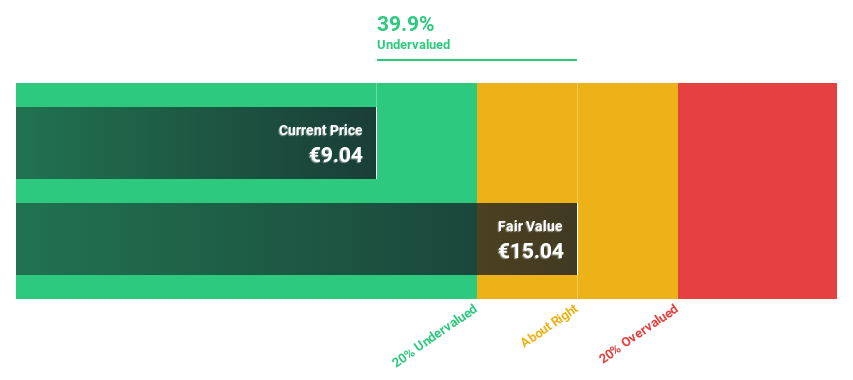

I.CO.P.. Società Benefit (BIT:ICOP)

Overview: I.CO.P. S.p.A. Società Benefit offers construction and special engineering services to both public and private clients in Italy and internationally, with a market cap of €261.98 million.

Operations: The company's revenue is primarily derived from its heavy construction segment, which generated €117.92 million.

Estimated Discount To Fair Value: 37%

I.CO.P. Società Benefit is trading at €9.48, significantly below its estimated fair value of €15.05, highlighting its potential as an undervalued stock based on cash flows. The company's earnings and revenue are projected to grow substantially faster than the Italian market, with annual growth forecasts of 56.3% and 48.4%, respectively. However, interest payments remain a concern as they are not well covered by current earnings, indicating financial pressure despite strong growth prospects.

- The analysis detailed in our I.CO.P.. Società Benefit growth report hints at robust future financial performance.

- Get an in-depth perspective on I.CO.P.. Società Benefit's balance sheet by reading our health report here.

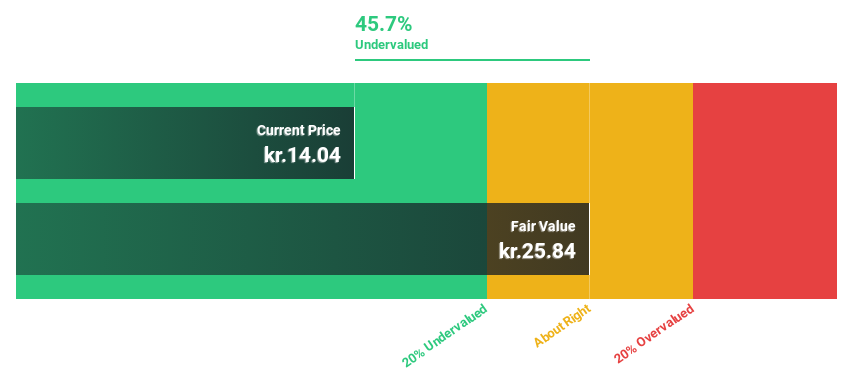

Bang & Olufsen (CPSE:BO)

Overview: Bang & Olufsen A/S is a company that designs, develops, markets, manufactures, and sells audio and video products across Europe, the Middle East, Africa, the Americas, and the Asia Pacific with a market cap of DKK20.09 billion.

Operations: The company's revenue is derived from the APAC region (DKK690 million), EMEA (DKK1.21 billion), and the Americas (DKK302 million).

Estimated Discount To Fair Value: 18.8%

Bang & Olufsen is trading at DKK 13.76, below its estimated fair value of DKK 16.95, suggesting it may be undervalued based on cash flows. Despite recent losses and shareholder dilution, the company maintains revenue growth guidance and forecasts a significant earnings increase of 116.63% per year, surpassing Danish market averages. However, low future return on equity at 6.2% remains a concern amidst these growth projections and executive changes in the boardroom could impact strategic direction.

- Upon reviewing our latest growth report, Bang & Olufsen's projected financial performance appears quite optimistic.

- Unlock comprehensive insights into our analysis of Bang & Olufsen stock in this financial health report.

