- Norway

- /

- Oil and Gas

- /

- OB:DNO

European Growth Companies With High Insider Ownership In March 2025

Reviewed by Simply Wall St

As of March 2025, the European market has shown resilience with the pan-European STOXX Europe 600 Index ending higher, despite ongoing concerns about U.S. tariffs and mixed performances among major stock indexes. Against this backdrop of cautious optimism and strategic central bank policies, growth companies with high insider ownership can be particularly appealing to investors seeking stability and alignment of interests in uncertain times.

Top 10 Growth Companies With High Insider Ownership In Europe

| Name | Insider Ownership | Earnings Growth |

| Pharma Mar (BME:PHM) | 11.8% | 40.8% |

| Elicera Therapeutics (OM:ELIC) | 27.8% | 97.2% |

| Vow (OB:VOW) | 13.1% | 111.2% |

| Bonesupport Holding (OM:BONEX) | 10.1% | 50.2% |

| CD Projekt (WSE:CDR) | 29.7% | 39.1% |

| Bergen Carbon Solutions (OB:BCS) | 12% | 50.8% |

| Elliptic Laboratories (OB:ELABS) | 22.6% | 88.2% |

| Nordic Halibut (OB:NOHAL) | 29.8% | 56.3% |

| Ortoma (OM:ORT B) | 27.7% | 68.6% |

| Circus (XTRA:CA1) | 26% | 51.4% |

We're going to check out a few of the best picks from our screener tool.

