- Netherlands

- /

- Hospitality

- /

- ENXTAM:BFIT

3 Euronext Amsterdam Growth Stocks With Insider Ownership Growing Earnings Up To 108%

Reviewed by Simply Wall St

In a global market environment marked by economic uncertainty and fluctuating indices, the Euronext Amsterdam has shown resilience, driven by strong fundamentals in certain sectors. Despite broader concerns about a slowdown in economic growth, some companies continue to demonstrate robust earnings and high insider ownership, which can be indicative of confidence in their long-term prospects. When evaluating stocks under these conditions, it is crucial to consider those with growing earnings and significant insider ownership as these factors often signal strong management alignment with shareholder interests. Here are three growth stocks listed on Euronext Amsterdam that exemplify these characteristics.

Top 5 Growth Companies With High Insider Ownership In The Netherlands

| Name | Insider Ownership | Earnings Growth |

| Envipco Holding (ENXTAM:ENVI) | 36.7% | 79.2% |

| Ebusco Holding (ENXTAM:EBUS) | 33.2% | 107.8% |

| Basic-Fit (ENXTAM:BFIT) | 12% | 77.1% |

| MotorK (ENXTAM:MTRK) | 35.7% | 108.4% |

| CVC Capital Partners (ENXTAM:CVC) | 20.2% | 32.6% |

| PostNL (ENXTAM:PNL) | 35.6% | 36.4% |

Below we spotlight a couple of our favorites from our exclusive screener.