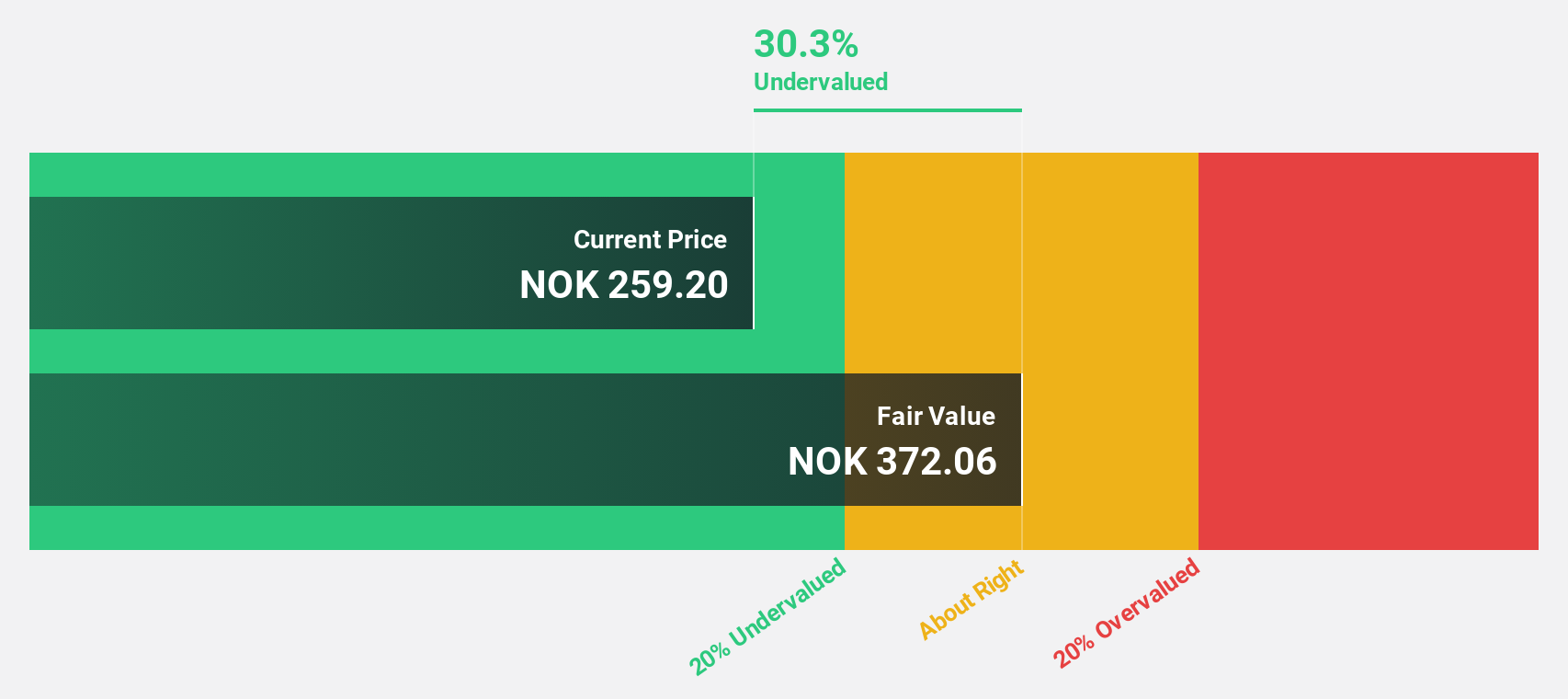

Gjensidige Forsikring (OB:GJF)

Overview: Gjensidige Forsikring ASA, along with its subsidiaries, offers general insurance and pension products across Norway, Sweden, Denmark, Finland, Latvia, Lithuania, and Estonia with a market cap of NOK120.89 billion.

Operations: Gjensidige Forsikring ASA's revenue is primarily derived from its General Insurance Commercial segment at NOK20.99 billion, General Insurance Private segment at NOK15.18 billion, and its operations in Sweden under the General Insurance category at NOK2 billion, along with a Pension segment contributing NOK854.80 million.

Estimated Discount To Fair Value: 34%

Gjensidige Forsikring, trading at NOK 241.8, is priced below its estimated fair value of NOK 366.52, highlighting potential undervaluation based on cash flows. The company's earnings grew by 25.8% last year and are forecast to grow annually by 10.26%, outpacing the Norwegian market's growth rate of 7.9%. However, its dividend yield of 3.72% isn't fully covered by free cash flows, raising sustainability concerns despite robust profit growth projections and a high future return on equity forecasted at 25.4%.

- Our comprehensive growth report raises the possibility that Gjensidige Forsikring is poised for substantial financial growth.

- Take a closer look at Gjensidige Forsikring's balance sheet health here in our report.

Next Steps

- Gain an insight into the universe of 203 Undervalued European Stocks Based On Cash Flows by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:GJF

Gjensidige Forsikring

Provides general insurance and pension products in Norway, Sweden, Denmark, Finland, Latvia, Lithuania, and Estonia.

Reasonable growth potential with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|43.6% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|36.4% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|28.4% undervalued

MA

Community Contributor