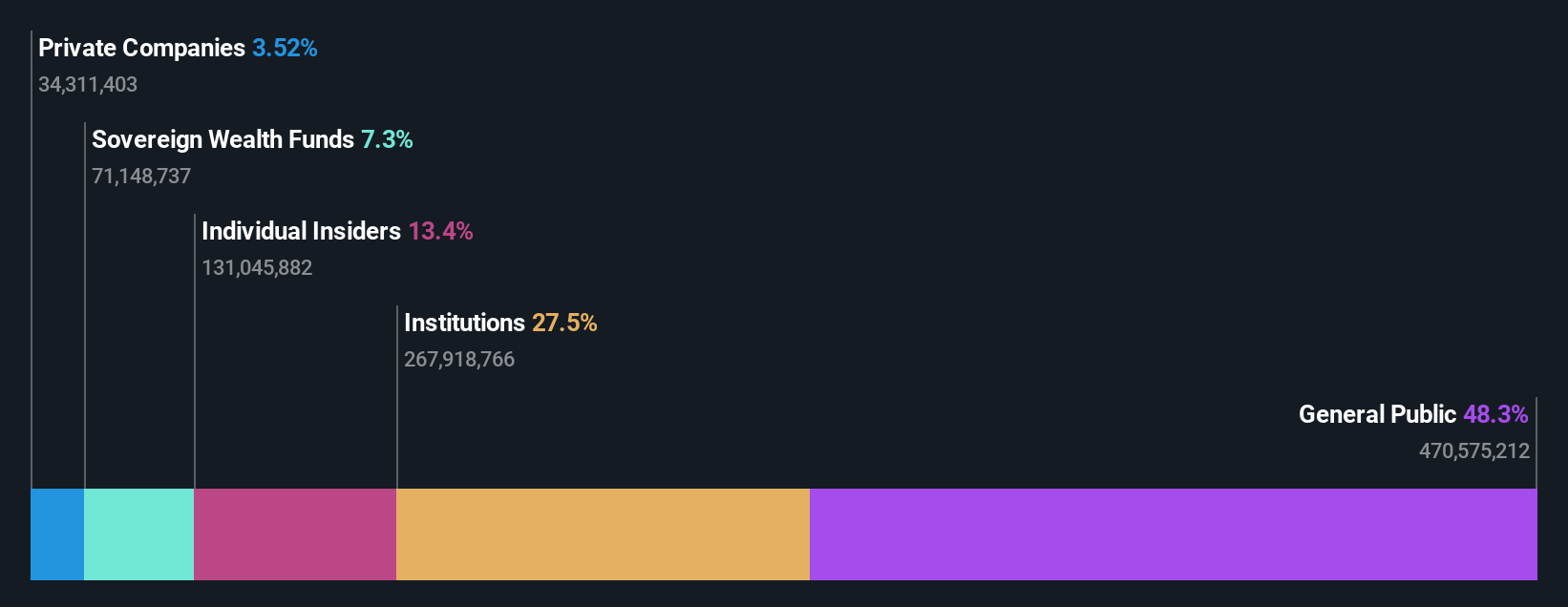

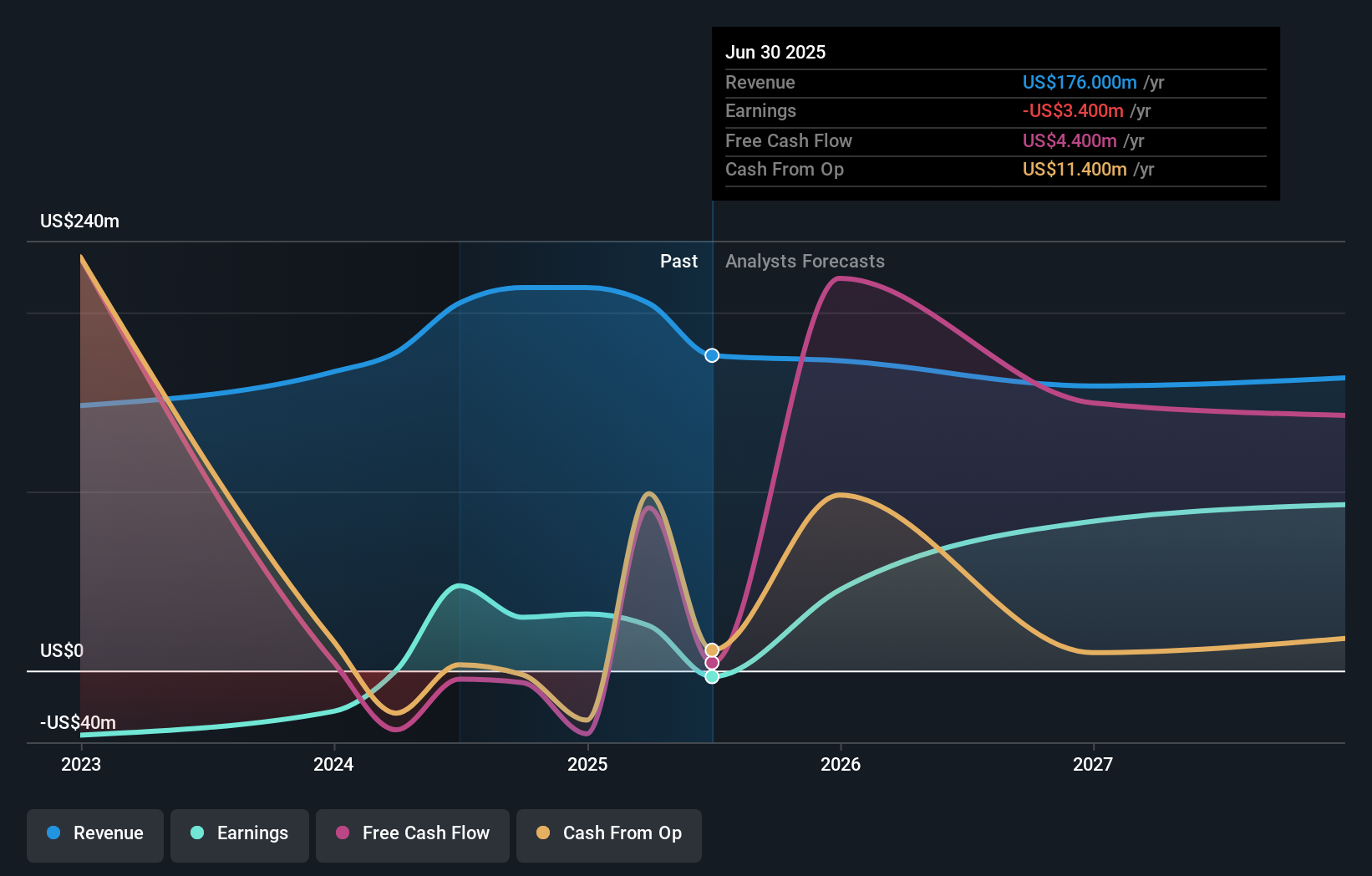

DNO (OB:DNO)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: DNO ASA is involved in the exploration, development, and production of oil and gas assets across the Middle East, the North Sea, and West Africa with a market capitalization of NOK13.41 billion.

Operations: The company's revenue primarily comes from its oil and gas activities, amounting to $666.80 million.

Insider Ownership: 13.1%

Earnings Growth Forecast: 70.1% p.a.

DNO is positioned for growth with its strategic acquisition of Sval Energi and a promising gas/condensate discovery at the Mistral prospect. Despite a forecasted low return on equity of 10.6% in three years, DNO's earnings are expected to grow significantly by 70.08% annually, surpassing market averages as it becomes profitable. However, its dividend yield of 8.49% is not well covered by earnings or cash flows, indicating potential sustainability concerns.

- Unlock comprehensive insights into our analysis of DNO stock in this growth report.

- Insights from our recent valuation report point to the potential overvaluation of DNO shares in the market.

