- Norway

- /

- Oil and Gas

- /

- OB:HUNT

Rainbows and Unicorns: Hunter Group ASA (OB:HUNT) Analysts Just Became A Lot More Optimistic

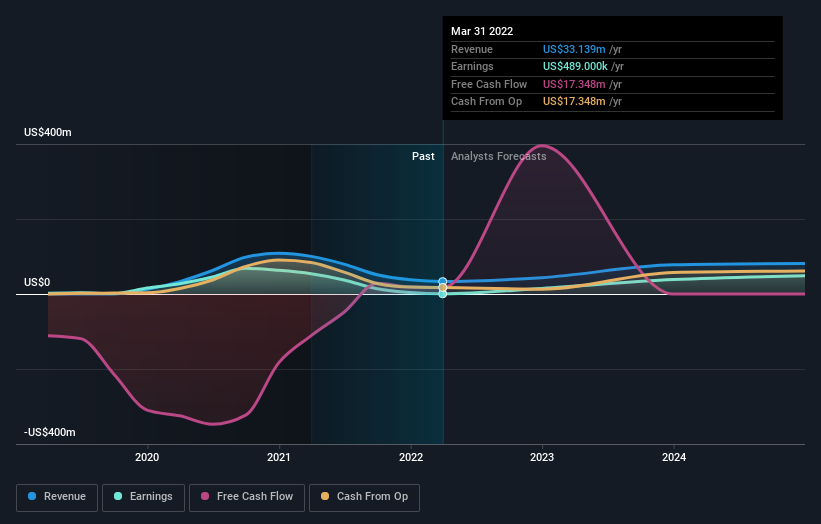

Shareholders in Hunter Group ASA (OB:HUNT) may be thrilled to learn that the analysts have just delivered a major upgrade to their near-term forecasts. Consensus estimates suggest investors could expect greatly increased statutory revenues and earnings per share, with the analysts modelling a real improvement in business performance.

Following the upgrade, the most recent consensus for Hunter Group from its two analysts is for revenues of US$44m in 2022 which, if met, would be a sizeable 32% increase on its sales over the past 12 months. Per-share earnings are expected to bounce 1,187% to US$0.011. Before this latest update, the analysts had been forecasting revenues of US$30m and earnings per share (EPS) of US$0.0056 in 2022. There has definitely been an improvement in perception recently, with the analysts substantially increasing both their earnings and revenue estimates.

Check out our latest analysis for Hunter Group

As a result, it might be a surprise to see that the analysts have cut their price target 12% to kr3.40, which could suggest the forecast improvement in performance is not expected to last. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic Hunter Group analyst has a price target of kr4.00 per share, while the most pessimistic values it at kr2.30. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Of course, another way to look at these forecasts is to place them into context against the industry itself. The analysts are definitely expecting Hunter Group's growth to accelerate, with the forecast 73% annualised growth to the end of 2022 ranking favourably alongside historical growth of 61% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to see a revenue decline of 10% annually. So it's clear with the acceleration in growth, Hunter Group is expected to grow meaningfully faster than the wider industry.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. On the plus side, they also lifted their revenue estimates, and the company is expected to perform better than the wider market. A lower price target is not intuitively what we would expect from a company whose business prospects are improving - at least judging by these forecasts - but if the underlying fundamentals are strong, Hunter Group could be one for the watch list.

Analysts are definitely bullish on Hunter Group, but no company is perfect. Indeed, you should know that there are several potential concerns to be aware of, including its declining profit margins. You can learn more, and discover the 4 other warning signs we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Hunter Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:HUNT

Hunter Group

An investment company, primarily focuses on the shipping and oil service investments in Norway and internationally.

Flawless balance sheet slight.

Market Insights

Community Narratives