Advertisement

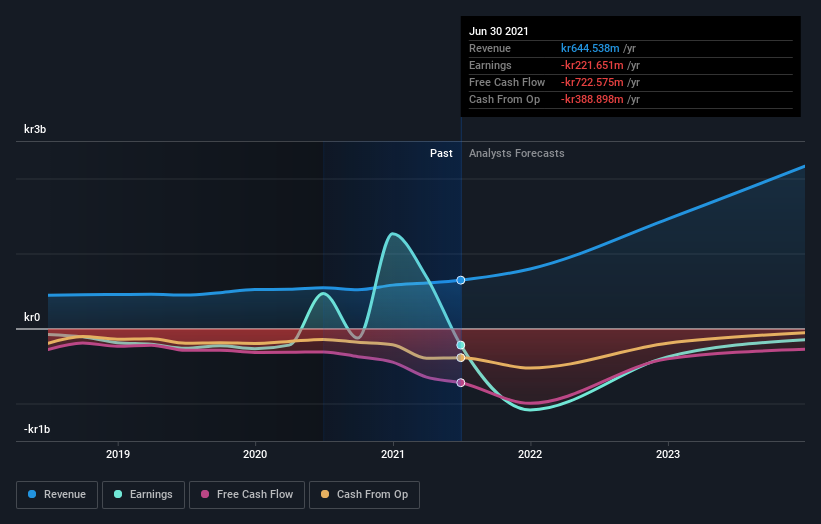

Market forces rained on the parade of Nel ASA (OB:NEL) shareholders today, when the analysts downgraded their forecasts for this year. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon.

After the downgrade, the 14 analysts covering Nel are now predicting revenues of kr794m in 2021. If met, this would reflect a major 23% improvement in sales compared to the last 12 months. Losses are supposed to balloon 394% to kr0.76 per share. Yet before this consensus update, the analysts had been forecasting revenues of kr945m and losses of kr0.47 per share in 2021. Ergo, there's been a clear change in sentiment, with the analysts administering a notable cut to this year's revenue estimates, while at the same time increasing their loss per share forecasts.

See our latest analysis for Nel

The consensus price target fell 13% to kr22.64, with the analysts clearly concerned about the company following the weaker revenue and earnings outlook. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic Nel analyst has a price target of kr33.00 per share, while the most pessimistic values it at kr8.00. With such a wide range in price targets, the analysts are almost certainly betting on widely diverse outcomes for the underlying business. As a result it might not be possible to derive much meaning from the consensus price target, which is after all just an average of this wide range of estimates.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Nel's past performance and to peers in the same industry. It's clear from the latest estimates that Nel's rate of growth is expected to accelerate meaningfully, with the forecast 52% annualised revenue growth to the end of 2021 noticeably faster than its historical growth of 30% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 6.8% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Nel to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that analysts increased their loss per share estimates for this year. While analysts did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. After such a stark change in sentiment from analysts, we'd understand if readers now felt a bit wary of Nel.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Nel going out to 2023, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you’re looking to trade Nel, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Nel might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OB:NEL

Nel

A hydrogen company, provides solutions to produce, store, and distribute hydrogen from renewable energy in Norway and internationally.

Flawless balance sheet with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|29.6% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|49.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.8% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.2% undervalued

AX

Community Contributor