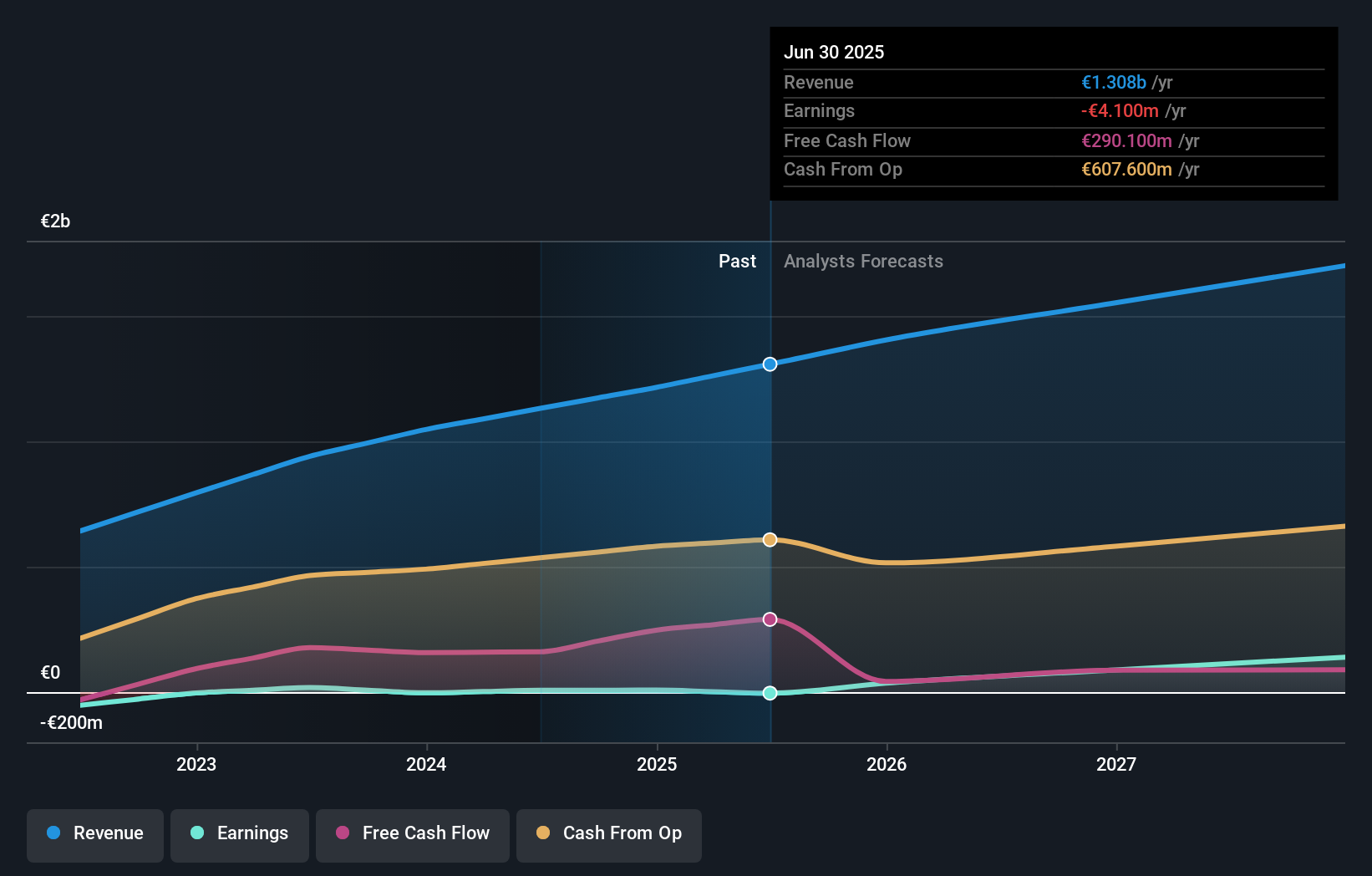

Basic-Fit (ENXTAM:BFIT)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Basic-Fit N.V., with a market cap of €1.44 billion, operates fitness clubs through its subsidiaries.

Operations: The company's revenue segments are divided into Benelux, contributing €505.17 million, and France, Spain & Germany, generating €626.41 million.

Insider Ownership: 12%

Earnings Growth Forecast: 77.1% p.a.

Basic-Fit demonstrates strong growth potential with high insider ownership and a forecasted earnings growth of 77.1% per year, significantly outpacing the Dutch market. Recent earnings reports show substantial improvement, with revenue rising to €584.76 million and net income turning positive at €4.18 million for H1 2024. Although profit margins have decreased, the company’s return on equity is expected to be robust at 25.1% in three years, indicating solid future prospects despite slower revenue growth compared to peers.

- Get an in-depth perspective on Basic-Fit's performance by reading our analyst estimates report here.

- Our valuation report here indicates Basic-Fit may be overvalued.

CVC Capital Partners (ENXTAM:CVC)

Simply Wall St Growth Rating: ★★★★★☆

Overview: CVC Capital Partners plc is a private equity and venture capital firm that focuses on middle market secondaries, infrastructure and credit, management buyouts, leveraged buyouts, growth equity, mature investments, recapitalizations, strip sales, and spinouts with a market cap of €20.09 billion.

Operations: Revenue Segments (in millions of €): null

Insider Ownership: 20.2%

Earnings Growth Forecast: 32.6% p.a.

CVC Capital Partners, a major private equity firm with high insider ownership, is forecasted to achieve significant earnings growth of 32.6% annually over the next three years, outpacing the Dutch market's 18.7%. Recent M&A activities include leading bids for Deutsche Bahn’s DB Schenker and Aavas Financiers Limited. Despite trading at 31.9% below estimated fair value and having substantial debt, CVC’s return on equity is expected to be very high at 48.7% in three years.

- Dive into the specifics of CVC Capital Partners here with our thorough growth forecast report.

- Our expertly prepared valuation report CVC Capital Partners implies its share price may be too high.

MotorK (ENXTAM:MTRK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: MotorK plc, with a market cap of €266.51 million, offers software-as-a-service solutions for the automotive retail industry across Italy, Spain, France, Germany, and the Benelux Union.

Operations: The company generates €42.50 million in revenue from its Software & Programming segment.

Insider Ownership: 35.7%

Earnings Growth Forecast: 108.4% p.a.

MotorK is expected to achieve significant revenue growth of 22.1% annually, outpacing the Dutch market's 9.4%. Despite a net loss of €6.48 million for H1 2024, down from €7.8 million a year ago, MotorK is forecasted to become profitable within three years. Insider ownership remains high with no substantial insider trading in the past three months. The company recently appointed Zoltan Gelencser as CFO, bringing extensive global finance experience to the team.

- Click to explore a detailed breakdown of our findings in MotorK's earnings growth report.

- According our valuation report, there's an indication that MotorK's share price might be on the expensive side.

Key Takeaways

- Embark on your investment journey to our 6 Fast Growing Euronext Amsterdam Companies With High Insider Ownership selection here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Basic-Fit might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:BFIT

High growth potential low.