Advertisement

- Norway

- /

- Oil and Gas

- /

- OB:EQNR

Could Equinor’s (OB:EQNR) Latest Buy-Back Reveal Shifts in Its Capital Allocation Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this month, Equinor reported the purchase of 1,327,002 of its own shares under the third tranche of its 2025 share buy-back programme, increasing its holdings to 40,990,676 shares, or 1.60% of share capital.

- This move underlines Equinor's ongoing approach to capital returns, with share buy-backs signaling management's focus on shareholder value and confidence in the company’s outlook.

- We’ll now explore how Equinor’s recently disclosed share buy-backs could influence its investment narrative and future capital allocation priorities.

These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Equinor Investment Narrative Recap

To be a shareholder in Equinor today, you need to believe in the durability of European energy demand and the company’s ability to generate stable cash flows from both oil and gas, even as renewables transition pressures grow. The recent buy-back announcement may reinforce near-term confidence in capital returns, but it does not fundamentally alter the most important production and policy catalysts or mitigate the main risk of falling upstream revenues if European demand or regulatory support wavers.

Among recent announcements, Equinor’s ten-year gas supply agreement with BASF stands out because it directly supports cash flow visibility, a key factor underlying the company’s share buy-backs and short-term investor confidence. This contract may help buffer earnings fluctuation, but it does not eliminate exposure to the challenge of sustaining margins as traditional oil and gas fields mature.

Yet, while capital returns offer some reassurance, investors should not lose sight of ...

Read the full narrative on Equinor (it's free!)

Equinor's narrative projects $90.2 billion revenue and $7.6 billion earnings by 2028. This requires a 5.4% yearly revenue decline and a $0.6 billion decrease in earnings from $8.2 billion today.

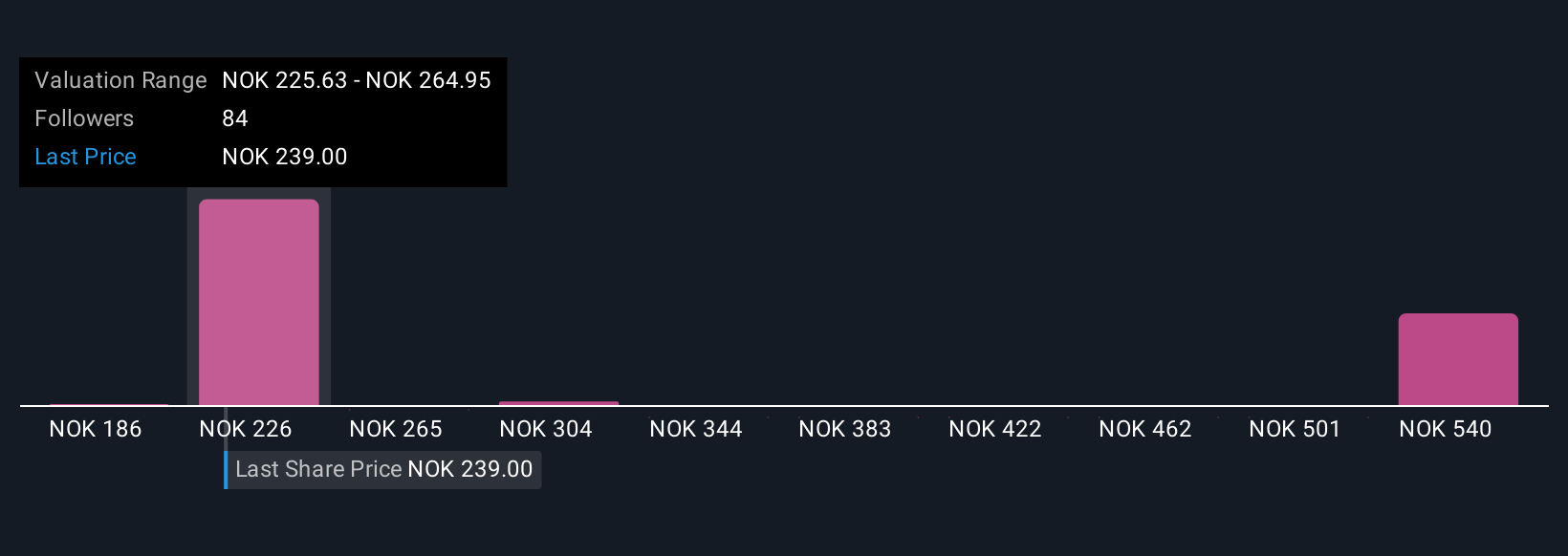

Uncover how Equinor's forecasts yield a NOK253.18 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Sixteen fair value estimates from the Simply Wall St Community span from NOK186 to NOK582 per share, highlighting a wide range of investor expectations. Current consensus admits the risk that ambitious shareholder distributions could become unsustainable if energy prices weaken, so it pays to consider alternative viewpoints before making any decision.

Explore 16 other fair value estimates on Equinor - why the stock might be worth over 2x more than the current price!

Build Your Own Equinor Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Equinor research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Equinor research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Equinor's overall financial health at a glance.

Want Some Alternatives?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 38 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Equinor might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:EQNR

Equinor

An energy company, engages in the exploration, production, transportation, refining, and marketing of petroleum and other forms of energy in Norway and internationally.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.1% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|11.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|39.4% undervalued

TR

Community Contributor