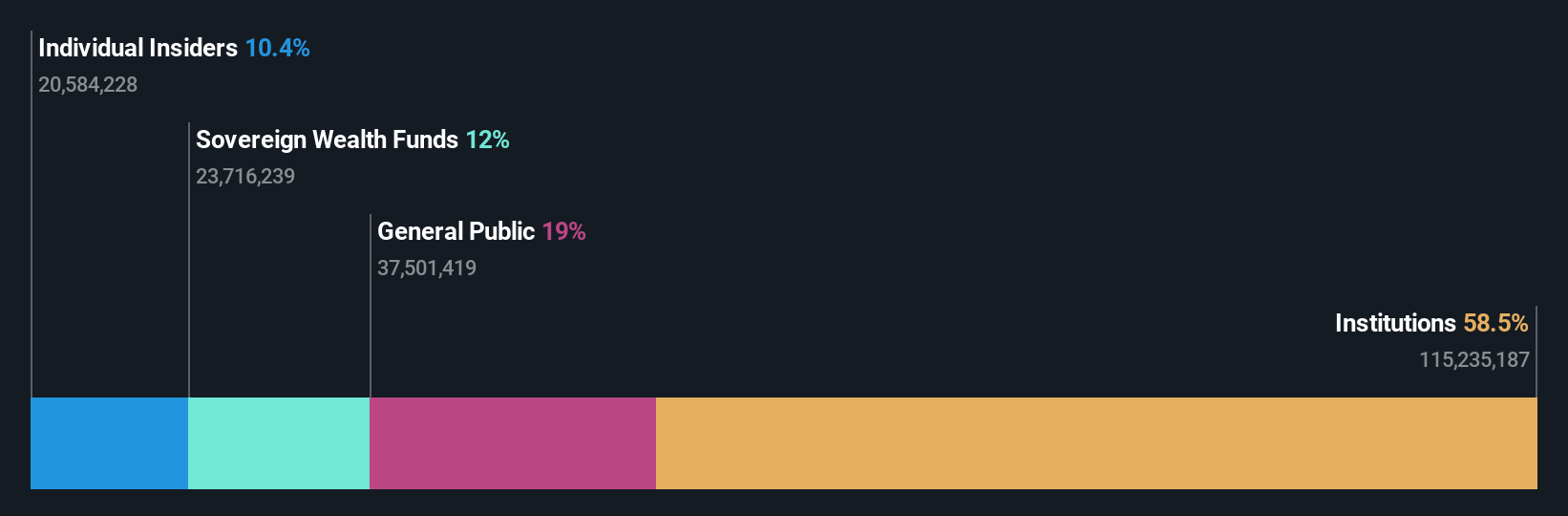

Nordic Semiconductor (OB:NOD)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Nordic Semiconductor ASA is a fabless semiconductor company that designs, sells, and delivers integrated circuits for short- and long-range wireless applications across Europe, the Americas, and the Asia Pacific, with a market cap of NOK25.44 billion.

Operations: Nordic Semiconductor generates revenue from designing, selling, and delivering integrated circuits and related products for wireless applications in Europe, the Americas, and the Asia Pacific.

Insider Ownership: 10.7%

Earnings Growth Forecast: 51.6% p.a.

Nordic Semiconductor is poised for growth, with forecasts indicating a 51.61% annual earnings increase and revenue growth of 15.3% per year, outpacing the Norwegian market. Despite recent volatility in its share price and a forecasted low return on equity of 18.9%, the company trades at 44.3% below estimated fair value, suggesting potential upside. The ongoing share repurchase program further underscores management's confidence in its long-term strategy to support employee incentive plans.

- Take a closer look at Nordic Semiconductor's potential here in our earnings growth report.

- Insights from our recent valuation report point to the potential undervaluation of Nordic Semiconductor shares in the market.

Paratus Energy Services (OB:PLSV)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Paratus Energy Services Ltd. operates by owning and managing jack-up drilling rigs through its subsidiaries under contracts in Mexico, with a market cap of NOK6.87 billion.

Operations: The company's revenue segments include $213.90 million from Fontis and $194.80 million from Seagems.

Insider Ownership: 29.1%

Earnings Growth Forecast: 26.4% p.a.

Paratus Energy Services is positioned for significant growth, with earnings expected to increase by 26.4% annually, surpassing the Norwegian market's average. Although revenue growth of 2% per year lags behind market expectations, the company's return on equity is projected to reach a very high level of 80.9%. Trading at 66% below estimated fair value and with no recent insider trading activity, Paratus offers potential value despite its financial challenges in covering interest payments.

- Delve into the full analysis future growth report here for a deeper understanding of Paratus Energy Services.

- According our valuation report, there's an indication that Paratus Energy Services' share price might be on the cheaper side.

Seize The Opportunity

- Explore the 235 names from our Fast Growing European Companies With High Insider Ownership screener here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:DNO

DNO

Engages in the exploration, development, and production of oil and gas assets in the Middle East, the North Sea, and West Africa.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives